Linear #184: Entrata's IPO = A New Public Vertical SaaS To Study

One vSaaS breakdown. One biz story. One 'how to'. In your inbox once a week.

Today’s newsletter is sponsored by Xplor Pay. Launching embedded payments is a major milestone, but it’s only the beginning of the opportunity. Many software companies see merchant adoption plateau after launch, not because of their technology, but because they stop investing in their payments business.

Built from firsthand experience growing and scaling more than 20 vertical SaaS platforms, this article explores what high-performing software companies do differently to increase merchant adoption, convert existing customers, and create long-term enterprise value. Read the article here.

Alright, let’s get to it…

Eighteen years bootstrapped, then $507M in one round

Dave Bateman didn’t raise venture capital because he thought bootstrapping was noble. He did it because no one would give him money.

The founding: 2003, paper ledgers everywhere

Entrata was incorporated in July 2003 as Property Solutions International. The multifamily property management industry was running on paper ledgers and fragmented on-premise software held together with duct tape. Property managers tracked leases on spreadsheets. Rent collection happened by check. Maintenance requests lived on Post-it notes.

Bateman’s first company was DearElder.com, a service that automated letter delivery for missionaries. It worked. It made money. But it wasn’t big. In 2002, he stumbled into property management through a friend who managed apartments. The workflows were medieval. Bateman started building.

He taught himself to code because his developers couldn’t solve the database bottleneck fast enough. He was obsessive about architecture. Not features. Not speed. Architecture. He believed that if you built the foundation right, everything else would compound.

Most founders optimize for shipping fast. Bateman optimized for building once.

