Today’s episode is brought to you by Parafin - the leading provider of ready-to-launch financial products that help your merchants grow. Check out what Parafin can do to drive revenue, retention, and TAM at your business!

Alright, let’s dive in…

Magic raised a $10M seed for loyalty software for restaurants. Remember 2010 when loyalty was hot? Every restaurant had kiosks everywhere. Most died. But the ones that got POS distribution (like what Toast acquired) worked. Lerer Hippeau led, joined by Bling Capital, Floodgate, Major Food Group, and VCR Group. Will be interesting to see if loyalty makes a comeback.

Streetbeat, a Palo Alto, Calif.-based developer of agents for wealth managers, raised $15m in Series A funding, per Axios Pro. CDP Venture Capital led, joined by TTV Capital, P101, Monte Carlo Capital, 3Lines VC, Azimut, and Evolution VC.

Beacon Software raised $250M from General Catalyst at a $1B valuation. The founder calls it an “anti-private equity” roll-up - smart positioning when PE has such a bad taste in founders’ mouths. Different model than Valsoft/Constellation but watching closely.

ChipAgents raised $21M Series A from Bessemer for AI in chip design. They sit on top of Cadence/Synopsys and use multi-agent workflows to speed up chip testing and debugging. With all the infrastructure bubble money going into data centers, improving chip design speed is critical. Also saw Chipmine raise $2.5M for similar. This vertical is heating up.

Sam Youssef, Founder & CEO @ Valsoft

You know those revenue leaders who just get it? Kyle Norton is one of them. He is one of the best software sales leaders in vertical SaaS right now.

Sam Youssef is the founder and CEO of Valsoft. You may not have heard of them. You really should.

130+ companies acquired

$750M+ in revenue

3,000+ employees

Multi-billion dollar valuation

Fastest Canadian company to reach $2B valuation

And he’s done it all following a playbook that’s equal parts Warren Buffett, Constellation Software, and hard-won operational experience.

Here’s his story.

From Shoveling Driveways to Building a Berkshire Hathaway for Software

Sam started as a lifelong entrepreneur. Shoveling neighbors’ driveways as a teenager. Contracting a bunch of people. Growing. Starting other businesses.

In 2011, he started an investing company called Valsif Capital with money he’d made along the way. He read Snowball - the Warren Buffett biography. And thought:

So he started buying value stocks. Cheap stocks that would go up.

He lost a bunch of money.

It wasn’t working. So they adapted. They kept learning. They started buying stocks in better companies - companies with:

High predictability of revenue

Mission criticality with customers

Pricing power

Great management teams

By 2011-2012, they were buying software companies in the public markets.

They invested early in companies during the SaaS boom. Valsif Capital took off. They started doing extremely well.

The Constellation Moment

They ran into Constellation Software. Constellation became their largest position. A very large position. Sam and his partners thought:

Their plan: Buy one company and see how it goes.

They bought one company in South Florida - a hotel management software company. They did extremely well with it. Using those cash flows and some money from the markets:

Year 1: 1 acquisition

Year 2: 3 acquisitions

Year 3: 5 acquisitions

Year 4: 8 acquisitions

Fast forward to 2022: Some of the largest institutional investors in America backed Valsoft.

Today: 130 companies, $750M+ revenue, multi-billion dollar valuation.

