Linear #182: The Software Survival Map, Who Is In The Kill Zone Of The Model Companies?

One vSaaS breakdown. One biz story. One 'how to'. In your inbox once a week.

Today’s newsletter is sponsored by Xplor Pay. In the Investor-Operator Guide to Embedded Payments, Xplor Pay examines how embedded payments increasingly impacts retention, operational scalability, monetization, and long-term enterprise value across vertical SaaS.

Built from firsthand experience building and scaling more than 20 vertical SaaS platforms, the guide covers why many payment programs underperform after launch, what sophisticated investors increasingly evaluate, and how high-performing SaaS platforms operationalize payments successfully as they scale.

Download the free guide today.

Alright, let’s get to it…

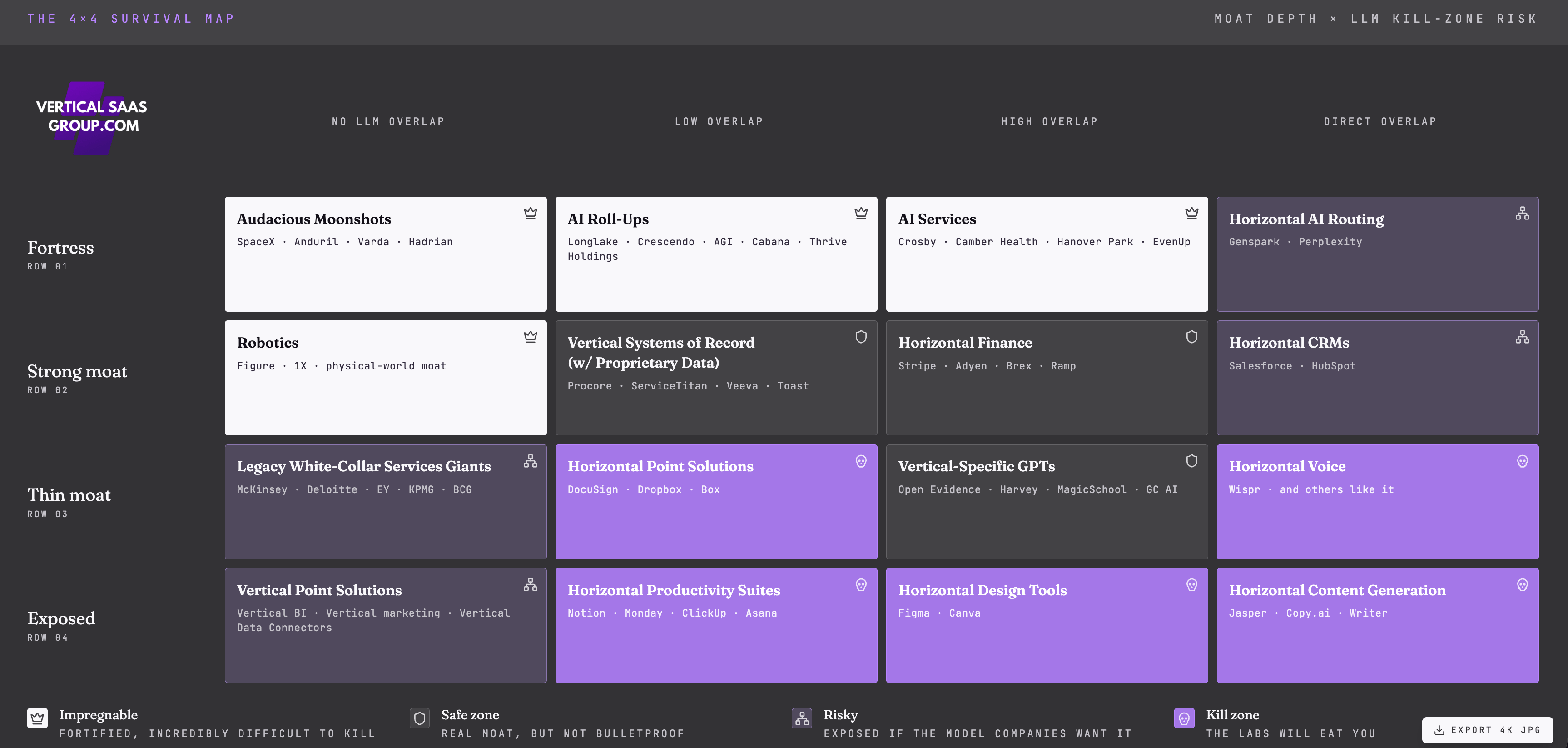

The 4x4 Survival Map — Moat Depth vs. LLM Kill-Zone Risk

Most founders are asking the wrong question about AI.

