Linear #181.5: Anti-Pedigree and notes on backing the founders the consensus market wont

One vSaaS breakdown. One biz story. One 'how to'. In your inbox once a week.

Pedigree is noise.

Evidence is signal.

Drive does the rest.

The honest version of inception-stage investing in 2026 is that the consensus market has fled to safety. The biggest funds are chasing founders who look de-risked on paper — Fortune 500 résumés, second-time CEOs, ex-FAANG operators — even though the entire historical record of venture says the largest outcomes came from young, scrappy, unfunded founders the consensus would not have touched. Gutter is built as an institutional critique of that drift. The name itself is the bet: if you’re going to call yourself Gutter, you’ve got to be good.

The first signal isn’t pedigree — it’s resourcefulness.

How much has this founder accomplished relative to the resources they actually had? The bar isn’t absolute output. It’s the ratio. A 22-year-old who bootstrapped a software business on internet-poker winnings gets credit a freshly-funded ex-VP does not. And it’s the deepest predictor in Gutter’s portfolio of who actually compounds.

The second is lifelong commitment — the founders whose attachment to the problem transcends any single company. Dan’s phrase: we couldn’t pay them not to do it. They grew up with family inside the industry, or worked in it themselves, or have been obsessed since they were a kid. That commitment is what survives a pandemic, a hyperinflation cycle, and AGI showing up mid-sprint. The cleanest pitch with the thinnest tether to the customer is the founder who quits the second the company gets actually hard.

The third is evidence density. When Gutter backtested every Elbow Grease application against which ones converted to an interview, the single dominant variable was hard evidence per word in the pitch. Named customers. Recorded calls. Specific numbers. \”We reduced X to Y for Bob, here’s his phone number, by the way Bob has a cousin Jim, and Jim uses it too.\” That is the texture of a founder who is actually customer-obsessed — and it’s almost impossible to fake against 40 hours of diligence. The rest of this issue is the operating system underneath those three.

This Weeks Vertical Titan:

Dan Teran & James Gettinger

(Co-Founder & GPs @ Gutter Capital)

Dan and James met playing rugby at Johns Hopkins and spent a decade on divergent careers before founding Gutter together five years ago. Dan was a partner at Pre Hype in New York, then founded Managed by Q — a vertical SaaS and B2B marketplace for office services — which he ran as CEO for five years before selling to WeWork in 2019 for $220M. James started a software company at 22, learned every lesson the hard way, and bootstrapped it by playing internet poker, eventually becoming one of the largest winners in online poker and DFS on sites like DraftKings and FanDuel before turning angel.

Gutter just announced Fund III — a $75M vehicle focused on the earliest stages of company building — and opened applications for the second cohort of Elbow Grease, their in-house accelerator. Cohort one funded an ex-SpaceX engineer putting satellites into very low earth orbit and Keeper Systems, AI agents for 211, the non-emergency hotline for people facing eviction or food insecurity. The Gutter HQ on Canal Street in Chinatown houses 70+ operators across 15 portfolio companies on two floors — the obstacle course Elbow Grease founders are dropped into for ten weeks.

The frame they keep coming back to: Gutter is anti-prestige to the bone. The consensus market wants founders who look de-risked on paper. Gutter wants founders who have done a tremendous amount with very few resources — the ratio, not the absolute. James calls it the most underweighted variable in venture today.

The line every founder should write on a wall: Dan and James are looking for teams they “couldn’t pay not to do it.” Authenticity is at an all-time premium. Gutter does not publish requests for startups — they don’t want founders studying to the test. The aperture is wider than the vertical-AI label suggests: if you’re doing your life’s work, they want to hear about it.

Ten moves for founders before the seed. How investors think about backing early entrepreneurs.

Operator-grade lessons for the things you’re actually deciding before your first real check — what signal beats pedigree, how to pitch with evidence density, what to send Gutter before they ask, and why doing your life’s work is now the most underpriced asset in venture.