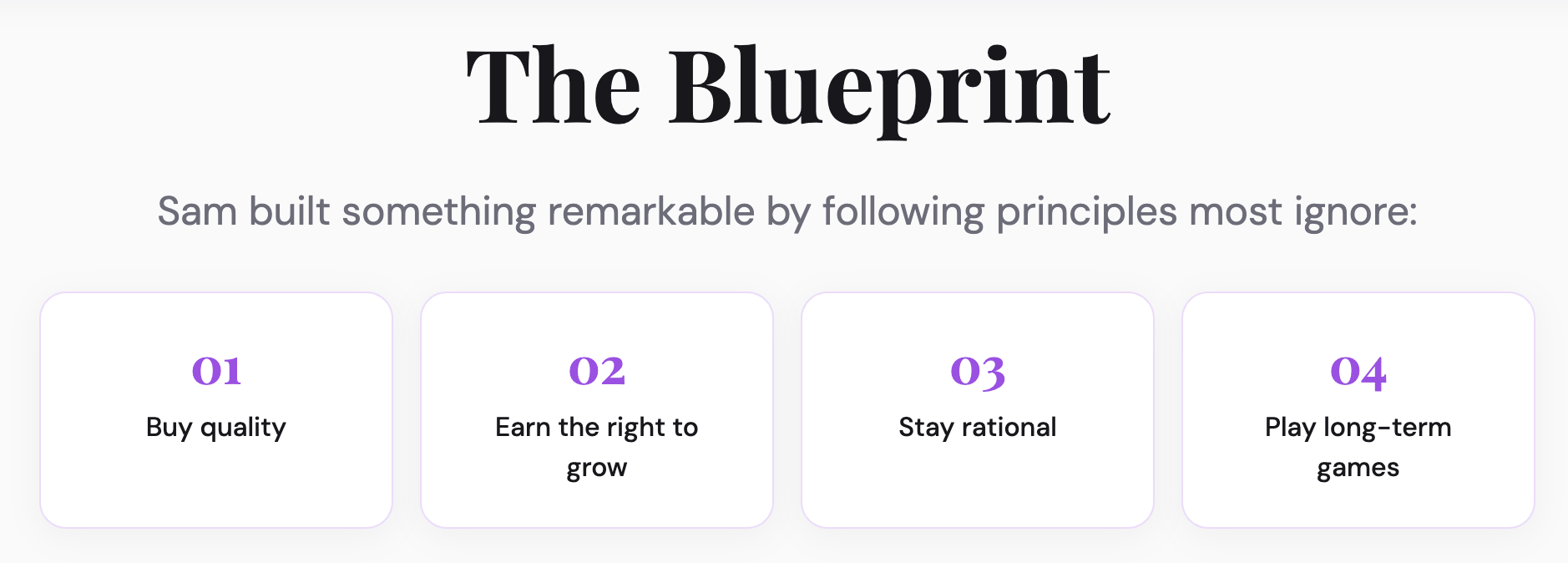

Throughout the history of the company, the strategy has been the same:

Buy good companies with a strong presence in rationally-structured markets where they can have enduring economics. Companies that have been around for decades. Then look for ways to grow them and generate operating leverage.

Inside an M&A Factory & How To Earn The Right To Be An Acquirer

Sam’s seen the M&A graveyard. He’s made the mistakes. And he’s learned from 130+ acquisitions across a decade.

Here’s what separates Valsoft from the companies that waste shareholder capital.

1. You Have to Earn the Right to Be an Acquirer

Sam is religious about this principle.

“You earn the right to be an acquirer by managing businesses better than they were previously managed.”

That means:

You can drive more growth out of them

You can drive more profitability out of them

You have something to bring to these businesses that will make them better

If you’re just buying companies to grow revenue, you’re doing it wrong.

Valsoft has seven proprietary integration playbooks. They discuss these with founders before the acquisition. There’s usually a reward tied to execution.

Some of the things they do:

Payments infrastructure: Bundle payments into the software

AI widgets: Most industries have 1-3 successful AI applications they can add to meaningfully increase ARR

Product expansion: They have large development centers in Sri Lanka and India where they can bring 20-25 developers to revamp an application, eliminate tech debt, and iterate faster

Acquisitive growth: Buy competitors or adjacent products to sell into the base

2. Only Buy Companies with Staying Power

“When a company goes through the acquisition process, it will be mismanaged for a little bit. You go through some team members that don’t adapt well. The integration can be tumultuous.”

So you need to buy companies that, on their own, have staying power. They’re not fickle.Valsoft looks for:

Companies between $3M - $100M in revenue (concentration risk concern on the bigger end)

Mission-critical to their customers

Strong fundamentals and market presence

Companies that have been around for decades (they bought one company founded in 1955)

If a company has survived 70 years, weathered every attack on its domain, and remained independent and successful - there must be something special about it.

3. The First Deal: $5M to $10M+ EBITDA

Their very first acquisition is a masterclass.