They want to know if their category will survive. They’re reading think pieces about whether LLMs will replace SaaS.

But here’s what they’re missing: LLMs are not coming for software as a category. They’re coming for specific positions on a strategic map.

This week, I’m breaking down the 4x4 Survival Map, a framework that plots software companies across moat depth and LLM kill-zone risk.

There are 16 positions on this map. Only four are fortresses.

The framework is simple. Two axes. Sixteen positions. Four survival zones.

The Y-Axis: Moat Depth

This measures how defensible your business actually is. Not how defensible you think it is. Not how many features you shipped last quarter. But whether a customer can realistically rip you out and replace you.

Row 1 is Fortress. These are companies that are fortified and incredibly difficult to kill. Network effects, workflow lock-in, regulatory capture, or physical-world integration. The deepest moats in software.

Row 2 is Strong Moat. Real defensibility, but not bulletproof. These companies have switching costs and integration depth, but LLMs can still chip away at the edges.

Row 3 is Thin Moat. Defensible today, fragile tomorrow. These companies are protected by relationships, brand, or execution, but those advantages erode fast when foundation models improve.

Row 4 is Exposed. No moat. Easily displaced by better execution, better pricing, or an AI-native competitor.

The X-Axis: LLM Kill-Zone Risk

This measures how much your product overlaps with what foundation models do natively.

Column 1 is No LLM Overlap. Your business has zero overlap with what LLMs do. Think SpaceX. Think robotics. Think businesses that live in atoms, not bits.

Column 2 is Low Overlap. LLMs touch your product, but they don’t threaten the core. Your moat is the system of record, not the features around it.

Column 3 is High Overlap. LLMs can replicate significant chunks of your value prop. You’re defensible if you own proprietary data, workflow depth, or distribution. But the clock is ticking.

Column 4 is Direct Overlap. You are basically an LLM wrapper or easily replaced by one. This is the kill zone—unless you’re routing across the labs themselves.

The map color-codes risk. The legend tells you everything you need to know. Impregnable means fortified and incredibly difficult to kill. Safe zone means real moat, but not bulletproof. Risky means exposed if the model companies want it. Kill zone means the labs will eat you.

Now let’s walk through each row.

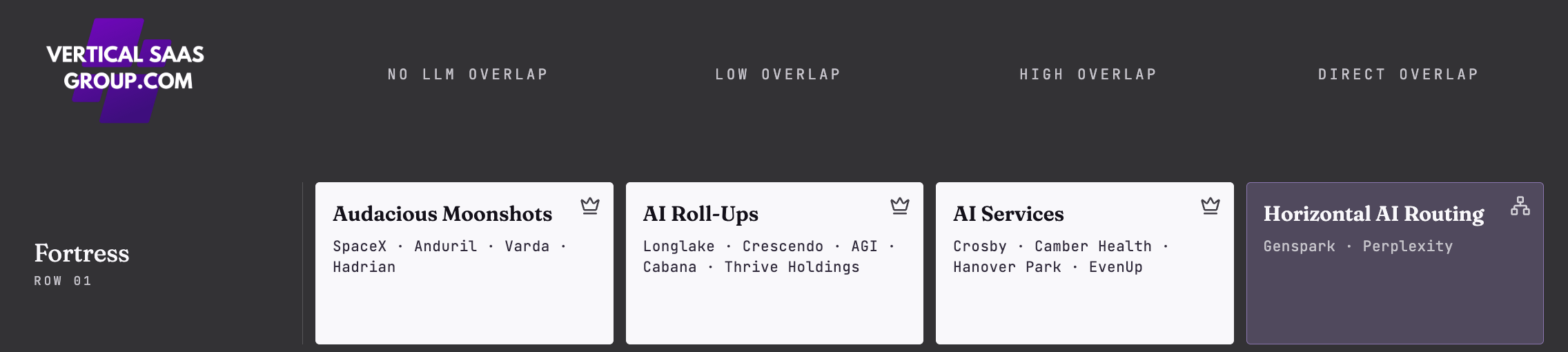

Row 1: Fortress — Impregnable and Incredibly Difficult to Kill

These are companies that LLMs fundamentally cannot displace because their moats are structural, not feature-based.

