Today’s episode is brought to you by Parafin - the leading provider of ready-to-launch financial products that help your merchants grow. Check out what Parafin can do to drive revenue, retention, and TAM at your business!

Remember folks, you have to watch the video on YouTube. Do us a favor and subscribe while your there :-)

Vertical Titan: Nick Tippman

From vSaaS CMO to Vertical AI Investor

Most VCs say they’re operator-led.

Nick actually is.

The origin story (Indiana → startups → vSaaS)

Nick describes himself as a founder/operator at heart who always wanted to start businesses (family influence), then got obsessed with venture as a senior in college when early VC blogging was taking off (Brad Feld, Fred Wilson, etc.). Source

Before Greenlight Guru, he’d already:

started multiple companies

raised money for one

did an accelerator with another

bootstrapped a media company to a small exit

That’s the “battle scars” resume that matters when you’re advising founders at 2am. Source

Greenlight Guru:

Compliance-heavy vertical SaaS (aka: real work)

Nick was one of the first employees and CMO at Greenlight Guru, a vertical SaaS platform for MedTech companies to get FDA approval and stay compliant. He also led RevOps, wore “many hats,” and later took on product, strategy, and corporate development responsibilities—especially after growth equity came in. Source

And yes—Greenlight Guru raised a ~$120M investment from JMI Equity (growth equity) to accelerate product development and expansion. That’s not “startup Twitter” hype. That’s enterprise-grade vertical SaaS scale in a brutal regulatory environment. Source Source

Concrete traction signals from that era:

Greenlight Guru was serving 500+ medical device customers globally (at the time of the JMI announcement coverage). Source

The company positioned itself as a “single source of truth” across quality/product/regulatory workflows. Source

TipTop VC: checks + collective + “operator trust”

Today, Nick runs TipTop VC, a pre-seed/seed fund focused on vertical software + vertical AI.

What stands out:

Check sizes: $100K–$400K, collaborative, alongside other investors (he mentions Euclid in the convo).

Their positioning is explicitly “built by vSaaS+AI operators for vSaaS+AI operators.”

So here’s the real question for you:

If your product disappeared tomorrow… would your customer’s workflow break? Or would they shrug and ask an agent to recreate it?

The Trillion Dollar Battle for SaaS:

A Debate Between 2 VC’s & a Founder

SaaS stocks are crashing. Claude launched workflow tools. The public markets are panicking. But three investors who spend every day in the trenches of vertical AI see something very different. Here’s what they said — and why it matters.

Is SaaS Dead?

