Linear #185: Rule of 40 Deep Dive: Why It Still Matters, Public vSaaS R40 Analysis, How/When It WILL Impact You

One vSaaS breakdown. One biz story. One 'how to'. In your inbox once a week.

Today’s newsletter is sponsored by Xplor Pay. Launching embedded payments is a major milestone, but it’s only the beginning of the opportunity. Many software companies see merchant adoption plateau after launch, not because of their technology, but because they stop investing in their payments business.

Built from firsthand experience growing and scaling more than 20 vertical SaaS platforms, this article explores what high-performing software companies do differently to increase merchant adoption, convert existing customers, and create long-term enterprise value. Read the article here.

Alright, let’s get to it…

The Rule of 40

I’ve become more of a fan of the rule of 40 recently.

I just think it’s a good north star metric for most companies.

It was popularized by Brad Feld around 2015 and quickly became the single most-cited operating benchmark in public SaaS. The appeal is its honesty: it forces a company to declare a balance between growth and efficiency rather than hide behind either one.

If your not familiar with the rule of 40, it’s pretty simple.

Annual ARR growth %

+

Ebitda margin %=

Rule of 40

So if you grow revenue 20% YoY and you have a 10% Ebitda margin,

you’re rule of 40 would be 30. The general premise is that a healthy software business’s revenue growth rate plus profit margin should equal or exceed 40%.

Grow 40% at break-even? You pass.

Grow 10% at 30% EBITDA margins? You pass.

Grow 25% at 15% margins? You pass.

It also constrains a tempting failure mode: buying growth that doesn’t survive contact with a cost-of-capital regime. If you can’t get to 40 by combining the two, you’re either not growing fast enough to justify the burn, or not efficient enough to justify the slowdown.

For boards, it’s a clean conversation. For founders, it’s a forcing function:

How much margin am I willing to trade for this next dollar of growth?

The Rule of 40 has fallen out of love recently due to the explosive growth of so many of the AI companies, who are blitzscaling at the moment and not giving a sh*t about EBITDA margin. But all things eventually revert :-)

Why it still matters for the rest of us

Here’s the catch: very few companies are actually growing 200%+ on a meaningful base. The median vertical software company is growing 15–25% into a defined TAM with a known sales motion. For that company — the modal company — the Rule of 40 is still the cleanest way to ask “are we worth funding?”

Vertical software is different from horizontal in a few structural ways that make R40 more relevant, not less:

TAMs are bounded. You can’t out-grow gravity for long. Eventually penetration math catches you.

Customers are sticky and slow. Net retention is high but new logo growth is bounded by the pace of an industry’s willingness to adopt.

Capital efficiency compounds. Because growth is steadier, every point of margin you protect early gets re-invested at known unit economics.

Translation: if you’re a vertical software founder, the Rule of 40 is still the benchmark you’ll be measured against — on the way in by growth investors, and on the way out by strategics and PE.

Public Vertical SaaS Analysis: The Rule of 40 Tells Us A Lot Of Biz Stories About Efficiency and Growth

I analyzed public vertical software companies to get a sense of where there Rule of 40 stands. The results, were, well, suprising…