Audacious Moonshots (No LLM Overlap)

SpaceX. Anduril. Varda. Hadrian.

These businesses operate in the physical world with massive capital requirements, regulatory moats, and government contracts. SpaceX does not worry about GPT-5. Why? Because launching rockets requires billions in capital, decades of engineering iteration, regulatory approval from multiple governments, physical supply chains, and deep relationships with defense customers.

LLMs can help SpaceX engineers write better code. But they cannot replace the business. The moat is physics, capital, and regulatory capture.

If your business requires atoms, not just bits, you’re safe.

AI Roll-Ups (Low Overlap)

Longlake. Crescendo. AGI. Cabana. Thrive Holdings.

These businesses are buying services companies, then layering AI on top to improve margins. The moat is not the software. It’s ownership. You own the companies. You control the customer relationships. LLMs become a tool you deploy, not a competitor you fear.

Longlake is acquiring hoa agencies and embedding AI agents to automate as much as possible. Crescendo doing the same with call centers. OpenAI will not compete with Longlake because OpenAI does not own the agencies, the customer relationships, or the regulatory licenses.

Ownership is a great moat in the AI era.

AI Services (High Overlap)

Crosby. Camber Health. Hanover Park. EvenUp.

These companies have high LLM overlap—their product is often powered by foundation models—but they survive because they sell outcomes, not software.

Camber Health uses AI+humans to automate medical billing end-to-end. The LLM does the heavy lifting. The human gives the rubber stamp. Customers buy Camber because Camber guarantees a 95 percent first-pass claim approval rate and delivers measurable EBITDA uplift.

The moat is trust. You’re liable for the outcome. You’re embedded in the customer’s operations. You combine AI with human QA to ensure accuracy. LLMs can replicate the model. They cannot replicate the trust, the workflow lock-in, the human element, or the guarantee.

Horizontal AI Routing (Direct Overlap)

Genspark. Perplexity.

This is the one that surprises people. Direct LLM overlap, but still a strong moat. Why?

Because the routing layer is structurally defensible as long as the foundation model market stays somewhat fragmented. And the foundation model market is going to have options for a long time.

Here’s the dynamic. Most users do not want to rotate models. They do not want to remember that GPT-5 is better at code, Claude is better at writing, Gemini is better at research, and Grok is better at real-time data. They want one interface. One subscription. One product that just figures out the right model for the job.

That’s the value of horizontal AI routing. You pay a small tax to a router, and in exchange, you get access to every frontier model with the best one selected automatically based on the query.

For a lot of users, that’s worth the tax. Maybe even worth more than the tax.

The only way the routing fortress falls is if one foundation model becomes so dominant that there’s no need to route. That’s not the trajectory we’re on. OpenAI, Anthropic, Google, xAI, Meta, and emerging Chinese labs are all racing. The frontier keeps splitting across models, capabilities, and use cases.

Row 2: Strong Moat — Real Defensibility, But Not Bulletproof

Robotics (No LLM Overlap)

Figure. 1X. Physical world moat.

Robotics lives in the physical world. LLMs can help robots understand natural language and reason about tasks. But they cannot replace the hardware, the control systems, or the deployment complexity. Hardware is hard. That’s a moat.

At some point model companies will likely move into robotics, but its still far out and these companies and there investors are betting on being so far ahead, that when that time comes, it will be too late.

Vertical Systems of Record with Proprietary Data (Low Overlap)

Procore. ServiceTitan. Veeva.

This is the strongest position in SaaS. These companies own the industry-specific workflow. They capture proprietary data. They integrate deeply into business operations.

Ripping out Procore means losing construction project history, retraining every project manager, rebuilding integrations with subcontractors, and breaking reporting dashboards that run the business. The switching cost is brutal.

LLMs will make Procore better. They’ll automate RFPs and predict cost overruns. But they will likely not replace Procore.

Why? Because the moat is system-of-record status. Proprietary workflow data. Workflow lock-in. Integration depth. You are the source of truth.

It’s more likely an Vertical AI takes out procore than an LLM. They are fighting too many bigger battles to focus on anything too industry-specific.

