Linear #183: The Token Uplift: Why Vertical AI Companies Can Get To A Billion Faster Than Vertical SaaS Ever Could.

One vSaaS breakdown. One biz story. One 'how to'. In your inbox once a week.

Today’s newsletter is sponsored by Xplor Pay. In the Investor-Operator Guide to Embedded Payments, Xplor Pay examines how embedded payments increasingly impacts retention, operational scalability, monetization, and long-term enterprise value across vertical SaaS.

Built from firsthand experience building and scaling more than 20 vertical SaaS platforms, the guide covers why many payment programs underperform after launch, what sophisticated investors increasingly evaluate, and how high-performing SaaS platforms operationalize payments successfully as they scale.

Download the free guide today.

Alright, let’s get to it…

The Token Uplift: Why Vertical AI companies can get to a billion faster than the Vertical SaaS ever could.

Every legacy vertical SaaS company is priced the same way, and the ceiling of every one of them is set by the same equation: average revenue per account, multiplied by the number of logos in the category, multiplied by the slice of those logos you can realistically win. The denominators are fixed by physics. There are only so many dealerships, only so many law firms, only so many school districts. When you do the arithmetic on what it takes to build a billion-dollar SaaS company in most verticals, you discover something uncomfortable: in many of them, it can’t be done from seats alone.

The old math: seats, locations, and a thin payments cut

Most people still model vertical AI like a better SaaS company. That is too small. The real prize isn’t a nicer product or a smarter automation layer or a new seat tier — it’s a new revenue architecture. Legacy vertical SaaS sold software access. AI-native vertical software can sell software access plus completed work. That one change makes the company a lot bigger, not because the market got bigger, but because revenue per customer can expand far beyond old SaaS ceilings.

For two decades, vertical SaaS has been priced the same way regardless of industry. There’s a per-seat fee (the user), a per-location platform fee (the rooftop, the office, the school), and a payments take rate bolted on once the workflow runs through the software. Toast does it for restaurants, ServiceTitan for HVAC, Procore for construction. The model is so standardized you can sketch the cap table on a napkin.

The constraint is brutal and arithmetic. There’s only one equation that really matters: Revenue = number of customers × annual revenue per customer. Most founders obsess over the first half — logos. The better founders obsess over the second half — ARPA (Annual Revenue Per Account, the average dollar value a single customer contributes over a year). If your average customer pays you $10,000 a year, a billion-dollar revenue company requires 100,000 logos. In most verticals, 100,000 logos is more than the entire addressable market. The reason every legacy SaaS deck eventually pivots to “expansion into adjacent verticals” is not ambition — it’s that the original TAM mathematically can’t get them there.

Historically, there was only one way to raise ARPA: find more seats or build more products. Embedded payments helped — a 30 bps take on the GMV flowing through your invoicing module can meaningfully lift ARPA without selling another seat. But payments are a rate, not a workflow — they don’t actually do anything for the customer that a generic processor wouldn’t. They’re an attach, not a product. And critically, the cost center they sit on top of is transaction fees, which is a small line item compared to the one AI is about to attack: labor.

The new math: sell the work, not the chair

A seat-based SaaS company gets paid when a human logs in. An AI-native company gets paid when work gets pushed through the system. That means revenue can scale with task volume, not just headcount — and that distinction matters enormously in verticals, because verticals are full of repetitive, measurable, high-value work.

Vertical AI keeps the seat fee and the payments line, and adds a third revenue line that didn’t exist before: AI credits, charged for the work the software actually does. Calls handled. Documents reviewed. Lessons generated. Clinical consults delivered. Claims processed. Follow-ups completed. The credit line is metered, it scales with usage, and crucially, it replaces a labor budget that is orders of magnitude larger than the software budget it sits next to.

Embedded payments helped the first generation of vertical SaaS lift ARPA. AI credits do the same thing — against a much larger cost center. That’s the token uplift, and it’s why the next generation of vertical software needs far less market penetration to build billion-dollar businesses.

The pricing instinct most founders get wrong: they compare an AI product to legacy SaaS comps and end up too cheap. The right anchor isn’t CRM pricing or document-management pricing — it’s payroll, outsourced services, error reduction, and throughput. A dealership AI that recovers missed service appointments shouldn’t be priced against a CRM seat. A legal AI that absorbs chunks of junior-associate time shouldn’t be priced against a case-management subscription. Wrong comparison set, wrong company.