They bought a hotel management software company in Tampa for $5 million. It was making about $1.5M EBITDA. Very reputable company. Thousands of customers globally. Leader in the boutique hotel market. Slightly declining market share but good product suite. The founder wanted to move to California and needed to sell for tax reasons.

Problem: Sam had never run a software company in his life.

His plan: Keep the manager in place, collect the money, tweak it a bit, and generate a good return.

Two weeks later, the manager quit.

Now Sam’s in Montreal with a company in Tampa and nobody to run it. So he went down there. Checked things out. Learned what people were doing. Got involved. He brought in one of his colleagues, Michael Assi, as president.

18 months later: This company that they bought for $5M was making $3M EBITDA.

Today: This company makes upwards of $10M+ of EBITDA.

The hospitality suite built from that core platform is now $50-60M in revenue and extremely successful for Valsoft. How? Product expansion. Most products were already there - they just added development resources. The old owner ran a lean ship and had a good company. But when an owner comes in with a multi-decade view, they invest differently.

All the profitability increases came from revenue growth. The company has many more people working there today than when they bought it.

4. Build Scale in M&A Infrastructure

Valsoft has over 100 people looking for deals in every corner of the world. They have people in 25 different countries. In the US and Canada, they have people who cover internationally too.

In Year 1: It was very hard to get a response.

In Year 2: It was a little easier.

Today: They benefit from the reputation of Valsoft. They’ve bought 130+ companies. People take them seriously. More deals go through brokers, and the brokers know them - probably their firm has sold a company to Valsoft before.

At any moment in time, they have over 20 due diligence projects ongoing.

Why? Because they need to be selective. If you’re looking at three companies and you want to do M&A, the pickings are slim. You don’t get to choose your opportunity effectively.

They have no problem not doing any acquisitions if the opportunities aren’t good.

5. Underwrite Every Deal on a Standalone Basis

Here’s where most acquirers screw up. Many acquirers will say:

“Our stock trades at 15x EBITDA. We can buy companies at 10x EBITDA. It’s accretive to shareholders. Good deal.”

Those always fail in the long term.

Why? Your stock trades at a moment in time. That can vary widely.

When you purchase an asset, it’s a long-term investment with your shareholder’s capital. You need to make sure you’re making a good deal standalone.

Valsoft underwrites each acquisition to an unlevered IRR on a standalone basis. They model a very conservative terminal value because the further out you’re modeling, the less certain it is.

Sam’s philosophy:

They’ve bought businesses for 1x ARR. They’ve bought businesses for 10x ARR.

If it’s a product they really want in an industry they’re already in with a stable of customers who could benefit - they’ll pay a lot.

If it’s a declining business with tech debt that’s going to hurt their organic profile - they’ll pay a very low multiple because there’s a lot of risk.

6. People of High Integrity Build Businesses of High Integrity

“If you end up dealing with people of low integrity in an acquisition process, the person selling you the business knows a lot more about the business than you do.”

The quality of your counterparty in any transaction is vital.

If you’re not comfortable with the culture of the company or the people you’re dealing with, regardless of what the numbers say - walk away.

People are good at making things look good in presentations and decks.

Valsoft has had learning experiences over the years:

Bought subscale companies that deteriorated with time

Bought companies with customer concentration where they lost big customers

Dealt with low-integrity sellers

But they’ve also had a lot of companies that are 10x what they were when they bought them.

Sam’s hit rate: Maybe 25-35% of acquisitions have outcomes below expectations. The majority have outcomes better than expectations.

Thinking About AI

Sam has a perspective on AI that’s more nuanced than most. He’s not panicking. He’s not dismissive. He’s operating with eyes wide open. Here’s what he sees…

The Big Picture: This Is the Next Technology Wave

“When the GUI came out, a lot of companies went out of business and a lot of companies grew a lot. When cloud came out, a lot of companies became legacy and a lot of companies grew a lot. When mobility came out, there was a wave of value creation.”

AI is the same thing.

It’s another continuation of the technology cycle that began decades ago.

Sam thinks about it like railroads. When railroads came out, a lot of businesses were enabled by that. Restaurants around railroad stops started popping up. You have to think: What type of stuff is this going to enable? And you have to get there early to protect and expand your market share.