The evolution: 2015, launch of the Operating System

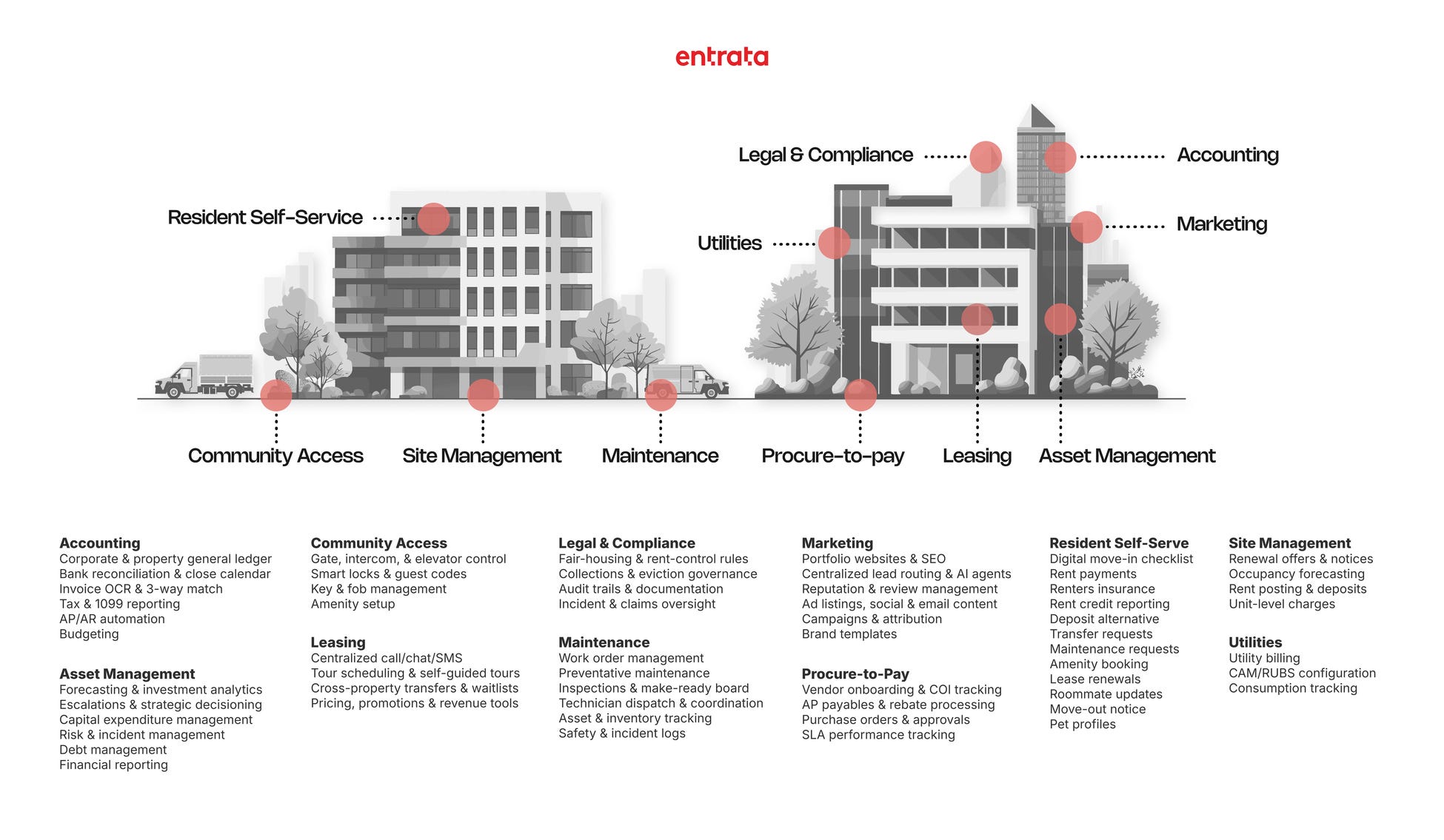

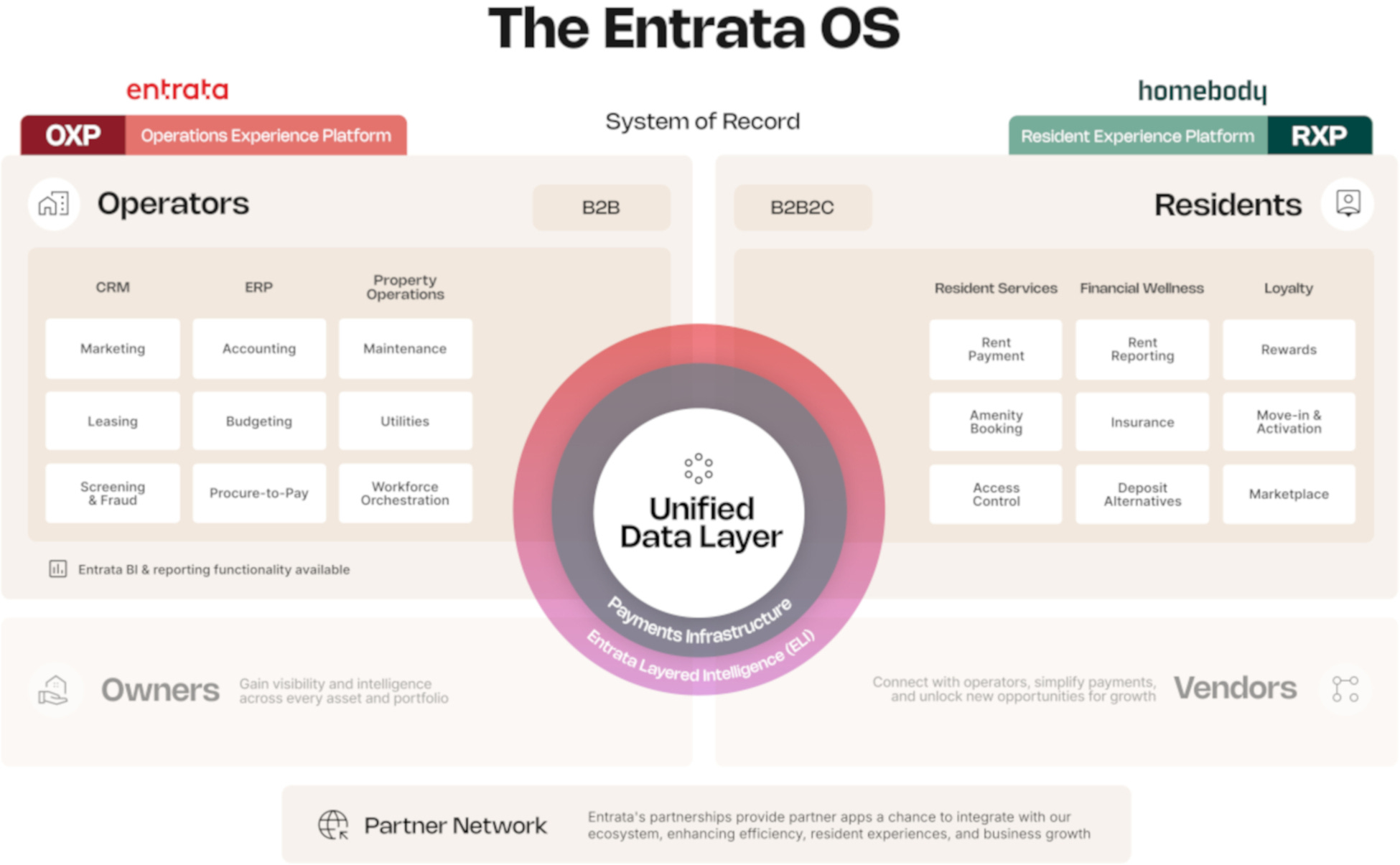

For the first twelve years, Entrata sold property management software in a fragmented market. In 2015, the company made a strategic shift that would define the next decade. They changed their name from Property Solutions International to Entrata. And they launched the Entrata Operating System.

Not a point solution. A unified, cloud-native platform with a single login and a Unified Data Layer for each customer. CRM, ERP, property operations, resident experience, payment processing, maintenance workflows. All in one system. All on one database.

Legacy providers had grown through acquisition. They’d buy competitors, bolt the products together, and call it a suite. The result was five logins, seven databases, and zero integration. Entrata built from the ground up. One login. One platform. One system of record.’

The business model: subscription plus transactions

Entrata didn’t survive on subscription revenue alone. Bateman embedded payment processing early. Operators paid a monthly subscription to use the software. But the real revenue came from processing billions of dollars in rent payments every year. By 2021, Entrata was processing over $20 billion annually.

All subscribers of the Operating System are required to use Entrata’s payment solution. That’s not optional. It’s the deal. Because rent is a recurring monthly obligation, payment volume is durable, predictable, and immune to economic cycles.

