Linear #180.5: The Vertical AI Survival Map: Where to Build & Where to Avoid (With Nikhil Basu Trivedi of Footwork VC)

One vSaaS breakdown. One biz story. One 'how to'. In your inbox once a week.

The Vertical AI Survival Map

Nic and I sat down with Nikhil Basu Trivedi, co-founder and GP of Footwork VC and a 16-year VC veteran (early Canva, Lattice, Frame.io), on the question every operator is quietly asking: in a market where the model companies eat horizontal categories overnight and 20 funded competitors crowd every obvious idea, where are the parts of the map you can actually survive on? We map the kill zones to avoid, the moats that still compound (brand, networks, workflow trust), the unloved low-NPS verticals quietly ripe for AI-native challengers, and the consumer-meets-enterprise zone where the biggest companies of the cycle are already being built.

Most of the map is a kill zone.

Find the opportunity.

The honest version of building in vertical AI today is that most of the obvious map is hostile territory. The model companies eat horizontal workflows on a quarterly cadence. The consensus categories are auctions with 20 funded competitors before the round even closes. The old SaaS moats — features, integrations, a tidy ICP — get re-priced overnight. Nikhil’s frame for cutting through it isn’t a thesis, it’s a survival map: a small set of zones on the board where a vertical AI company can actually compound, and a much larger set you should refuse to play on at all.

The first survival question is the kill zone: how badly does your product overlap with what Anthropic or OpenAI is going to ship horizontally next year? Pure document review, generic Q&A, white-collar workflows that live happily in a Claude tab — the labs will eat. The survivors are products that need proprietary data, complicated integrations, or workflows that simply do not fit a chat box. If a one-pager titled “why a Claude tab can’t do this in 12 months” writes itself, you’re on the safe side of the map. If it doesn’t, change the product before you raise.

The second is the moats that still compound: in this era, very few do. Brand is the one technologists chronically underrate and the one Nikhil is most bullish on — the iPhone effect, where users simply do not switch off the products they trust, even when something technically better ships. Real network effects are the rarest and most valuable; the next LinkedIn, the next ACV Auctions. And there is workflow trust in traditional industries — the quiet truth that, once a credit union or a pharma company actually likes you, they do not want to re-evaluate every six months. Build one of these or you’re racing on execution speed alone, which is a brutal place to live.

The third is where on the map to actually build: the unloved low-NPS verticals everyone else ignored. CPG (a $3T+ category with 10,000 brands doing $100M+, almost no software at scale). Credit unions. Blood testing. Pharma research. Accounting back-offices. Antifragile demand, terrible incumbents, no real software heritage — and the buyer is finally ready, because their staff is using ChatGPT at home and asking why their forty-year-old EHR can’t do the same. And quietly underneath all of it, the founders Nikhil keeps backing share one trait: years of having lived in or studied the buyer. Domain depth, not pedigree, is the unlock. The rest of this issue is the full map.

This Weeks Vertical Titan:

Nikhil Basu Trivedi

(Co-Founder & GP @ Footwork VC)

Nikhil started his VC career nearly two decades ago. He co-founded Footwork five years ago with one partner and built it deliberately small: just the two GPs as the entire investment team, leading the seed or Series A in roughly five companies a year. Footwork is now investing its second fund — $225M, following a $175M first fund — and has made 25 investments to date.

Before Footwork, Nikhil was an early backer of Canva (led the seed in 2014), Lattice, and Frame.io. The Footwork portfolio today reads as a deliberate refusal of the consumer/enterprise binary — Elicit (AI for scientific research, co-led with Spot), Fuse (AI-native loan origination for credit unions, banks, auto lenders), Confido (the source of truth for ops, sales and finance at $100M+ CPG brands), plus stealth investments in blood testing and AI-native services in pharma and financial services.

The frame he keeps coming back to: roughly three-quarters of Footwork’s portfolio self-identifies as both consumer and enterprise. That isn’t a market-sizing trick. It’s a bet that the very biggest companies of this decade will be the ones with the audacity to conquer multiple markets — and that picking a side too early is quietly the most expensive mistake a founder can make.

And the line every founder should write on a wall: Nikhil is looking for teams with “years of having studied the buyer.” In the unsexy verticals where the customer is skeptical and the AI thesis isn’t pre-sold, that domain depth — not pedigree — is the unlock. Several of his best founders are first-time entrepreneurs in their 20s who simply know the back office cold

Ten coordinates on the survival map.

Operator-grade lessons for the things you’re actually deciding this week — which part of the map is safe to build on, which moats actually compound, which “stupid” vertical to attack, and which categories to walk away from before the model companies eat them — written for founders shipping on Monday morning, not the memo author a year later.