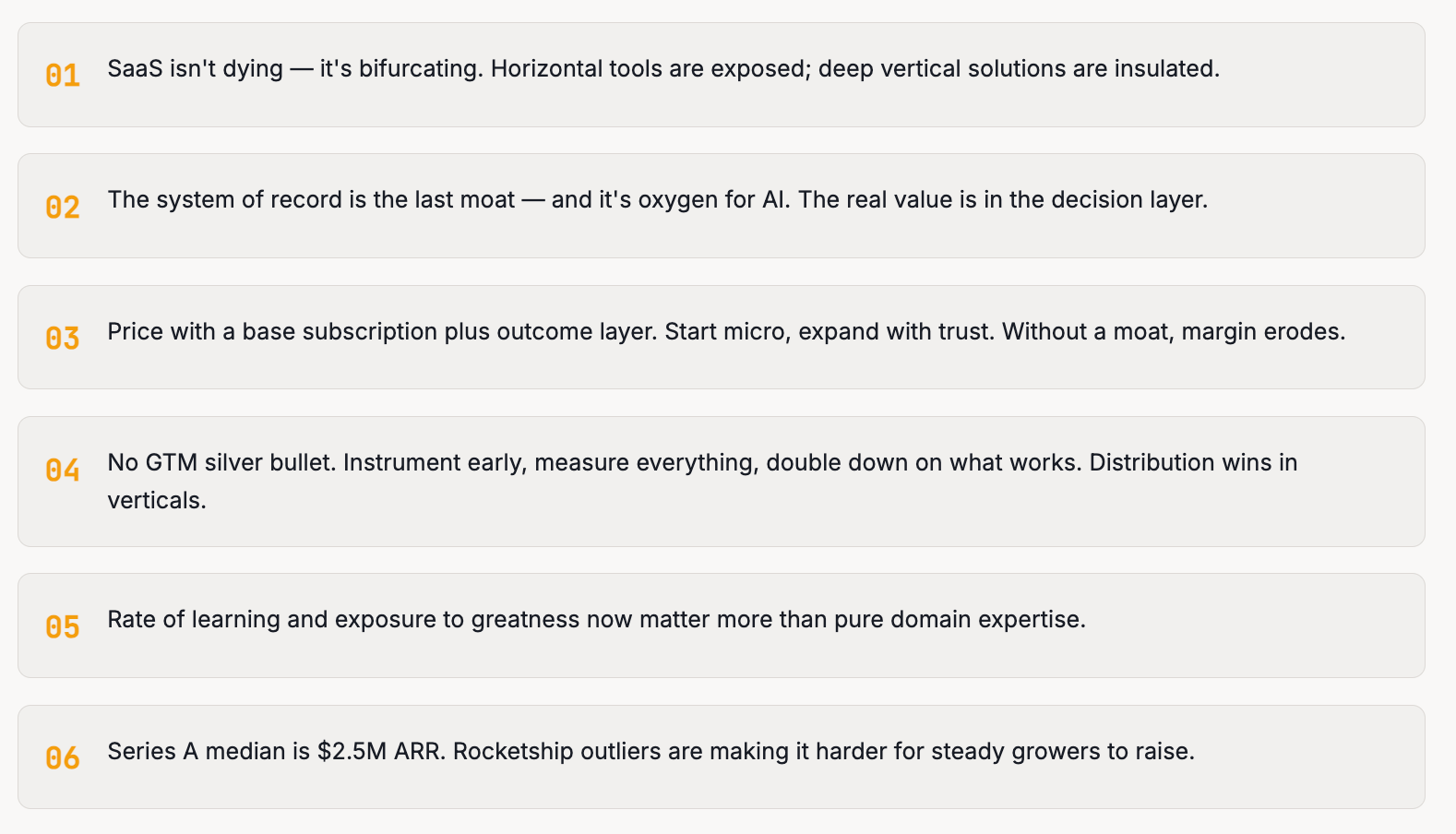

It started with Anthropic releasing Claude’s workflow tools — giving anyone the ability to build internal software through a chat interface. SaaS stocks cratered within days. monday.com drew down hard. Even ServiceNow, with near-100% net retention, took a 10-15% hit. The narrative was swift: if anyone can build their own software, who needs to buy it?

The panic, however, conflates several distinct threats. Can people build their own software and stop buying? Is the seat-based model dying? Can AI handle all workflows autonomously? Each is real in isolation, but they affect different segments very differently. Median public SaaS multiples haven’t actually left their recent trading band — the Claude launch was a catalyst for a repricing already underway.

“This is really just setting up for a battle of epic proportions between AI native upstarts and the legacy SaaS incumbent providers.”

— Nick Tippmann· TipTop VC

The counterintuitive consensus: the most exposed companies are generalist, horizontal solutions — task tracking, project management, basic dashboards. The kind of thing you can now spin up in Claude Code in minutes. Deeply vertical solutions with proprietary data and compliance requirements? They’re the least exposed. You can ask Claude to build a Kanban board. You cannot ask it to build an FDA submission workflow with audit trails and regulatory compliance checks.

The Trillion Dollar Battle

On one side: legacy incumbents with existing relationships, trust, regulatory compliance, and data gravity. On the other: AI-native upstarts with modern architectures, no legacy code, and a willingness to reimagine the product from scratch. Both sides are arming up fast — 55% of SaaS companies have now launched an AI product (up from 31% in 2024), with projections hitting 85% by end of 2026.

But launching an AI product isn’t the same as being AI-native. Most incumbents are bolting features onto existing architectures — a chatbot here, predictive analytics there. That’s fundamentally different from a company built from day one around AI-first workflows. The pattern echoes the on-prem to cloud transition: incumbents dismissed Salesforce and Workday as toys until it was too late.

“Some of the incumbents are thinking these are cute tools and dismissing them as point solutions, but not really understanding they have a broader vision.”