That transactional revenue created a cash flow engine that let the company grow without dilution. Subscription revenue funded operations. Payment revenue funded R&D. The dual model made bootstrapping possible.

Scaling offshore before it was cool

Bateman built a 1,200-person engineering team in Pune, India. Not because labor was cheap. Because he couldn’t hire fast enough in Utah. But offshore development doesn’t work unless someone is awake when the offshore team is working. So Bateman hired technical managers in Utah to work overnight shifts. They’d code alongside the Pune team in real time. No handoffs. No email threads. Just live collaboration across time zones. It was brutal. It was expensive. It worked.

The litigation years

For years, Entrata fought legal battles with Yardi Systems, the legacy incumbent in property management software. The details don’t matter. What matters is that Bateman was running a high-growth software company while defending lawsuits that could have killed the business. He didn’t have the luxury of raising $50M to hire lawyers. He had to win on product. So he did.

The 2021 round: $507M, first institutional dollar

By 2021, Entrata had over $200M in ARR. More than 20,000 apartment communities on the platform. Over 2,100 employees. And zero venture capital. Silver Lake led a $507M round in July 2021. Ryan Smith (Qualtrics), Todd Pedersen (Vivint), Josh James (Domo), and Dragoneer joined. It was the largest private investment round in Utah history.

Dave Bateman retained majority ownership even after the round. Kyle Paster from Silver Lake and Todd Pedersen joined the board.

Most founders raise capital because they’re out of cash. Bateman raised because the opportunity was bigger than the balance sheet.