Below, four head-to-head examples. Same verticals. Same buyers. Different unit economics.

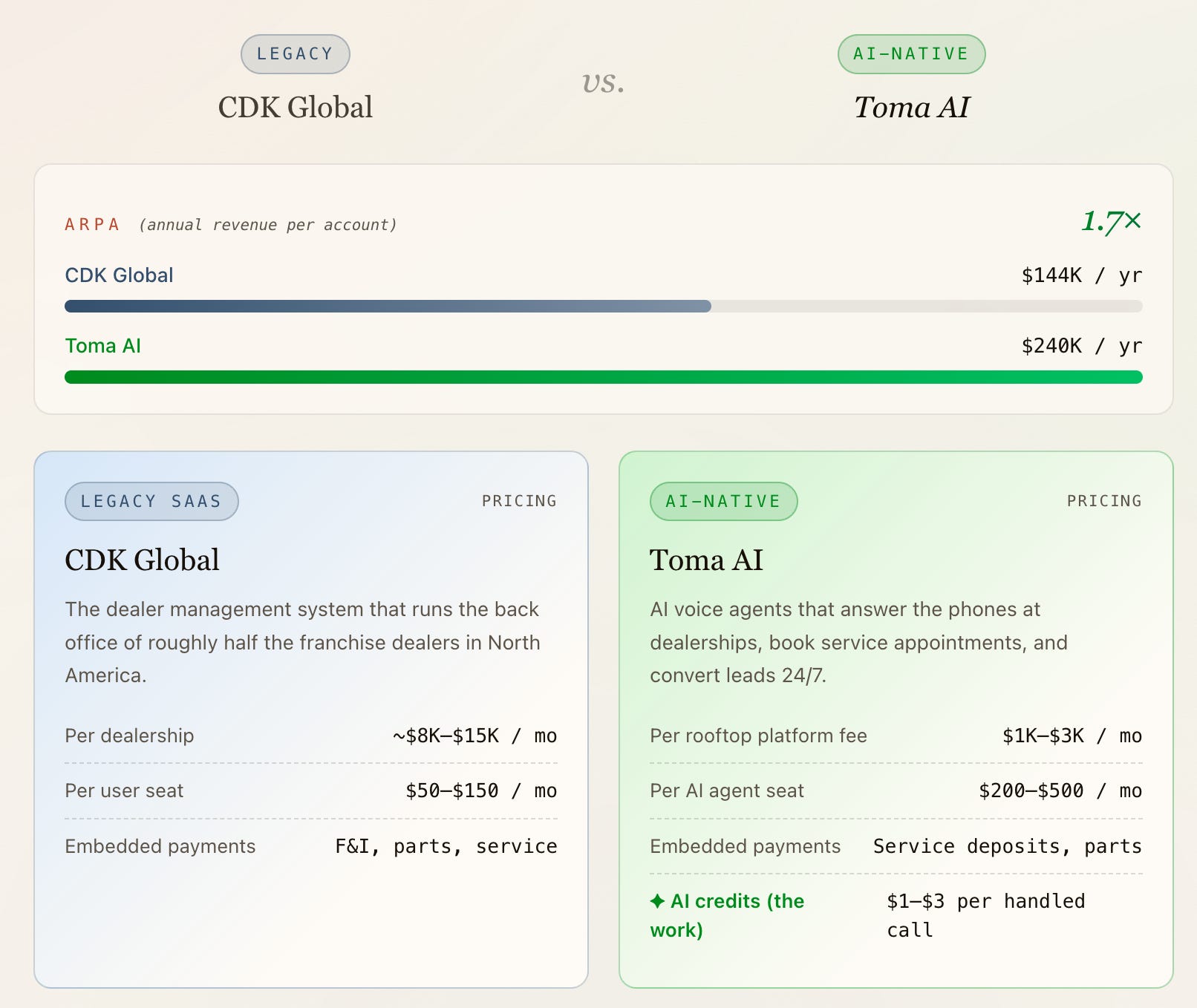

Case Study #1: Car Dealerships

Labor Bridge & AI Average Revenue Per Account Origin:

A typical franchise dealer staffs ~10 BDC + service advisors at a ~$60K fully-loaded comp — roughly $600K of annual labor on inbound calls and scheduling. Toma’s $240K AI ARPA represents capturing ~40% of that single labor line.