— Nick Tippmann· TipTop VC

The Scorecard

Incumbent Advantages

✦ Customer relationships & trust

✦ System of record with data gravity

✦ Regulatory compliance baked in

✦ Revenue base to fund AI R&D

Upstart Advantages

✦ No legacy code or inertia

✦ AI-native architecture from day one

✦ Speed of iteration

✦ Can start with outcomes, not features

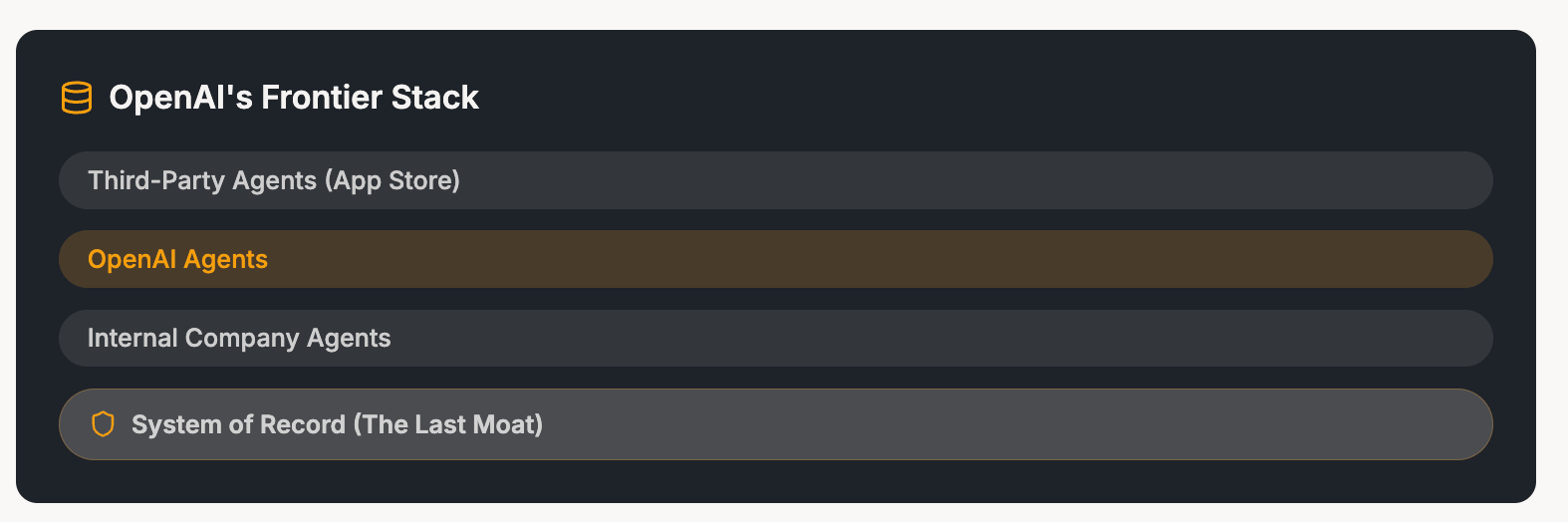

System of Record Is Oxygen for AI

OpenAI’s Frontier enterprise announcement made the stack clear: system of record at the bottom, then internal agents, OpenAI agents, and third-party agents above. OpenAI wants everything above the data layer — but conspicuously left the system of record alone. That’s not an oversight. AI agents need structured, domain-specific data to perform. Without the CRM, the EMR, the quality management system, they have nothing to work with.

But the real value goes beyond raw data. What some are calling the “context graph” — the encoded understanding of how decisions get made in a specific industry — is where durable value lives. An LLM gives you general intelligence. But you need a layer that understands what HIPAA compliance means for a medical clinic, what a takeoff means for a GC, or what FDA submission requires for a device maker. That decision layer doesn’t need a traditional UI. It could be headless, embedded in Slack, or powering autonomous agents. The form factor is secondary.

“You can’t fly a 747 through a chat box. Human nature is such that we need visual ways to consume information.”

— Nic Poulos, Euclid Ventures

UI Will Matter Less. Outcomes Will Matter More.