#01. Refuse the pedigree shortcut — back the resourceful

Most VC money in 2026 still chases founders who look de-risked on paper: Fortune 500 résumés, ex-FAANG, second-time founders battle-tested by a tier-one logo. James calls it out plainly: that profile is in direct conflict with how most of the great companies actually got built. Jobs, Bezos, Gates — young, scrappy, no one would give them the time of day. The flight to safety at the top of the market has quietly left the highest-variance founders unfunded.

Gutter’s filter for signal-without-pedigree is resourcefulness: how much did this person accomplish relative to the resources they had? A 22-year-old who bootstrapped a software business by playing internet poker on the side gets credit a Stanford MBA with a $2M friends-and-family round does not. The point isn’t to fetishize struggle — it’s to underwrite a real input to outcomes that the consensus market has stopped pricing.

Action item: Stop putting your prestige logos at the top of the deck. Put a slide that shows what you accomplished per dollar and per month. If that ratio isn’t extraordinary, fix it before you raise.

#02. Lifelong commitment — “we couldn’t pay them not to do it”

Dan’s single most-used phrase for inception-stage founders: we couldn’t pay them not to do it. The best-performing founders in the Gutter portfolio carry a commitment to the problem that transcends any given company — they grew up with family in the industry, they worked in it themselves, or they have been obsessed since they were a kid. That commitment is what survives a pandemic, a hyperinflation cycle, and AGI arriving mid-sprint.

Charisma without that commitment has a short half-life. Founders who can tell a beautiful narrative but parachuted into the space last quarter tend to leave for the next hot thing the second the company gets genuinely hard. The companies Gutter has watched die were often the ones with the cleanest pitch and the thinnest tether to the customer.

Action item: Write the version of your origin story where you do not get funded — and still keep working on this for ten years. If you can’t write it credibly, you have an investor problem, not a market problem.

#03. Drive + pace of learning > airplane-test charisma

The market over-rewards founders who are charismatic and agreeable — the ones you’d want next to you on a long flight. James’s blunt observation: many of the people who have actually done it would not pass that test. What does correlate with outcome is drive (the initiation energy plus the refusal to quit the hundreds of times the ball is on the fence) and pace of learning. The job changes shape at every revenue inflection — $300K, $1M, $10M, $100M, $1B — and the founder has to change with it.

When Don Valentine first met Steve Jobs at Sequoia, he called the person who made the intro and said: don’t introduce me to more people. Jobs was not yet the CEO we remember; he became him on a 30-year journey. The Gutter question isn’t “are they great today” — it’s “are they on a trajectory steep enough that they will be”.

Action item: Track your own learning velocity. List the three biggest things you understand now that you didn’t 60 days ago. If the list is thin, your trajectory is too.

#04. Evidence density is the single biggest predictor of a yes

When Gutter backtested every Elbow Grease application against which founders made it to interview, one metric dominated: evidence density. Hard evidence per word in the pitch. Specific customer names, exact numbers, recorded calls, real testimonials — not a wall of text claiming “customers love it”. The founders who advance pile on primary evidence that they understand the space better than anyone in the room.

Dan’s mental model: “we reduced X to Y for Bob, here’s his phone number, by the way Bob has a cousin Jim, and Jim uses it too.” You pull the string and the founder keeps going. That is the texture of a founder who is actually customer-obsessed — and it’s almost impossible to fake for the 40 hours of diligence Gutter runs on each seed investment.

Action item: Read your last pitch deck and count the named customers, the specific numbers, and the exact quotes. If that count is under ten, your deck is hand-waving — go talk to fifty more people this month.

#05. Send three recorded customer calls — before they ask

Dan’s pro tip for any founder applying to Elbow Grease (or anywhere): in addition to a product demo, attach three recorded customer calls. A pitch to a non-customer. A QBR with a current customer. A feature walkthrough. They don’t need to be polished — they need to be live, dynamic, unscripted, and obviously real.

Most investors won’t actually listen to all three. But knowing they could is a different kind of signal. It tells the room you are so deep in the work that the calls are happening daily anyway, and you’re not hiding anything. In a world where every meeting is transcribed and recorded, the founders who don’t share customer interaction are the ones quietly admitting it isn’t happening yet.