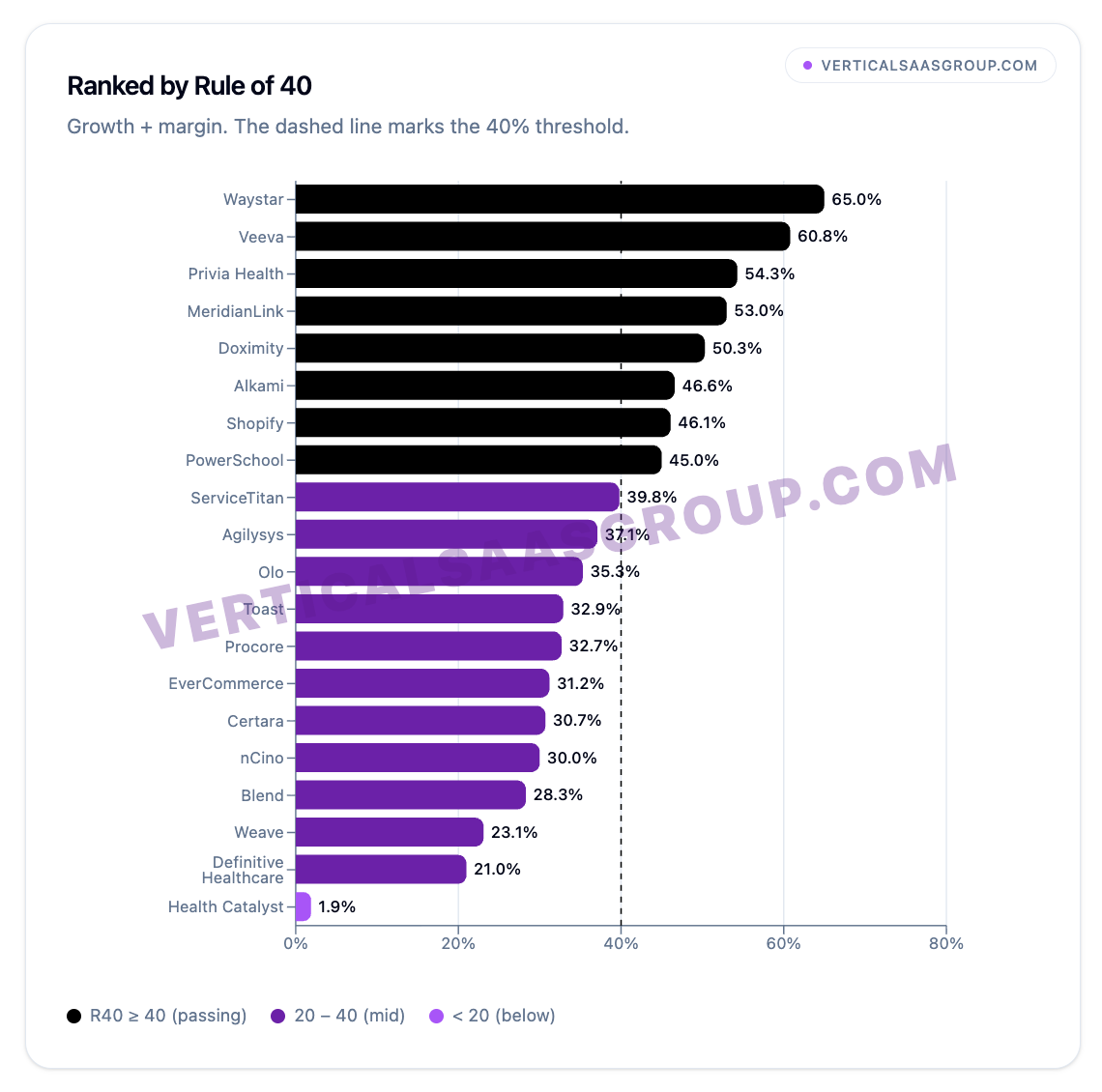

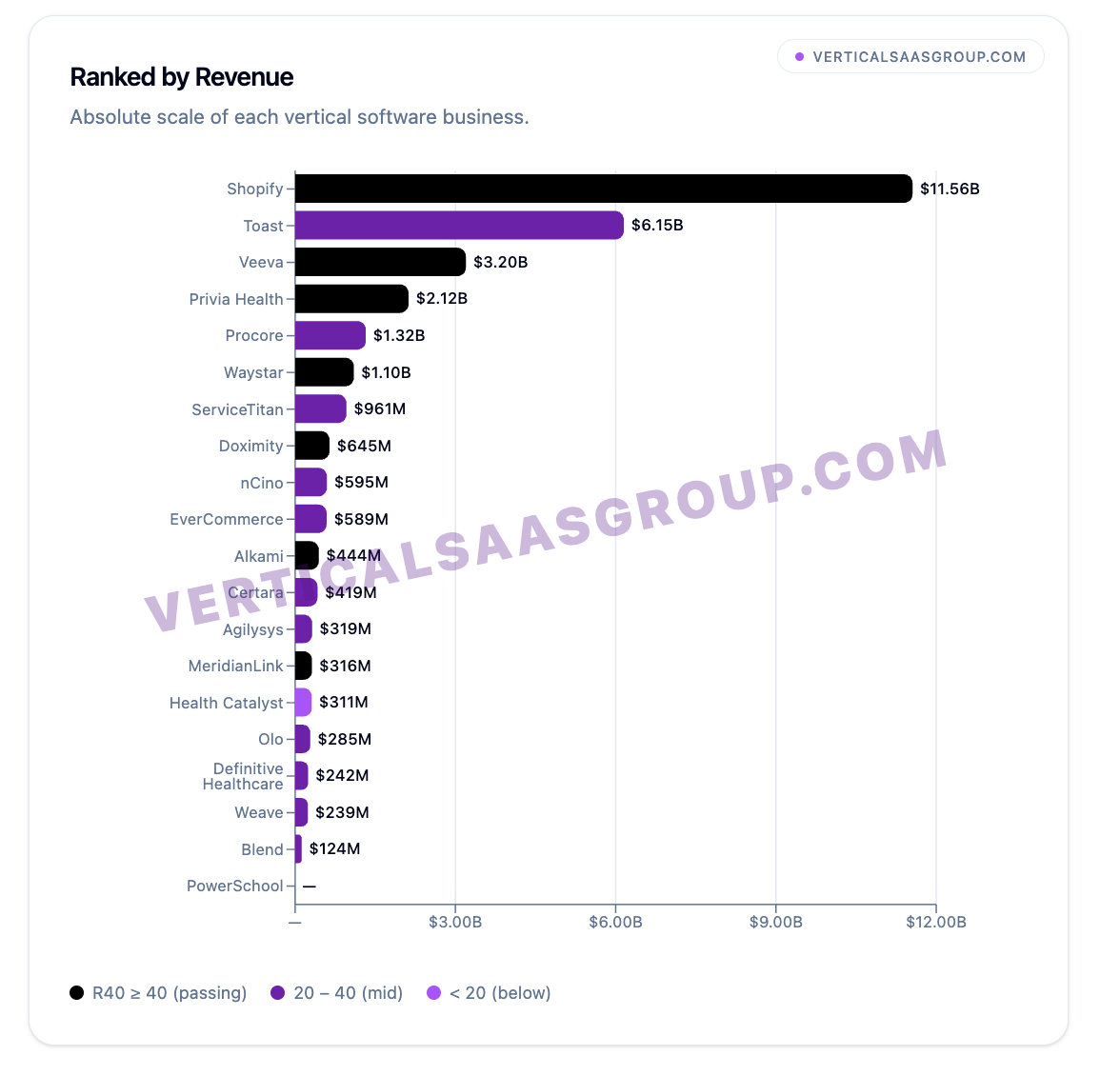

Below are 20 public vertical software companies ranked by Rule of 40, using each company’s preferred margin metric (adj. EBITDA or non-GAAP operating margin).

Waystar, Veeva, and Privia Health sit at the top — all healthcare-adjacent, all proving that deep vertical workflow lock-in supports both growth and margin. Note the dashed 40% line: nine of these twenty companies clear it, which is better than many horizontal SaaS baskets. The bottom of the list (Definitive Healthcare, Health Catalyst) shows what happens when a vertical data or analytics company’s growth stalls before costs normalize: you’re left with decent margins but a shrinking top line.