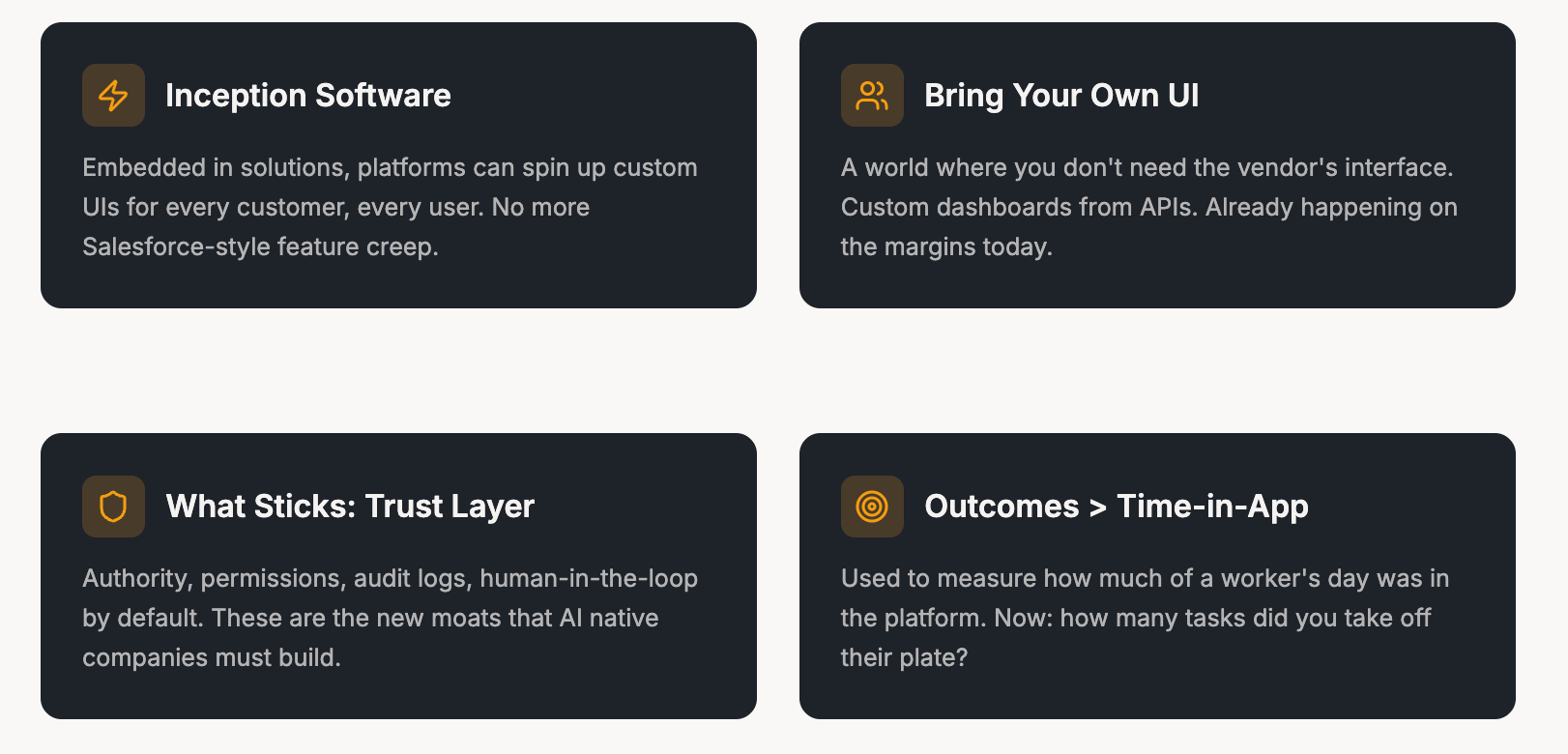

The traditional interface — buttons, forms, dashboards — is becoming commoditized. Two emerging models point to what replaces it. “Inception Software” embeds AI code generation directly into platforms, giving every customer a custom UI for their role — no more Salesforce-style feature creep. “Bring Your Own UI” goes further: fully decouple the interface, let customers build their own frontends with APIs and AI tools.