Action item: Record your next five customer conversations (with permission). Pick three. Send them, unprompted, the next time an inception-stage investor takes a meeting.

#06. Judgment is the hardest signal — Elbow Grease is the obstacle course

Drive and pace of learning you can screen for in a couple of meetings. Judgment — do they have a history of good decisions, can they explain why a past mistake was a mistake, will they actually learn from it — is much harder. James and Dan can’t see it in a Zoom. So they built Elbow Grease, a 10-week accelerator inside Gutter HQ on Canal Street, specifically to put founders through an obstacle course of real decisions in the same room as 70+ other operators across 15 portfolio companies.

They watch how the founder connects with other founders. How they enlist later-stage CEOs to introduce them to customers and talent. How they handle a no-decision. “You would be blown away at how effective some of the Elbow Grease founders have been at just enlisting these much later-stage founders to do work for them — they are demonstrating their resourcefulness before our very eyes.” Demo day at the end? No. The next check comes from Gutter, or it doesn’t come.

Action item: Manufacture your own obstacle course. Spend the next month embedded somewhere that forces you into uncomfortable judgment calls weekly — a customer’s office, a peer’s company, a co-working space full of operators ahead of you.

A quick word from our incredible partner,

Parafin - the leading embedded capital partner.

4.8 star rating on Trustpilot, with over 500 reviews [source]

71% CSAT rating across all partners

84 NPS

Serving top Fortune 500 companies, including Amazon, Walmart, and DoorDash

#07. Reference founders precisely — “would I bet on them, not rehire them”

Gutter does heavy reference work — talking to dozens of people who actually know the founder. But the lesson is in how the references get interpreted. The wrong question is “would you hire this person back into the job they had?” The right question is “would you bet on them as a founder?” Dan’s own references in 2014 — pre-Managed by Q, fresh out of a paralegal job — would not have read as exceptional. They didn’t need to. Scott Belsky, Hunter Walk, and Satya Patel were betting on the founder, not the employee.

When a reference does come back mixed, the question is never “is this disqualifying” — it’s “what are the specific circumstances in which the next 18 months would be different?” References have killed plenty of Gutter processes. But they’ve killed the right ones, by being specific about context and what was actually being measured.

Action item: Pre-write the reference questions you want investors to ask about you. Make them specific: founding context, judgment under uncertainty, what you learned from the worst quarter. Send them to your references, not the investor.

#08. Hunt the weird verticals where AI has dropped the cost of being there

Gutter’s first Elbow Grease cohort included a former SpaceX / Northrop Grumman engineer putting cheap satellites into very low earth orbit, and Keeper Systems — AI agents for 211, the non-emergency hotline for people facing eviction or food insecurity. Neither was in Gutter’s stated thesis. Both got funded because the application quality forced the fund to broaden its aperture, and because the founders had domain depth no Stanford generalist could fake.

James’s frame: AI is dropping transaction costs across the entire economy, and “it feels like the entire economy is up for grabs.” The old rule that you need a big proven TAM dissolves when you can credibly displace a meaningful chunk of human labor inside a small market. Niche is no longer a death sentence — it’s increasingly where the most interesting Elbow Grease companies are showing up.

Action item: Make a list of verticals you actually understand that no Sand Hill partner would ever fund. Rank by how much human labor is currently doing work AI could now do credibly. Go where the score is highest.

#09. Don’t fetishize youth — sometimes the mid-career parent is the unlock

The fund is skewing younger; that’s real. Cheap software development means a 22-year-old operations person can ship product without engineers. But Dan is explicit about the trap: don’t fetishize youth. Some of the most prolific vibe-coders in the Elbow Grease cohort were not 19-year-olds — they were mid-career operators who had been thinking about a problem their entire careers, and the AI toolkit finally cut the dependency on engineers they’d been chafed by for two decades.

The archetype: the founder of Punch, a father of five (sixth on the way) in Atlanta who got permission from his family to spend ten weeks in the Canal Street office. He shipped product faster than almost anyone in the Gutter portfolio because his attitude was “I know this is my shot.” The right founder profile is not an age — it’s the person for whom this set of tools, right now, is the difference between never building and finally building.