The business didn’t need capital to survive. It needed capital to dominate. Adam Edmunds, a serial SaaS founder who had built and sold Allegiance to MaritzCX in 2014 and served as president at Podium, joined as CEO. Chase Harrington became president and COO. Bateman stayed on as chairman. The company shifted from founder-mode to scale-mode.

The leadership transition: 2022

In March 2022, Silver Lake acquired Bateman’s majority stake and took control of the company. Bateman stepped down as chairman following a public controversy in early 2022. The company moved forward under Edmunds’ leadership.

The growth phase: acquisitions and AI

In July 2023, Entrata acquired Rent Dynamics, a provider of rent credit reporting services, for up to $50M in contingent consideration. In June 2024, Entrata acquired Colleen AI, a Tel Aviv-based AI company, for $53.2M. The company wasn’t buying competitors. They were buying capabilities: credit reporting, AI infrastructure, products that deepened the platform and expanded ARPU.

The 2025 round, the dividend, and the IPO

In May 2025, Entrata raised $200M from Blackstone at a $4.3B valuation. Six months later, in November 2025, the company paid a $356.3M special dividend to shareholders, funded by cash and a $400M term loan from JPMorgan.

This is the type of activity that get a lot of PE firms in a hot water. Taking out a massive loan to pay off shareholders is typically not a loved act. The business can support it, and you know those PE investors were in year 4 of their hold and getting nervous!

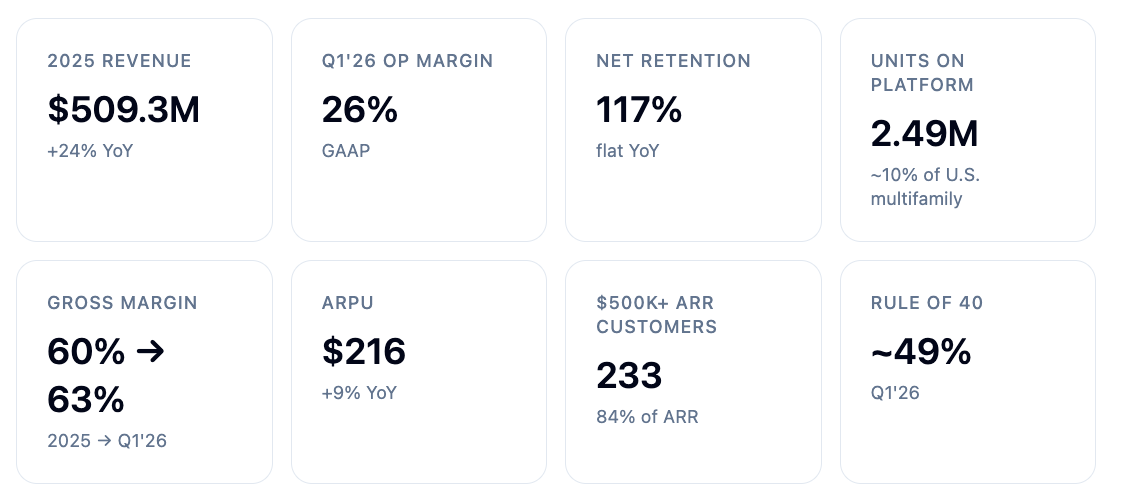

Then, in May 2026, Entrata filed to go public on the NYSE under the ticker ENT. The S-1 shows $509M in revenue, 24% growth, 60% gross margins, $50.7M in GAAP net income, and a business that powers ~2.5 million residential units — roughly 10% of the entire U.S. multifamily market.

What Entrata actually does

Entrata is a unified operating system for property management. It connects owners, operators, residents, and vendors in a single platform. The product has three layers, plus an AI engine sitting on top:

OXP (Operations Experience Platform): guided workflows for operators — CRM, ERP, property ops, leasing, accounting, procurement, vendor management.

RXP (Resident Experience Platform): the consumer-grade Homebody app. Residents pay rent, submit maintenance, manage their lease.