Horizontal Finance (High Overlap)

Stripe. Adyen. Brex. Ramp.

Financial infrastructure has high LLM overlap risk because LLMs can automate reconciliation, expense categorization, and fraud detection. But these companies survive because payments create lock-in. Once you run money through Stripe, switching is painful. Once you roll out corporate cards to all your employees you don’t want to do it again.

The moat is distribution, trust, and capital relationships. Fintech survives if you own the rails, not just the workflow.

Horizontal CRMs (Direct Overlap)

Salesforce. HubSpot.

CRMs have direct LLM overlap. Foundation models can draft emails, summarize calls, update records, and predict churn. So why are they still in the strong moat category?

Data lock-in. Your entire sales history lives in Salesforce. A push to headless. Enterprise inertia means ripping out Salesforce at a 10,000-person company is not going to happen very soon. Seat licenses go down? Yes - already happening. But full churn? I dont think so.

But the moat is eroding. LLMs are making it easier to migrate CRM data. New vertical CRMs are emerging that use AI to automate data entry. The feature advantage Salesforce built over 20 years can be replicated in 6 months by an AI-native startup.

Data lock-in buys time, but not forever.

Row 3: Thin Moat — Risky and Exposed If Model Companies Want It

Legacy White-Collar Services Giants (No LLM Overlap)

McKinsey. Deloitte. EY. KPMG.

Consulting firms have no direct LLM overlap because they sell judgment and relationships. But their moat is thin. Why? Because LLMs are automating the grunt work that junior consultants used to do. Market research. Competitive analysis. Financial modeling.

The partners are safe. The $1,500 per hour strategic advice is still defensible. But the $200 per hour analyst work? That’s getting automated.

McKinsey knows this. That’s why they bought QuantumBlack and are building AI tools to augment consultants.

Horizontal Point Solutions (Low Overlap)

DocuSign. Dropbox. Box.

These companies have low LLM overlap, but thin moats. DocuSign does e-signatures. LLMs do not directly threaten that. But LLMs can automate the workflow around signatures. Drafting contracts. Extracting terms. Routing for approval.

If OpenAI builds a document workflow agent that handles the entire contract lifecycle, what is left for DocuSign? Distribution and integration depth.

Vertical-Specific GPTs (High Overlap)

Open Evidence. Harvey. MagicSchool. GC AI.

These all started as vertical wrappers around foundation models. They survive today because they tune models for specific verticals, build models that only hold industry-specific data, expand into vertical-specific workflows, and own customer relationships.

The only defensible path is to move faster than the labs in their given industry, build deeper workflow integration, expand into multi-product, and capture proprietary data. Open Evidence is doing this right. They started as a clinical decision support tool. Now they’re embedding into EHRs and capturing clinical usage data.

Vertical GPTs survive if they can continue to fine tune AI to be industry-specific, and expand their product surface area beyond GPT’s only.

Horizontal Voice (Direct Overlap)

Wispr and others like it.

Voice AI is a feature, not a business. OpenAI, Google, and Anthropic all have voice APIs. They’re near-free. If your entire product is voice interface to LLMs, you’re in the kill zone.

Row 4: Exposed — The Labs Will Eat You

Vertical Point Solutions (No LLM Overlap)

Vertical BI. Vertical marketing. Vertical Data Connectors.

These have no LLM overlap, but also no moat. They’re easily displaced by better execution or better pricing. If your only defensibility is “we got here first,” you’re exposed.

Horizontal Productivity Suites (Low Overlap)

Notion. Monday. ClickUp. Asana.

Productivity tools have low LLM overlap today, but rising risk. LLMs can generate project plans, summarize tasks, automate workflows, and draft meeting notes.

Notion is already embedding AI everywhere. That’s smart. But it also means the product layer is getting thinner. The moat becomes rip and replace. But if you can one-click move it all over to Claude that’s not a place I want to be.

Horizontal Design Tools (High Overlap)

Figma. Canva.

Generative design is real. LLMs can already generate mockups, create brand assets, and design social media graphics. Canva knows this. That’s why they bought Leonardo.ai for hundreds of millions.

The survival path is to own the creative workflow, not just the design output. Figma is trying to survive because it’s a collaboration tool. The value is the shared workspace, the version history, the comments. But what is stopping LLM’s from doing this eventually? Probably nothing.