Addressable Labor: ~$600K / yr per dealer (BDC + service-advisor phone & scheduling labor)

AI Capture: ~40%

Target AI ARPA: $240K / yr (1.7× vs. legacy)

Market: ~16,800 franchise dealers in the US

Legacy path to $1B —At ~$12K/mo all-in ARPA, a billion of ARR requires ~6,950 dealers — roughly 41% of every franchise rooftop in America.

AI-native path to $1B —At a blended $8K/mo subscription + $12K/mo in AI call credits (a busy store handles 4,000+ inbound calls a month), ARPA approaches $20K/mo. A billion in ARR comes from ~4,200 dealers — about 25% of the market.

Toma is selling the BDC headcount, not the software seat. The AI credit line is bigger than the SaaS line within 12 months of go-live.

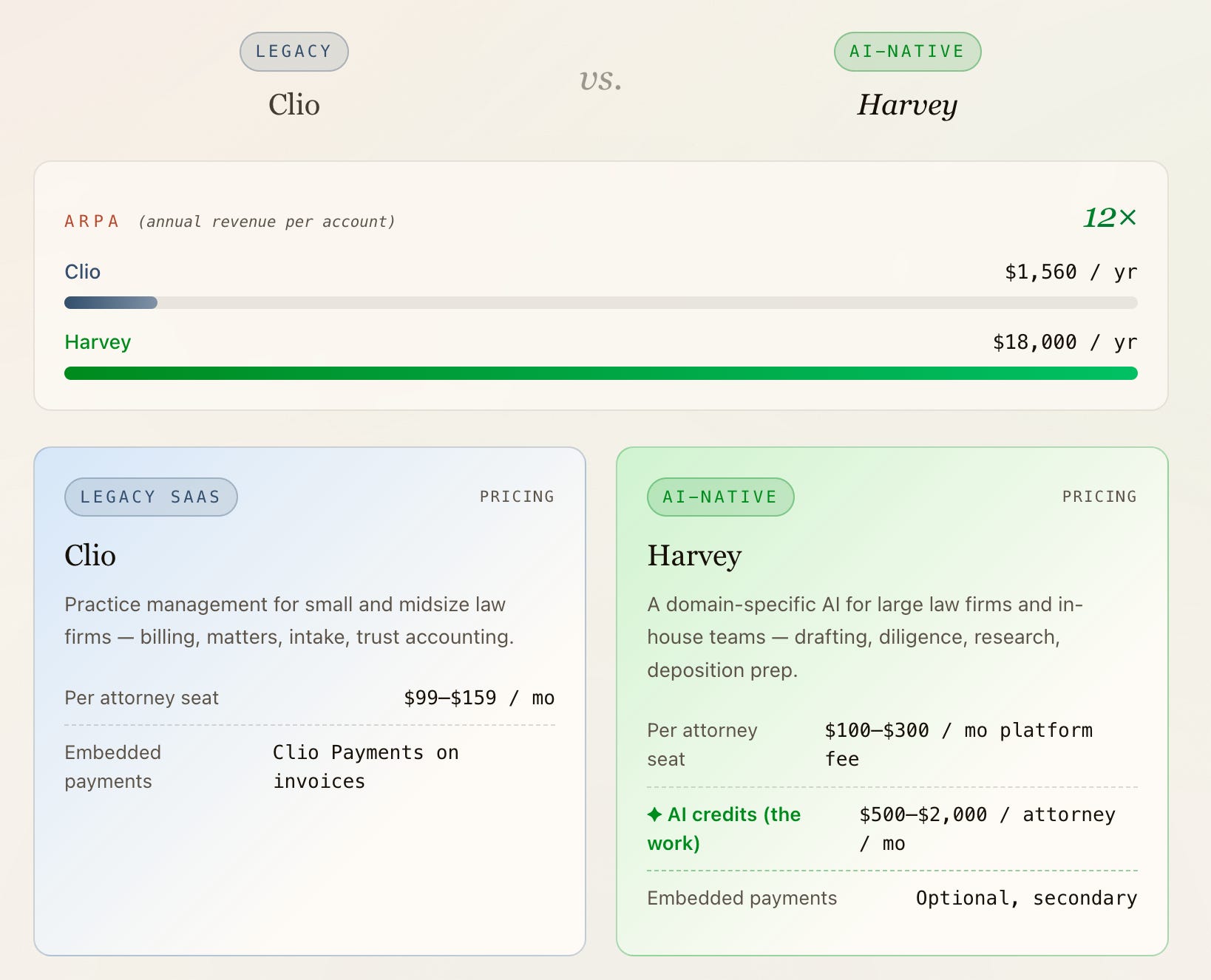

Case Study #2: Legal

Labor Bridge & AI Average Revenue Per Account Origin

A mid-level associate bills out near $400K/yr; ~$150K of that is the drafting, diligence, and research workload AI can now absorb. Harvey’s $18K/attorney/yr is ~12% of that addressable wedge — and still cheaper than the alternative.