Payments Infrastructure: the financial layer. Rent collection, procure-to-pay, refunds, reconciliation — unified rails, settlement logic, and accounting data.

ELI (Entrata Layered Intelligence): an agentic AI engine. Essentials is free; ELI+ is the premium tier covering Leasing, Payments, Renewals, and Maintenance AI.

All three layers run on the Unified Data Layer — a proprietary database that captures real-time profile attributes, property data, behavioral signals, transactions, and workflow activity.

Go-to-market: enterprise land-and-expand

Entrata doesn’t sell to mom-and-pop landlords. They sell to enterprise operators managing thousands or tens of thousands of units — the top 50 property management companies, the REITs, the institutional owners. As of December 2025, Entrata served 4 of the top 10 NMHC operators and 10 of the top 50.

The sales motion is land-and-expand. A customer comes in on a subset of their portfolio — maybe 5,000 units — validates the product, then migrates the rest. 20,000. 50,000. 100,000. Of the 15% unit growth in 2025, 60% came from existing customer expansion and 40% from new logos. Net retention is 117%. Customers don’t just stay. They grow.

Eighteen years bootstrapped doesn’t mean eighteen years small. It means eighteen years of compounding without dilution.

By the time Entrata raised, the founder had built a business so valuable that he could take $500M+ in financing and still own the majority.

Entrata’s S-1: The Numbers That Matters

The S-1 is 230 pages. Here’s the highlights.

The ACV nobody talks about: ~$1.8M

The S-1 discloses 233 customers with $500K+ ARR driving 84% of total ARR. Do the math and the implied average contract value is ~$1.8M. That’s not a SMB SaaS number — it’s a mega-enterprise number, in the same zip code as Veeva and Guidewire, the only publicly listed vertical software companies with comparable ACVs.

Every second-order effect of a mega-enterprise motion shows up in the S-1: capital efficiency (S&M only ~13–17% of revenue), expansion (117% NRR, 97% GRR), and switching cost (3–5 year contracts with mandatory payments baked in).

Revenue: $509M and accelerating

Five-year CAGR sits around 24%. 2024 came in at $412M (~30% YoY), 2025 at $509.3M (24% YoY). Q1 2026 is $143.5M vs. $116.6M in Q1 2025 — 23% growth and accelerating margin. Worth noting: ARR growth actually re-accelerated from 22.5% in Q4’25 to 23.1% in Q1’26. Small move, big signal — most companies decelerate into an IPO.

The mix is two buckets:

Subscription-related: $437.7M in 2025 (86%). Includes monthly OS subscriptions, payment processing fees, rent credit reporting, utilities, and embedded products like insurance and resident screening.

Professional services and other: $71.6M in 2025 (14%). Implementation, training, consulting.

Payments are bundled into subscription-related. The S-1 doesn’t break it out cleanly, but they were processing $20B+ in rent annually as of 2021 — and that number has only grown.

Gross margins: Not great but expanding fast

GAAP gross margin moved 56% (2024) → 60% (2025) → 63% (Q1’26). Non-GAAP gross margin: 61% in 2025, 64% in Q1’26. Almost ten points of expansion in two years. It’s still below pure-play SaaS (80%+) — the gap is the ~15% of revenue that’s transactional (payments, insurance, screening) carrying a lower margin profile. That’s the trade-off for owning the rail.

Operating income: 26% margin in Q1 2026

Operating margin: 13% (2024) → 16% (2025) → 26% (Q1’26). Non-GAAP op margin: 23% in 2025, 28% in Q1’26. S&M dropped from 20% to 17% of revenue YoY. R&D held at 14%. G&A fell from 15% to 13%. The S-1 also shows headcount essentially flat versus 2022 — Entrata cut ~5% in 2024. Operating leverage isn’t a slide. It’s payroll.

Net income: GAAP profitable

$21.8M in 2024 (5% margin), $50.7M in 2025 (10% margin), $23.3M in Q1’26 (16% margin). GAAP. Not adjusted. Most high-growth SaaS is burning cash. Entrata is printing it.