Action item: Audit the founders you admire from the last 18 months by life stage, not by Twitter age. Identify the underrated profile in your network — and either back them or recruit them.

#10. Do your life’s work — authenticity is at an all-time premium

Gutter does not publish requests for startups. The reason is deliberate: they don’t want founders studying to the test. Dan’s closing advice — to Elbow Grease applicants and to everyone else — is that authenticity is at an all-time premium. Founders who are doing the thing only they can do get further, faster, against a backdrop where everyone else is pattern-matching to whatever a16z tweeted last week.

The aperture is wider than the AI label suggests. Gutter does the vertical AI work, but funded a satellites company and a 211 agents company in the same cohort because both founders were obviously on their life’s work. The question isn’t “is this a thesis area” — it’s “is this person doing the thing that, if you took venture capital off the board entirely, they would still be doing.”

Action item: Write the one-page version of why you are the only person who could be building this. If it reads generic, change the company, not the deck.

The pedigreed founders Gutter passes on,

and the ones they back the check on.

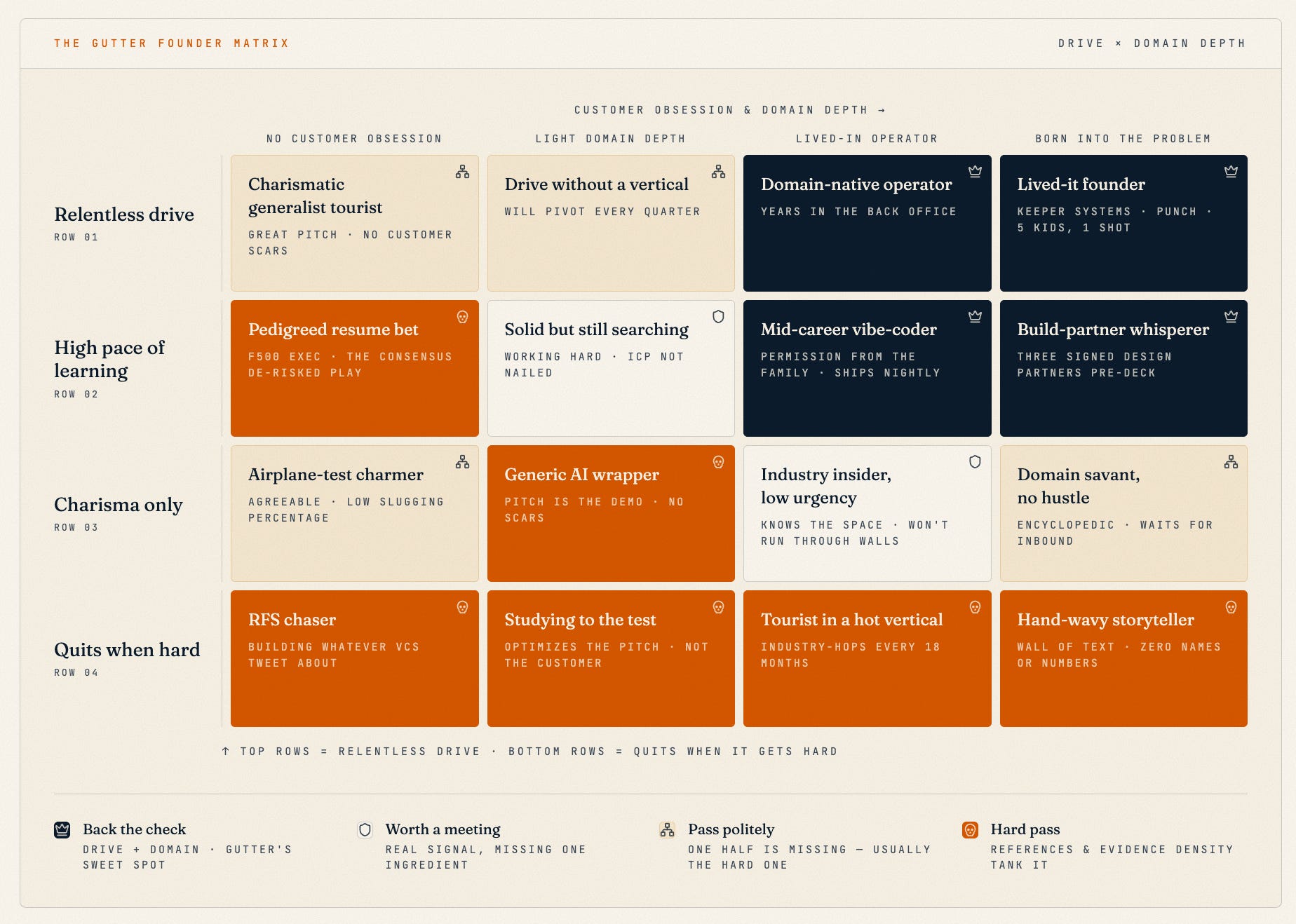

The Gutter founder matrix maps the two variables that drive inception-stage outcomes in their portfolio: relentless drive on the vertical axis, customer obsession and domain depth on the horizontal. The top-right corner is where the check gets written. The bottom-left is where references and evidence density tank the process. Most of the consensus market is busy underwriting the top-left.

We closed the episode by putting Nikhil — and Nic — in the seat and pricing the map in real time: which of the most highly valued vertical AI bets are sitting inside the kill zone, and which still have a clean moat, a real network, or an unloved vertical underneath them. Below: where on the map each lands, and the operator-grade reasoning underneath.

The pattern is uncomfortable but consistent. The hype-cycle category of any given year almost never produces the biggest outcome of that year. The biggest outcome comes from the category everyone agreed was dead, niche, or already won. If your whole thesis is in the consensus column, you’re not actually playing for power-law returns — you’re playing for second place.

The patterns that show up in the pitches Gutter passes on.

Walls of text without names or numbers