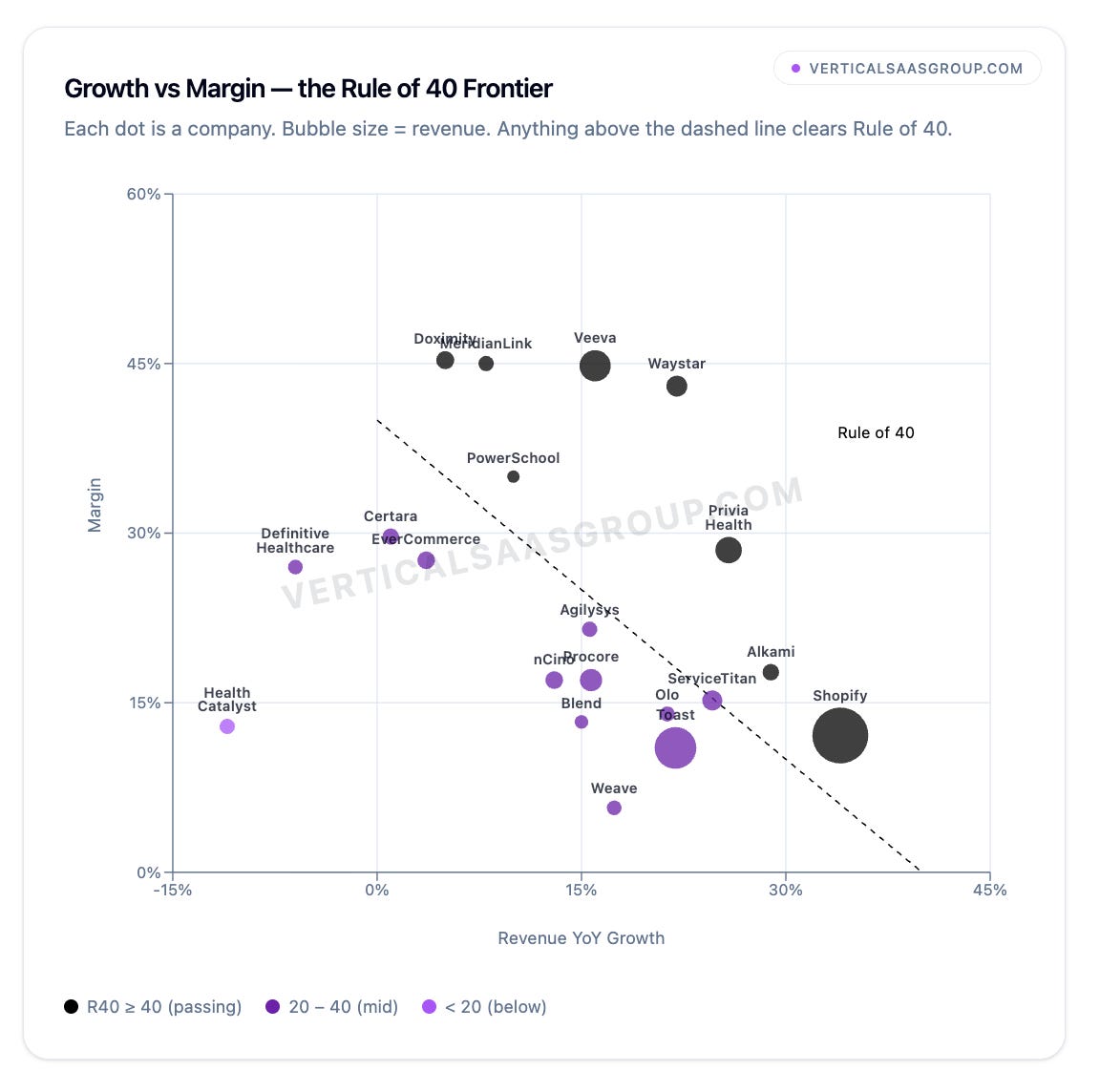

This is the most honest view. The dashed diagonal is the Rule of 40 frontier — anything above it passes. Notice the two tribes: margin engines in the upper-left (Veeva at 45% margin, 16% growth; MeridianLink at 45% margin, 8% growth) and growth engines in the lower-right (Shopify at 34% growth, 12% margin; Alkami at 29% growth, 18% margin). Bubble size maps to revenue scale, which is why Shopify's dot is enormous despite modest margins. The danger zone is the muddy middle near the origin: companies that are neither growing fast nor printing cash. That is where multiples get compressed.