The old SaaS metric was engagement — time spent in the platform. The new metric might be its opposite: how many tasks did the platform take off the user’s plate? The best product might be one you barely interact with. But the companies that deliver autonomous outcomes without the trust infrastructure — audit logs, permissions, compliance — will hit a wall when they try to move upmarket. Requirements like these aren’t constraints. They’re the moat.

Subscriptions + Outcomes: The Winning Formula

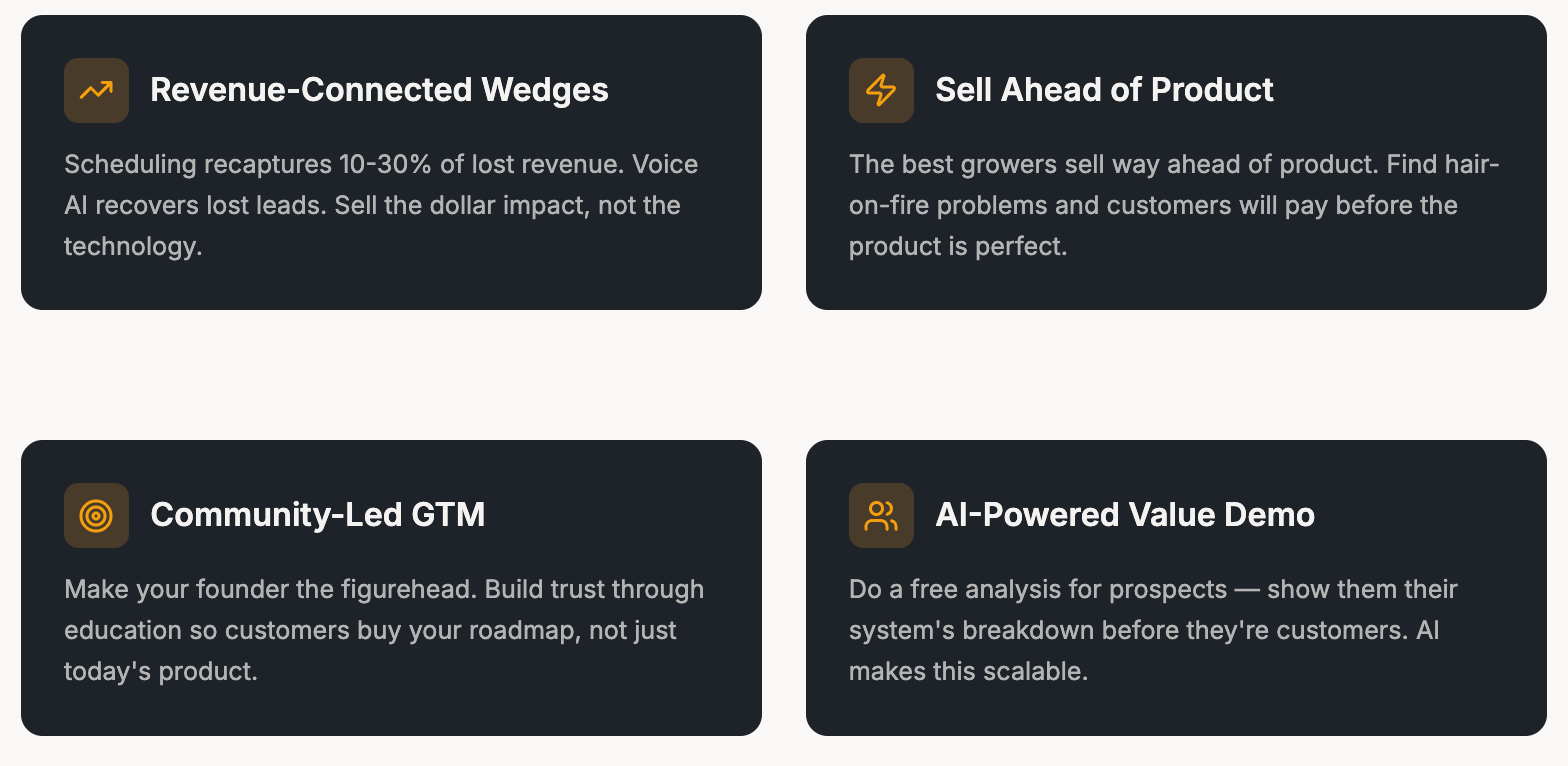

The seat-based model is under pressure, but the shift to outcomes isn’t as revolutionary as it seems — it’s a continuation of pricing evolution from platform-plus-seats to usage-based (Twilio-era) to outcome-based. The critical insight: “outcomes” doesn’t have to mean macro business results that take 12 months to measure. It can mean micro-outcomes — a generated document, an answered call, a booked meeting.