Addressable Labor: ~$150K / yr per attorney (AI-addressable) (Junior-associate drafting, diligence & research time)

AI Capture: ~12%

Target AI ARPA: $18,000 / yr (12× vs. legacy)

Market: ~1.33M licensed attorneys in the US

Legacy path to $1B —Clio’s blended ARPU sits near $130/mo, or ~$1,560/yr per seat. A billion of ARR requires ~640,000 paying attorneys — nearly half of every lawyer in the country.

AI-native path to $1B —Harvey’s blended take is roughly $1,500/attorney/mo once credits ramp ($18K/yr). A billion of ARR comes from ~55,000 attorneys — about 4% of the market, and concentrated inside the AmLaw 200 where adoption is already mid-double-digits.

The same lawyer who paid $1.5K/yr for a practice tool now pays $18K/yr for an associate that doesn’t sleep. Same logo, 12× the revenue.

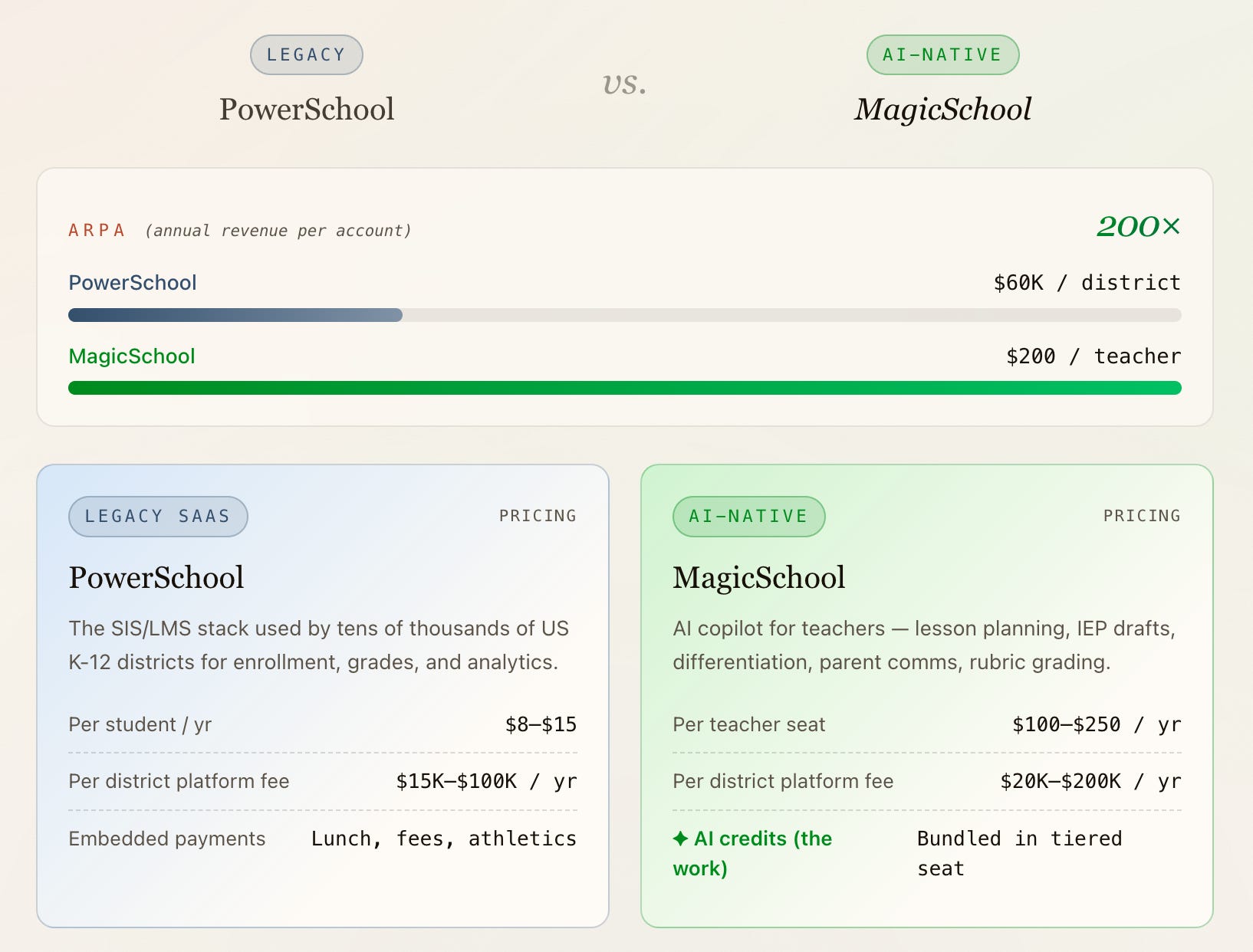

Case Study #3: Education

Labor Bridge & AI Average Revenue Per Account Origin:

Average US teacher comp is ~$66K, and ~$20K of that is the prep, grading, and IEP/comms work AI can offload. MagicSchool’s $200/teacher/yr captures only ~1% of that today — the runway up to even 5% capture is a 5× ARPA expansion before they touch a new logo.

Addressable Labor: ~$20K / yr per teacher (AI-addressable) (Teacher prep, grading & differentiation hours)

AI Capture: ~1%

Target AI ARPA: $200 / teacher (200× vs. legacy)

Market: ~13,300 US public districts · ~3.8M public school teachers

Legacy path to $1B —PowerSchool sells the district, not the educator. At ~$60K/yr per district ARPA, a billion of ARR requires ~16,700 districts — more districts than exist in the United States. Hence the international and higher-ed expansion.

AI-native path to $1B —MagicSchool can sell every teacher in a district. At $200/teacher/yr fully loaded, a billion of ARR requires ~5M teachers globally — or ~1.3M US teachers, ~35% penetration of US public school teachers. The unit is 50× bigger than ‘one district’.

Legacy SIS hit a ceiling at the number of districts. AI flips the denominator from buildings to humans, and humans are 200× more numerous.