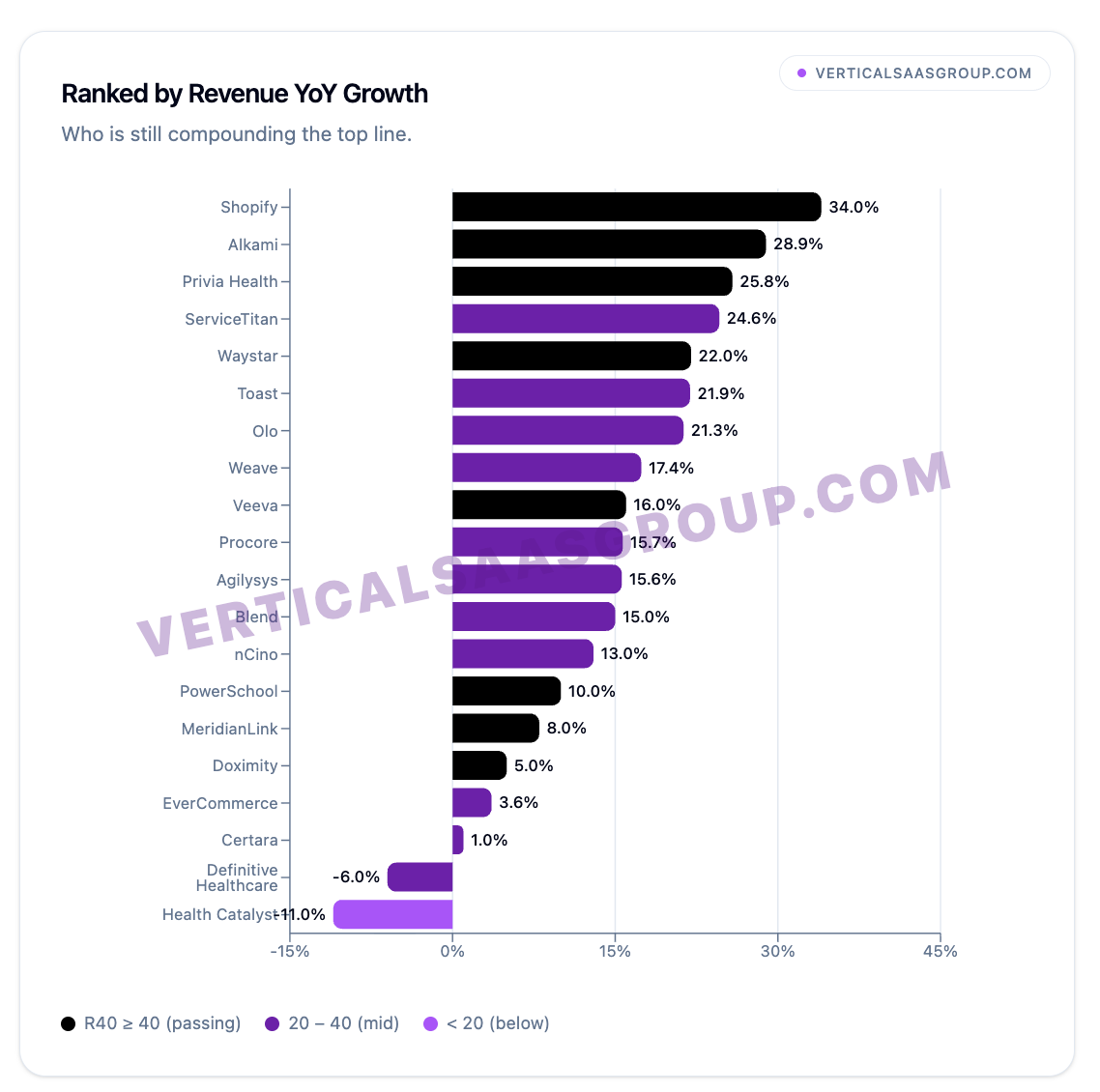

Shopify and Alkami are the only companies on this list still growing near 30% year-over-year at public scale. That is hard to do in vertical software. Most of the group is compounding at 10–25%, which is perfectly healthy for a business with 110%+ net revenue retention. What should worry founders: if your vertical SaaS is growing sub-15% and you’re not yet at $100M ARR, you may be under-penetrating the market rather than maturing into it. Growth is a choice until it isn’t.