Horizontal Content Generation (Direct Overlap)

Jasper. Copy.ai. Writer.

This is the dead zone. These companies are horizontal content wrappers. They take GPT-4, add some prompts, and charge $50 per month. OpenAI has already pretty much eaten this.

The Vertical Software Summit Is Back!

Hear biz stories from 6+ billion dollar vertical ai Founders+CEO’s

We are already 50% booked and still 4.5 months from the Summit!

Don’t miss out by grabbing tickets late :-)

How to Know If Your vSaaS Is in the Kill Zone

Most founders think they have a moat because they have customers. That’s not a moat. That’s momentum. Here’s how to assess whether your vertical software business can survive the LLM era.

Step 1: Map Your Position

Ask two questions.

First, how deep is your moat? Real moats look like network effects, proprietary workflow data, embedded fintech, regulatory compliance, physical-world integration, or system-of-record status. Fake moats are feature velocity, better UX, or being first.

Second, how much does your product overlap with core LLM capabilities? Content generation, summarization, Q&A, and basic automation are all high-overlap areas.

Plot yourself on the grid. Be honest. If you’re in the bottom-right quadrant—exposed with direct overlap—you’re in the kill zone.

Step 2: Identify Your Actual Moat

Real moats in vertical software are structural, not operational.

System-of-record status means you’re the source of truth for critical business data. Proprietary workflow data means your product gets smarter as customers use it. Embedded fintech means you control payments or financial rails. Regulatory compliance means certification or audit trails create switching costs. Network effects mean value increases with more users. Physical-world integration means hardware or supply chain dependencies. Multi-model aggregation means users pay you to abstract away a fragmented market.

Those are real moats. Feature velocity is not. Better customer support is not. Being first is not.

Step 3: Decide Your Survival Strategy

If you’re in the kill zone, you have three options.

Go vertical, fast. Horizontal content generation is dead. Vertical content generation with proprietary context and workflow depth can survive. You need to become the system of record for a specific workflow in a specific industry.

Embed into a system of record. Become a feature inside someone else’s fortress. If you can’t own the customer relationship directly, partner with someone who does.

Or sell outcomes, not software. Become an AI services business. Use the LLM as a tool, not the product. Get paid when the customer wins. Own the liability. Provide guarantees.

If you have a thin moat, deepen it. Add proprietary data capture. Build workflow lock-in. Embed payments. Get closer to the system of record. Move faster than the labs.

If you’re impregnable, stay impregnable. Do not drift toward horizontal. Do not become a feature. Protect the moat. The temptation will be to expand horizontally because the market looks bigger. But horizontal is where you die.

Step 4: Apply the “Could OpenAI Do This?” Test

Ask yourself: could OpenAI replicate 80 percent of my product with a new prompt template and a vertical fine-tune?

If yes, you’re at risk.

If OpenAI would need to acquire companies, build physical infrastructure, navigate regulation, own proprietary data, or aggregate across competing labs to compete with you, you’re safer.

The moat is not the software. The moat is everything around the software that makes it impossible to replicate. The workflow. The integrations. The trust. The liability. The outcome guarantee. The proprietary data. The multi-model abstraction layer.

That’s what survives.

What This Actually Means

The 4x4 Survival Map is not static. Companies move. Moats erode. LLMs get better. Salesforce used to be impregnable. Now it’s vulnerable. Horizontal content tools used to be venture-backable. Now they’re dead.

But the framework holds. Moat depth and LLM overlap determine survival.

Most founders are optimizing for the wrong things. They’re adding features when they should be deepening moats. They’re chasing horizontal scale when they should be going vertical. They’re building AI wrappers when they should be building systems of record or routing layers that abstract the fragmentation.

The AI era does not kill vertical software. It kills undifferentiated horizontal software with thin moats.

If you’re building in vertical software, the opportunity is bigger than ever. But you need to know where you stand. You need to map your position. You need to deepen your moat. You need to move fast.

The labs are coming. The only question is whether they eat you, ignore you, or you become their distribution.

//

So where does your company sit on the 4x4 map? Are you deepening your moat or adding features? Hit reply. I read every response.

Until next week,

Luke

Do me a solid and forward to a friend :-)

Great work on this Luke, super clear and well put together