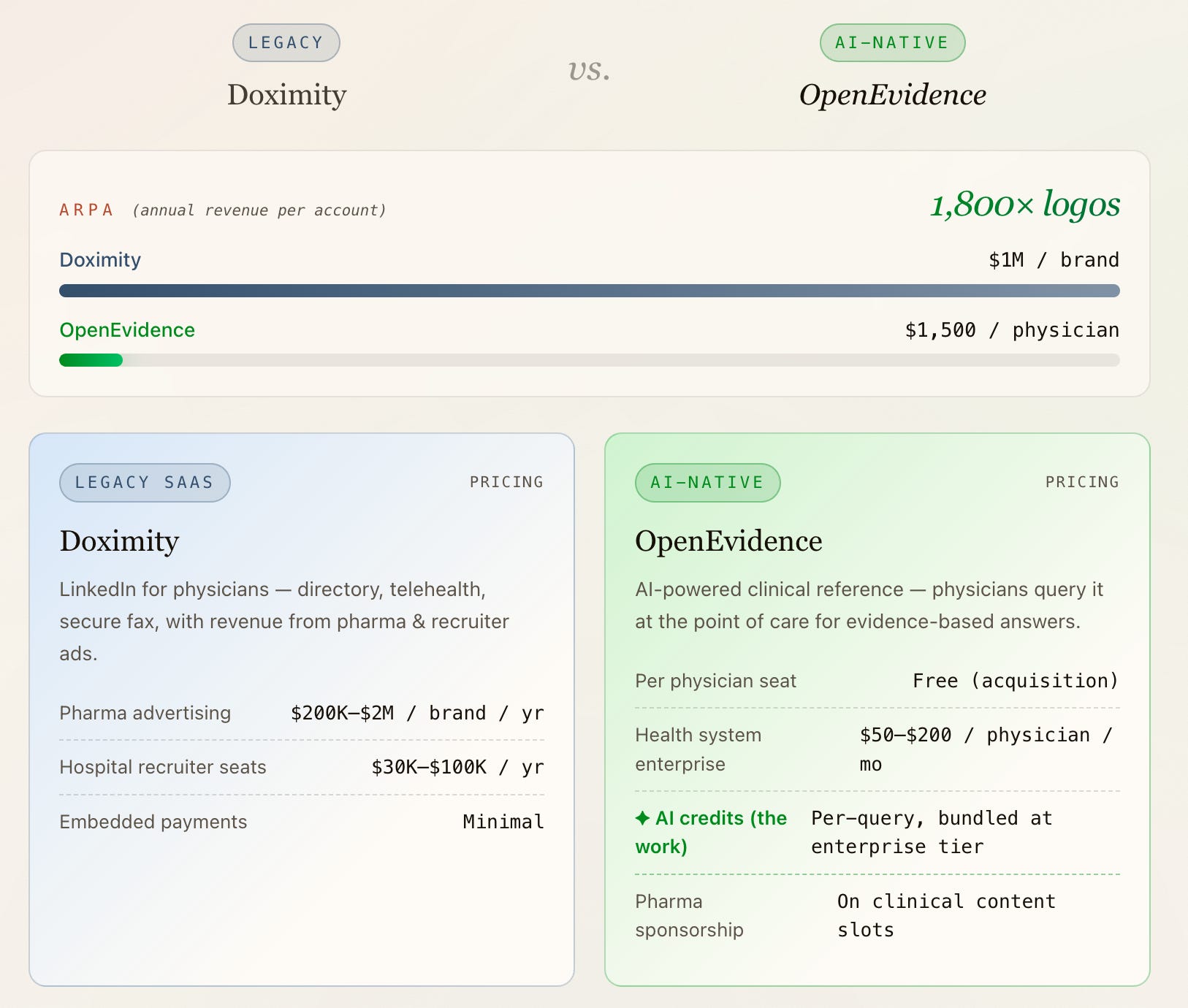

Case Study #4: Healthcare

Labor Bridge & AI Average Revenue Per Account Origin:

Average US physician comp is ~$350K, and ~$40K is the literature search, chart synthesis, and point-of-care decision work AI can absorb. OpenEvidence’s $1,500/physician/yr is ~4% of that line — and unlocks a malpractice-avoidance multiple on top.

Addressable Labor: ~$40K / yr per physician (AI-addressable) (Clinical research, chart synthesis & decision-support time)

AI Capture: ~4%

Target AI ARPA: $1,500 / physician (1,800× logos vs. legacy)

Market: ~1.1M practicing US physicians

Legacy path to $1B —Doximity’s revenue model is concentrated: ~600 pharma brands × ~$1M ARPA = bulk of revenue. A billion requires capturing roughly the entire top-of-funnel pharma marketing wallet.

AI-native path to $1B —OpenEvidence at $1,500/physician/yr enterprise pricing needs ~660K physicians — ~60% of US doctors, achievable because the product is used several times per shift and ROI is measured in avoided malpractice. Adoption already exceeds 40% of US clinicians.

Doximity monetized the doctor’s attention once a quarter. OpenEvidence monetizes the doctor’s decisions every hour.

The Vertical Software Summit Is Back!

This is the LAST day for early bird tickets. Price goes up tomorrow.

Hear biz stories from 6+ billion dollar vertical ai Founders+CEO’s

We are already 50% booked and still ~4 months from the Summit!