Cash flow: strong but lumpy

Operating cash flow was $161.9M in 2024 (37% FCF margin), $100.1M in 2025 (17% FCF margin), then -$34.8M in Q1’25 and a hard rebound to $56.6M in Q1’26 (38% FCF margin). The 2025 dip was driven by changes in customer deposits, not operations. Adjusted FCF: $82.5M in 2025 (16%), $26.8M in Q1’26 (19%). CapEx of $13M in 2025. Capital-light by design — spend is people and cloud.

Units and ARPU: the two-variable growth engine

The S-1 lays out the unit count: 2.13M units (Dec ‘24) → 2.44M (Dec ‘25, +15%) → 2.49M (Mar ‘26, +12% YoY). At ~10% U.S. multifamily share (23.4M units), the TAM is ~90% unpenetrated. ARPU: $194 (2024) → $209 (2025, +8%) → $216 (Q1’26, +9%). Units growing ~13%, ARPU growing ~10% — that’s the ARR equation. Per the S-1, 60% of new units come from existing customers expanding their portfolios on the platform.

The top cohort tells the future

The S-1’s cohort disclosure is the most interesting page in the filing: the 1,000+ unit cohort hits $580 per unit annually. That’s 3x the company average and a window into where every customer ends up after a few years of attach. Entrata’s own filing says the platform replaces seven systems on average at onboarding — CRM, ERP, payments, screening, accounting, marketing, resident apps — all collapsed into one bill. That’s what’s doing the work in the ARPU number.

Customer concentration: 233 customers, 84% of ARR

Per the S-1: 233 customers with $500K+ ARR (up from 183 in 2024, +27%). Those 233 are 84% of total ARR. This is enterprise vertical SaaS — the top 50 PMCs in the U.S. are the target market. Some operators run multiple customer accounts (different portfolios, different legal entities from M&A), so the literal customer count is fuzzy on purpose.

Retention: 97% gross, 117% net

The S-1 prints gross retention at 99% (Dec ‘24) → 97% (Dec ‘25). The 2-point dip came from legacy point solutions Entrata acquired — they’re <3% of ARR but generated about half of all churn/downgrade events. Net retention held flat at 117% — the cohort of customers from 12 months ago now generates 17% more revenue. Every year, the base grows on its own.

Rule of 40: 41 trailing, ~49 forward

On a trailing basis (23.1% ARR growth + 18.3% GAAP operating margin), Entrata prints a 41.2. On the Q1’26 run-rate (23% growth + 26% GAAP op margin), you get to ~49. Both clear 40. Both are best-in-class. That’s the new minimum bar to IPO in 2026 — $500M+ ARR, accelerating, Rule of 40 compliant. The S-1 clears all three.

The competitive frame: real estate doesn’t have one winner

Here’s the uncomfortable part. The best vertical SaaS companies become the de-facto standard their industry consolidates on. In multifamily real estate, that may not be possible. RealPage ($10B+ valuation), AppFolio ($5.6B market cap), and Yardi ($15–25B private valuation) are all real. No one is getting to 30%+ share. Entrata is at ~10% and crowded at the top. The bull case is that the category is big enough that three or four winners all compound. The bear case is that nobody gets the monopoly multiple.

Debt and capital structure

As of March 31, 2026: a $400M JPMorgan term loan at 6.4%, a $75M undrawn revolver, and ~$389.6M net long-term debt. The term loan funded the $356.3M special dividend in November 2025. The IPO will partially de-lever the balance sheet but this is a recap story, not just a growth story.

Headcount, RPO, SBC

2,198 employees (including Pune) as of March 31, 2026 — that’s roughly $232K of revenue per employee. RPO of $279M (up from $272.5M at year-end), most of which recognizes within 12 months. SBC was $15.5M in 2024 and $35.0M in 2025 (7% of revenue) — the wedge between GAAP and non-GAAP op margin.