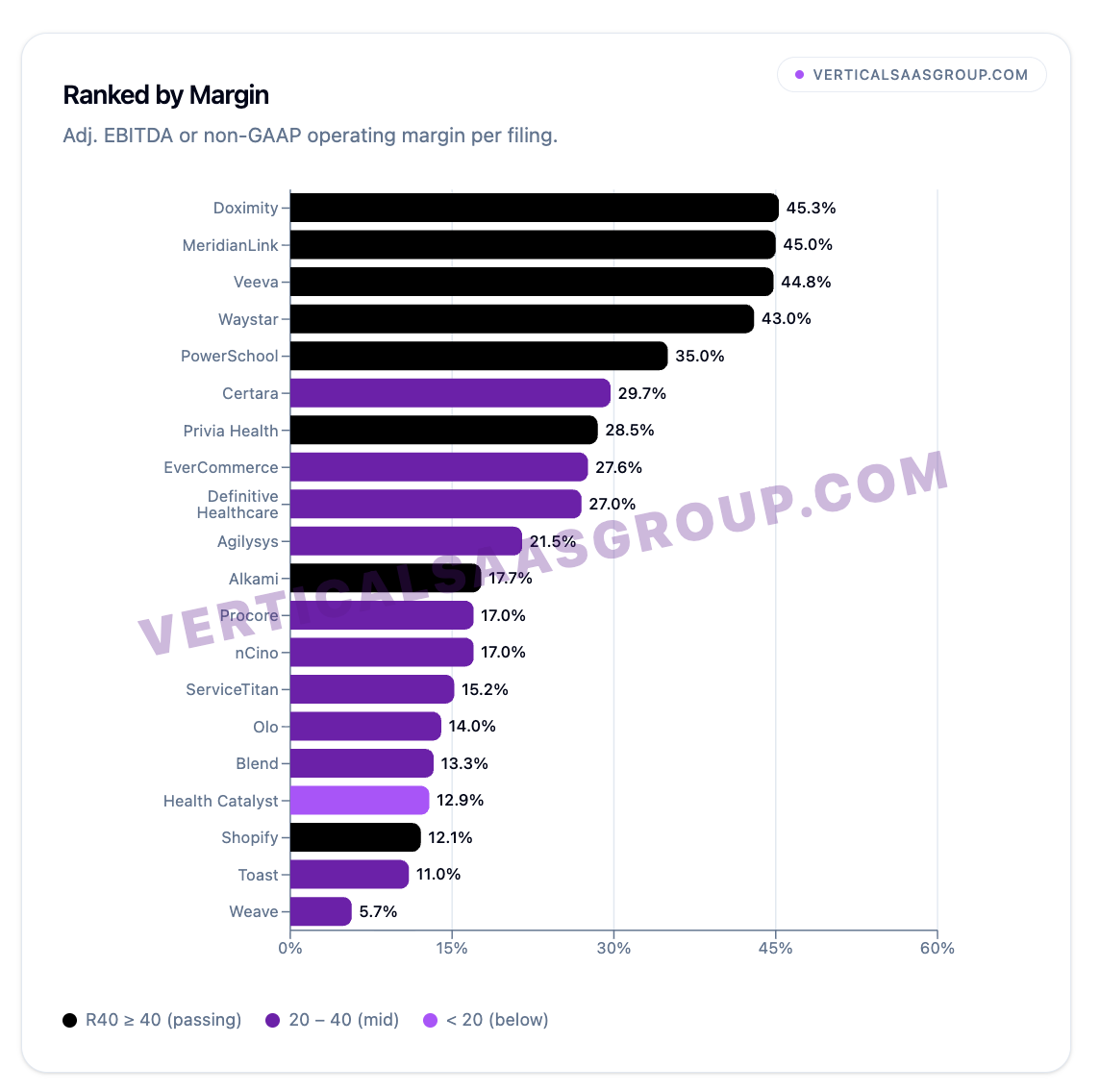

Doximity, Veeva, and MeridianLink all post 45%+ margins. The common thread? Low customer acquisition cost, high net retention, and pricing power inside a regulated vertical. If you’re building in healthcare, financial services, or another compliance-heavy industry, your margin ceiling is structurally higher than consumer-adjacent verticals like restaurants or hospitality. Toast and Shopify sit at 11–12% margins not because they are poorly run, but because their markets are volume-driven and competitive. Know which game you’re playing.

Revenue scale is not destiny, but it changes the conversation. Shopify ($11.6B), Toast ($6.2B), and Veeva ($3.2B) operate at a scale where even modest margin improvement moves hundreds of millions of dollars in free cash flow. For founders under $100M ARR, the lesson is different: don’t optimize for revenue scale until you have durable unit economics. A $300M vertical SaaS business with 45% margins (MeridianLink) is arguably a better PE asset than a $6B one with 11% margins (Toast) — depending on the buyer’s thesis and leverage capacity.

Across all five views, the pattern is consistent: the best vertical software companies find a way to be good at one axis and at least acceptable on the other. Mediocre on both is what kills valuations.

How To Internalize Rule of 40 Based On Where You/Your Company Is Actually At

The Rule of 40 is not a constant. It’s a target that should evolve with your ARR and the kind of capital you’re raising. Below is a practical guide.

$0 – $1M ARR: Don’t even compute it.

Venture track: Growth should be above 3x year-over-year. Margin is basically irrelevant at this stage. You’re validating product–market fit and proving that someone will pay.