If the pitch can’t point to specific customers, exact metrics, or a phone number Gutter could actually call, it’s hand-waving. Evidence density was the single biggest predictor of who got an interview.

RFS chasers

Founders building whatever VCs are tweeting about this month. Gutter deliberately doesn’t publish requests for startups — they don’t want anyone studying to the test.

Charisma without commitment

Beautiful narrative, three-month tether to the space. The half-life of caring predicts the half-life of running. The pitch survives a meeting; the company doesn’t survive the next downturn.

Pedigreed but unscarred

Fortune 500 résumés where the line on the deck is the credential, not the accomplishment-per-dollar. The consensus market overpays for this; Gutter is built to pass on it.

None of these are character verdicts. They’re all repairable — but the founders who don’t notice them in their own pitch are the ones who don’t make it through the funnel.

The texture Dan & James see in the founders they actually back.

Resourcefulness-per-dollar

Founders who accomplished something extraordinary with almost nothing — and can prove it. The ratio, not the absolute. The most underweighted variable in the consensus market.

Lifelong commitment to the problem

Family in the industry, years in the back office, or an obsession since childhood. The kind of founder you couldn’t pay not to do this — even with venture off the board entirely.

Evidence-rich, name-game pitches

Specific customers, real numbers, three recorded calls attached unprompted. The founder pulls the string and just keeps going.

Demonstrated judgment in the wild

Enlists later-stage CEOs to do work for them. Tells a slow-moving customer she’s flying in Friday for a decision — and they send the address. Drive plus pace of learning, in real time.

The common thread: the founder has clearly been doing the work long before the deck got written, and the evidence is everywhere in the pitch. Gutter doesn’t have to imagine the company — they can see it operating.

The operator takeaway from a 40-hour Gutter diligence: pedigree is the cheapest input you can fake — evidence, drive and judgment are the ones you can’t. The check goes to whoever stacks the latter three on the same page.

The most uncomfortable line of the conversation: most consensus VC funds in 2026 are pattern-matching to founders who look de-risked on paper. The historical record says that’s the opposite of where the biggest outcomes come from. Gutter is a deliberate bet on the founders the consensus market is quietly leaving on the table.

Thanks for reading LINEAR. I reply to every email…

Have any questions, feedback, comments? Let us know, we work for you!