Valuation context

Entrata is targeting a $4.3B valuation at IPO. At $509M trailing, that’s ~8.4x — and ~7x forward at consensus growth. High-growth vSaaS (30%+ / 70%+ GM) trades 10-15x; profitable vSaaS (20%+ / GAAP positive) trades 6-10x. Entrata splits the middle: strong growth, expanding margin, GAAP profitable, embedded payments, AI layer, enterprise base. 8.4x is reasonable. Some of us think it’s cheap.

Entrata is not a growth-at-all-costs story. It’s a profitable, efficient, capital-light vSaaS with strong unit economics and a decade of TAM left.

Embedded payments when your customer uses ACH, not cards

Most embedded payment strategies are modeled on credit card interchange. Rent collection runs on ACH. That changes everything.

The problem

Credit cards generate 2-3% interchange. High volume, high margin, easy math. Most rent payments happen via ACH, electronic checks, or debit. Interchange is effectively zero. The traditional embedded payments playbook doesn’t work. If you’re building vertical SaaS in a category where the core transaction is ACH-heavy, you need a different model.

Entrata’s approach: fixed fees, not percentage-based

For ACH, electronic checks, and debit cards, Entrata charges a fixed per-transaction fee. Not a percentage. A flat dollar amount per payment. The only exception is credit cards, which are priced as a percentage. This does two things:

It protects margin. ACH has negligible processing cost. A fixed fee creates predictable margin per transaction regardless of payment size.

It scales with volume, not size. Rent is high-dollar but low frequency (monthly). A percentage fee would look expensive to the end user. A fixed fee feels like infrastructure.

The distribution advantage: mandatory adoption

All subscribers of Entrata’s Operating System are required to use the payment solution. This isn’t optional. If you’re on the platform, you process payments through Entrata. That means 100% attach. Zero incremental CAC to distribute the payments product. Every new customer is a payments customer. Every unit added is incremental payment volume.

If payments are optional, attach is 30–50%. If payments are required infrastructure, attach is 100%. That’s the entire game.

Revenue model: subscription plus usage

Entrata charges operators a monthly subscription fee to access the payment solution, then a per-transaction fee on every payment processed. That dual structure creates a revenue floor (subscription) and a ceiling that scales with unit count and transaction volume (usage). The subscription alone doesn’t cover cost-to-serve — but it signals payments are a core product, not a bolt-on.

Why ACH-heavy models are better than card models

Lower churn risk. Rent is a recurring human need. Payment volume is durable. Card spend is discretionary; rent isn’t.

Predictable volume. Rent is due monthly. Same cadence. Same behavior. Easy to forecast.

Higher LTV. Property managers don’t churn. Residents turn over every 12-18 months, but the building doesn’t move.

The real value isn’t the payment fee — it’s the data

Entrata records payment revenue gross of interchange and third-party fees, so the $509M includes payments to processors like Worldpay. Net take rate isn’t disclosed, but the 56% → 60% → 63% gross margin march tells you the blended economics work.

The real value isn’t the payment fee. It’s the Unified Data Layer. Every rent payment feeds Entrata’s system of record: payment history, resident behavior, lease terms, delinquency risk. That data powers the AI agents, underwriting models, the credit reporting product, and insurance upsells. Payments aren’t the end state. They’re the data-capture mechanism.

Three rules for embedded payments in ACH-heavy verticals

Make payments mandatory. Optional products have 30% attach. Required infrastructure has 100%.

Price by transaction, not percentage. Fixed fees protect margin when interchange is low.

Monetize the data, not just the fee. Payments create the system of record. The system of record creates the platform.

If you’re building vertical SaaS in logistics, healthcare billing, supplier payments, or any category where the core transaction is ACH-based — this is the playbook. Entrata just published a 230-page proof of it.

The story is that a Utah founder bootstrapped through paper ledgers, lawsuits, and an entire generation of VC fashion — and built one of the cleanest vertical SaaS businesses going public this decade.

If you made it thus far, go check out the 2026 Vertical Software Summit. We’ll have 400+ vertical founders/operators/investors in Miami in November. Two days, 6+ billion dollar vertical founders. The Vertical AI event of the year.

Do me a solid and forward to a friend :-)