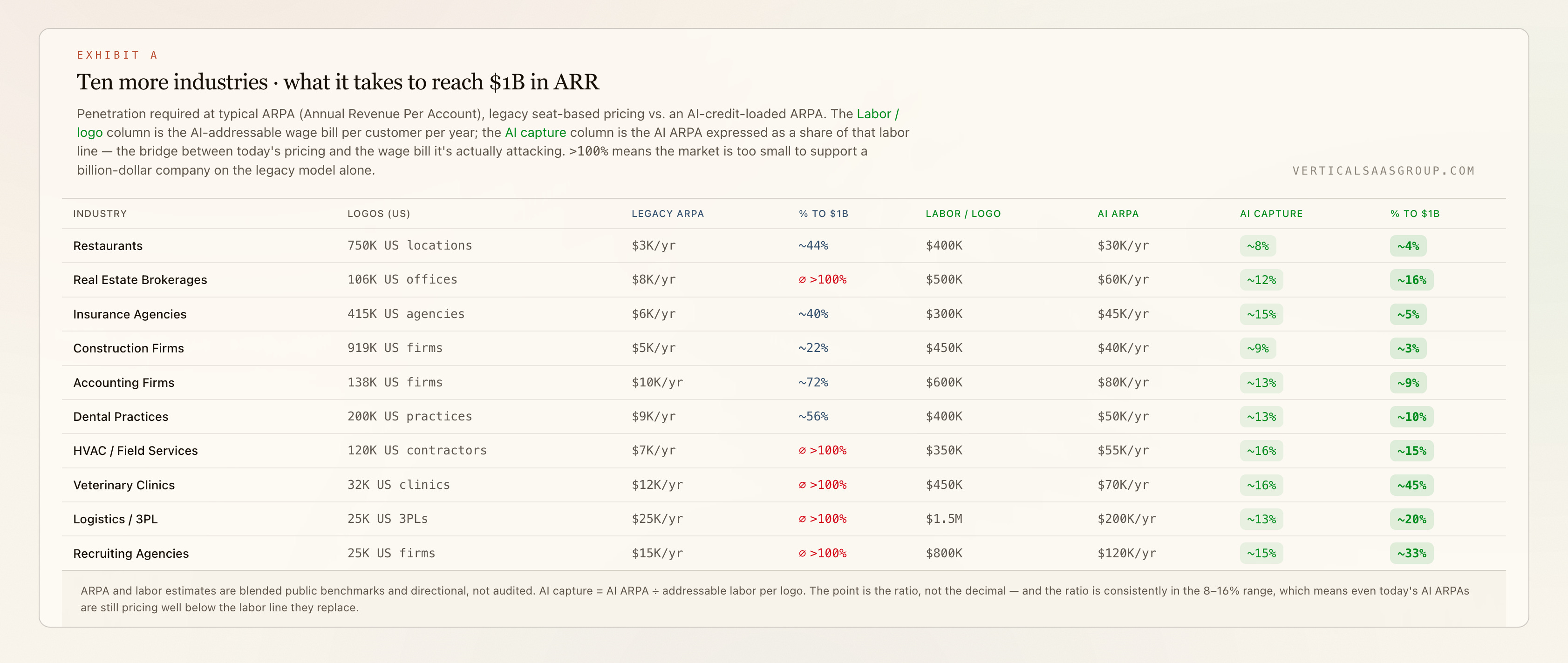

The chart: ten more industries, same pattern

The four deep-dives aren’t outliers. Run the same math across any vertical with a meaningful labor line, and the legacy SaaS model either requires a mathematically impossible market share or a forced expansion into adjacent categories. The AI-credit model collapses the required penetration into the low single digits — sometimes the low double digits in tiny markets, but always a fraction of what the seat-only model would have needed.

The pattern is consistent: wherever there’s a repetitive, measurable, expensive human task — claims adjudication in insurance, intake and routing in home services, lesson generation in schools, clinical synthesis in medicine — the labor line is 10× to 50× larger than the software line that currently serves it. Whoever turns that labor line into a metered work unit captures a multiple of the legacy ARPA.

What this changes

The best AI-native companies don’t need to win the whole stack first — they just need to win one expensive work loop. Toma doesn’t need to replace CDK Global to become important; it only needs to become the default layer for one painful, recurring, high-value job: handling inbound demand that human teams consistently drop.

Once that wedge works, every adjacent workflow carries its own AI work revenue. Harvey doesn’t need to become the operating system of every law firm on day one — it only needs to become indispensable in enough substantive workflows that firms start budgeting for AI output, not just AI access. MagicSchool doesn’t need to replace PowerSchool; it needs to own a growing share of teacher and administrator workload.

The seat license was a proxy for value when the software made the human faster. AI credits are not a proxy — they’re a direct claim on the wage bill. That shift moves the ceiling of every vertical software company from “how many seats can we sell” to “how much of the work can we do.” The second question has a much larger answer.

The companies that will compound the fastest from here start with embedded payments and a tight seat — because that’s how you earn the right to be in the workflow — and then expand the credit line until it dwarfs the subscription. Legacy vertical SaaS made money by becoming the system a business used. The next generation will make far more money by becoming the system that actually gets the work done. If AI only makes software better, you get a better SaaS company. If AI makes software billable against labor, you get a much bigger one.

That’s the whole game.

It’s time to ask yourself a very important question…

Which game are you playing?

Do me a solid and forward to a friend :-)