Systems of Record Will Capture More of the Customer Workflow

Dave Friedberg said on All In two years ago:

“It’s the death of vertical SaaS because end customers are just going to build their own AI tooling.”

Sam disagrees.

“I think horizontal-type solutions are more at risk than vertical solutions.”

Why? Vertical companies aren’t just software providers. They’re:

Integrated to all kinds of industry-specific things

Staffed with experts in the vertical who support and service customers

Acting like consultants with very specific workflows

Providing Intel into the industry and best practices through the software

“This one-for-one software thing that people are talking about? I don’t believe in that. I don’t think that’s anywhere near reality.”

The percentage of cost base that software represents to an end customer does not justify losing the expertise that dealing with an external organization that sees hundreds of customers gives you.

Very thin pieces of software could be at risk. But systems of record? The more integrated pieces of software?

“I think they have a good future as long as they’re able to adapt.”

Sam sees things more positively than most. He thinks systems of record are going to grow a lot because they’ll tackle a bigger percentage of the customer’s workflow.

They’re going to be able to grab a bigger part of the economics.

The Risk: Companies with Tech Debt

“Businesses that have a large amount of tech debt - businesses that cannot adapt to the new reality - they’re going to be challenged.”

Why?

Things are going to start moving faster.

The rate at which technology will be produced is going to be significantly higher in the next 10 years than the last 10. You could still kind of make it work over the last 10 years despite that.

In the next 10 years? If you’re not set up in a way where you can build on top of your current stack, it’s going to be difficult.

What’s going to happen:

Your customers are going to become at a competitive disadvantage. And they’re going to want to switch their software solution. Let’s say you’re servicing the revenue cycle management industry. You have an ERP you sell to customers. Your ERP is legacy.

The new features that AI enables could cut a lot of the workflow of agents doing RCM with technology that’s out there today.

If you’re not able to provide that, you’re going to start losing market share.

But if you’re able to do it? Your customers are going to see a lot of value. And they’ll ask: “What else can you do for us?”

You’re likely to make a lot more money down the line than you are today.

How Valsoft Is Adapting

Valsoft runs fully decentralized. All 130 businesses are managed by GMs - usually the old founder or someone with deep vertical expertise. But they build an ecosystem within which vertical market software companies can thrive.

Things that individual companies are subscale to do on their own, Valsoft provides as resources:

1. Global Delivery Centers

Large development centers in Sri Lanka, India, and other places staffed with people who understand how to code using the latest technology. They can augment the product capacity of any company significantly.

Sam says this is probably the area where they bring the most value.

2. Payment Infrastructure

They have their own payment infrastructure they can plug into any company and bundle payments.

R&D Budgets: Up or Down?

Nick asked Sam a great question: “Do you think about that R&D budget changing? Do you suggest or model out a higher R&D budget for AI experimentation?”

Sam’s answer:

“On one side, we’re going to have a lower R&D budget because you can do more with less if you’re set up properly and if you have the right infrastructure to start with.”

But if you don’t have the right infrastructure?

“Well, then you better get there quickly. You’re going to have a problem as technology iterates faster.”

Small Verticals > Big Verticals (Even More So in AI Era)

“For us, the bigger the vertical, the less interesting it is.”

Why?

Small verticals lend themselves better to a rational environment.

Bigger verticals attract a lot of money chasing exponential returns. They’ll get it one in 50 times. But the other 49 times, there’s a lot of money competing irrationally.

In smaller verticals, you need less of a massive investment to protect your market share and be competitive.

If you’re playing in very large spaces, there are a lot of very able entrepreneurs and very large money pools chasing these areas.

In the AI era, this is even more true.

Big verticals are going to see a flood of VC money funding AI-native upstarts. Small verticals? Much more defensible.

Sam built something remarkable by following principles most ignore…

If you’d like to go deeper and watch the full breakdown I highly encourage you to do so. Sam and team have built and absolutely incredible company...

Have a product or service that would be great for our audience of vertical SaaS founders/operators/investors? Reply to this email or shoot us a note at ls@lukesophinos.com