Bootstrap track: Get to break-even as fast as possible. You don’t have a venture cushion, so every dollar of burn comes out of your own pocket or a small friends-and-family raise. Target 2x+ growth, but the real goal is proving customers stay and pay you profitably.

PE track: This is not a PE-fundable stage. Get to $5M+ ARR before you even think about it.

Watch out: Founders who “optimize for profitability” here are usually rationalizing a slow sales motion. Burn is fine; aimless burn is not.

$1M – $5M ARR: Prove the motion, not the margin.

Venture track: Target growth of 150% or more. Your Rule of 40 will be deeply negative — something like 150% growth and -100% margin — and that is exactly what investors expect.

Bootstrap track: Your R40 should be turning positive. Aim for 50%+ growth and at least break-even margins — ideally 20% growth plus 10% margin for an R40 of 30. If you’re still burning at this stage, you need a very clear path to profitability because there’s no outside capital to refill the tank.

PE track: Probably still too early for traditional PE. Growth equity may start engaging if growth is above 80% and your burn multiple is under 2.

Watch out: Beware of product-market-fit theater. High growth on a tiny base often collapses the moment you turn on a real sales team. Make sure the motion is repeatable. Not to investors, to yourself!!!

$5M – $10M ARR: First real R40 conversation.

Venture track: Aim for a Rule of 40 between 60 and 80, with growth dominant — for example, 80% growth and -20% margin.

Bootstrap track: This is where bootstrapped companies can really shine. You should ideally be at or above R40 with both growth and margin contributing — think 30% growth and 15% margin for an R40 of 45. You have no board demanding hypergrowth, so compound steadily and reinvest what you earn. The discipline of self-funding usually produces better unit economics than venture-backed peers at this scale.

PE track: This is growth-equity territory. Investors want to see R40 at or above 40 with a believable path to breakeven within 24 months.

Watch out: Unit economics become non-negotiable here. It becomes a lot harder to sell the dream if it took you a ~5 or more years to get here.

$10M – $100M ARR: The R40 sweet spot — and where most companies fail it.

Venture track: You need R40 at or above 40 with growth still above 40%. Below $25M ARR, growth should be 60% or higher; above $50M, margin in most cases should start to be flipping positive.

Bootstrap track: You’ve built something durable. Target R40 above 40 with margins driving an increasing share of the score — 25% growth and 20% margin for an R40 of 55 is a beautiful place to be. The advantage of bootstrap at this stage is optionality: you can raise venture, sell to PE, or just keep compounding. Don’t give that up by reaching for growth you can’t fund internally. You are about to become very rich :-)

PE track: Prime PE zone. Target R40 above 40 with at least 15% adjusted EBITDA margin. Rule of 40 plus 20% EBITDA is what drives the highest multiples.

Watch out: The muddy middle — 20% growth and 0% margin for an R40 of 20 — gets re-rated hard. Either re-accelerate growth or take a knife to costs.

$100M+ ARR: Durability beats heroics.

Venture track: R40 should be 40 or higher with margin at 20% or more. You may be in public-company territory but regardless you will be benchmarked against names like public vSaaS comps like a Veeva or ServiceTitan.

Bootstrap track: You’re now one of the best-owned assets in software. Target R40 of 50+ with 25%+ margins and 25%+ growth. The playbook is simple: protect net revenue retention above 110%, expand existing accounts, and acquire only when you can pay cash. You built this without venture — don’t dilute it now unless the strategic logic is overwhelming.

PE track: Target R40 above 40 with EBITDA margin of 25% or more. Multi-year visibility on net revenue retention above 110% is what unlocks premium take-private multiples.

Watch out: Pure growth narratives stop working. The market pays for compounding free cash flow, not TAM slides.

To Wrap This Up…

The Rule of 40 hasn’t been disproven; it’s been temporarily drowned out by a category of companies whose growth math makes the rule trivially true.

For the other 99% of software founders — and most vertical software founders — it remains the most honest single number to manage to. The trick is knowing which side of the equation you should be solving for, and when.

Pick a side.

Defend it with numbers.

And don’t find yourself apologizing for margin in a year or two when capital is harder to come by than it is now.

If you made it thus far, go check out the 2026 Vertical Software Summit. We’ll have 400+ vertical founders/operators/investors in Miami in November. Two days, 6+ billion dollar vertical founders. The Vertical AI event of the year.

Do me a solid and forward to a friend :-)