“Don’t start with ‘I’ll sell you a closed deal for $2K.’ Start with ‘What’s the value of one missed call we could answer for you?’ Break down the outcome into smaller value units.”

— Nick Tippmann· TipTop VC

Consider an AI sales agent. There are 10-30 micro-conversions in a sales process — booking, follow-up, demo scheduling, proposal generation. Start by pricing the smallest provable unit, then expand as trust builds. But a critical warning applies: without a moat — proprietary data, workflow lock-in, network effects — pricing power erodes to marginal cost as 40 other players enter with the same offering. Buyers also crave predictability; nobody wants surprise bills. The emerging consensus is a base subscription for stability, with a variable outcome layer on top.

💡 The Pricing Stack

1.Base subscription — predictability for buyer and seller

2.Variable outcome layer — start with micro-outcomes, expand as trust grows

3.Moat determines margin — without defensibility, pricing erodes to input cost

Go-to-Market Playbooks That Work

There is no silver bullet. The best companies instrument their GTM engines early and treat rev ops like a product — with backlogs, priorities, and weekly accountability meetings where every channel owner reports their number. Channel effectiveness isn’t static; something crushing it today can stop working in 60-90 days. The compounding advantage goes to teams that measure and reallocate fast.

Not every fast grower is PLG. Some are hammering phones with old-school outbound. Others run forward-deployed models with six-figure ACVs. One portfolio company goes to “the random plumbing conference, the random HVAC conference” — boots on the ground. In vertical markets, most buyers below the enterprise don’t care that a product uses AI. It can even be a turnoff. They want solutions, period.

Nearly every compelling vertical AI opportunity has 5-10 credible competitors. What separates winners? Speed of land-grab, brand trust, and ecosystem lock-in. Toast won by going feet-on-the-street in Boston while competitors ran PLG. Evolution IQ spent a year with a single design partner making $35K in ARR — then built to a near-billion-dollar exit. Fast growth is great, but retention is the real question.

“Distribution matters more than ever. It can provide uniquely powerful advantages in vertical markets because they can be harder to access.”

— Nic· Euclid Ventures

The AI-Era Founder

The traditional playbook prized domain expertise above all. That’s still valuable, but the weighting has shifted. It’s arguably harder to learn how to build and scale a high-growth AI startup than it is for a 20-year industry veteran to learn the tech side. AI has been the great equalizer — everyone started as a beginner three years ago. What matters now is rate of learning, ambition, and whether you’ve been exposed to greatness before.

VCs still want a founding CTO, but formal CS matters less — especially in verticals where innovation isn’t primarily in the engineering. With AI coding tools, knowing what to build and having taste for what good looks like increasingly trumps raw technical ability. Domain expertise is needed on the team, but the domain expert doesn’t have to be the CEO.

“Having seen greatness before — the slope of learning and ambition — I place a greater emphasis on these days than pure domain expertise.”

— Nick Tippmann· TipTop VC

Fundraising Benchmarks & VC Stacks

$220K - Median ARR at Seed

Bottom quartile near zero

$2.5M - Median ARR at Series A

Up from ~$1M historically

$750K–$6M - Series A range

Bottom to top quartile

The Series A bar has risen significantly, but the dispersion is wild — some raise at $750K ARR with extraordinary growth, others need $5-6M. The existence of hyper-growth outliers ($0 to $10M in a year) has reset VC expectations across the board, making it harder for solid-but-not-explosive companies to raise. Meanwhile, AI is changing the VC profession itself: Tippmann runs TipTop as a solo GP using Affinity (CRM), Granola (notes), and Velvet FS with automated agents that handle 60-80% of what an analyst once did.

What to Remember

Have a product or service that would be great for our audience of vertical SaaS founders/operators/investors? Reply to this email or shoot us a note at ls@lukesophinos.com