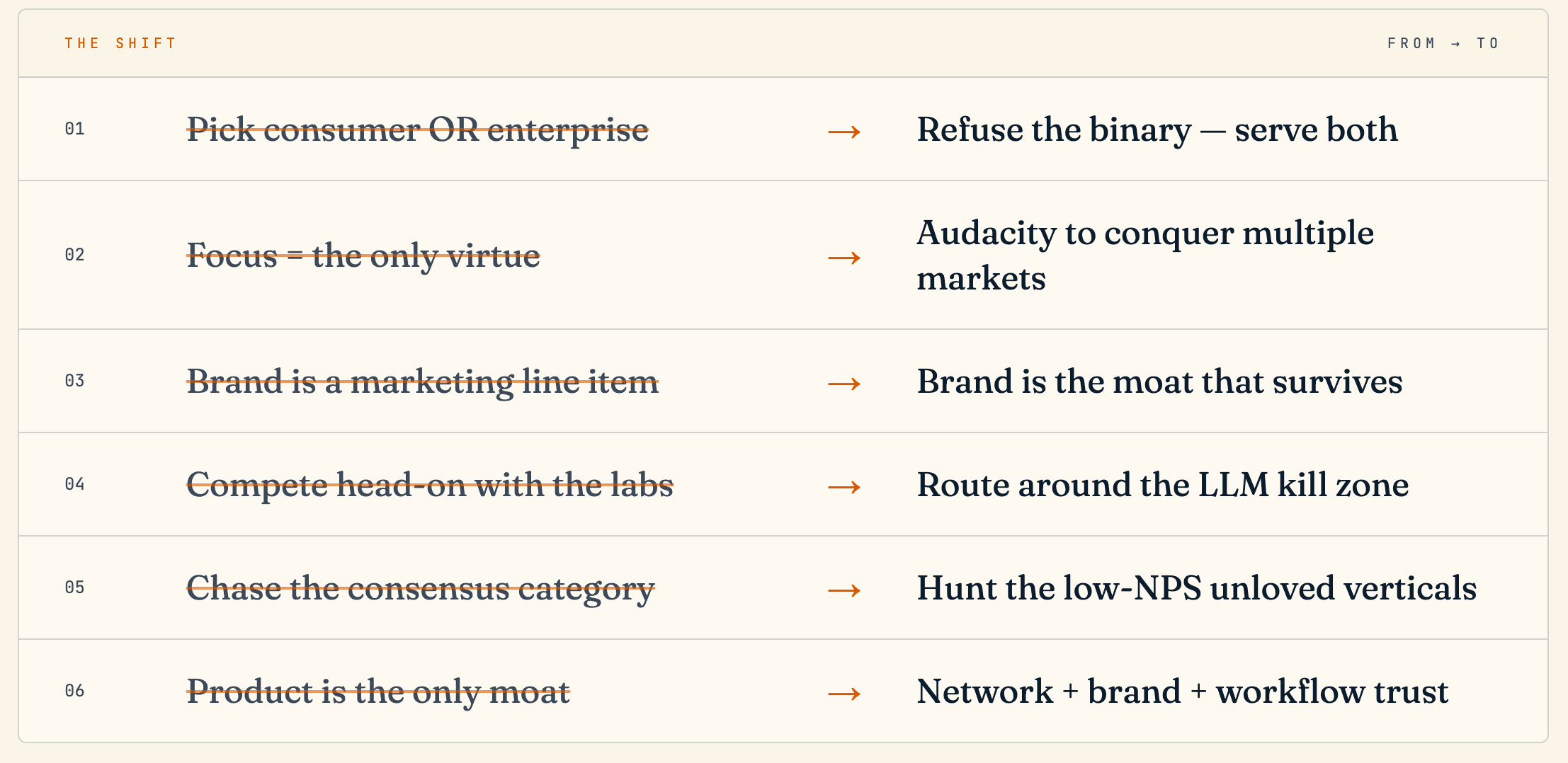

#01: Step one on the map: refuse the consumer/enterprise box

For twenty years the industry trained founders and investors to pick a side. Consumer team or enterprise team. PLG funnel or top-down sales motion. Nikhil’s contrarian read: the biggest companies in the world serve both, and almost always became both over time. Canva did $4B+ of ARR organically spreading from consumers to prosumers to the enterprise — $600M+ of that ARR now sits in the enterprise. SpaceX is a consumer subscription business (Starlink) renting B2B capacity to Colossus. OpenAI, Anthropic, Mercor, Open Evidence — every defining company of this cycle quietly carries both DNAs.

On the survival map, the binary itself is a trap. Picking one side caps your ceiling and quietly hands the other side to a competitor who didn’t. Three-quarters of Footwork’s portfolio refuses the box on purpose — not as a market-size argument but as a product-quality one. The bar set by ChatGPT and Claude at home is now the bar inside the enterprise. Build for one audience only and you’ll be out-magicked by someone who built for both.

Action item: Stop fighting over the consumer vs. enterprise label in your seed deck. Map both wedges. Pick the one you ship first — but design product, brand and pricing as if the other is two years away, not never.

#02: Earn the end user — it’s the cheapest path through the map

Elicit started as a self-serve AI product for individual researchers. Today it has enterprise-wide licenses with multiple top-20 pharma companies — none of which were sold top-down. Open Evidence didn’t pitch hospital systems; it earned physicians one at a time and let the bottoms-up demand pull the contract through. Both quietly went around the procurement playbook every legacy vertical software company is still running.

On the survival map, end-user love is the cheapest distribution you can buy. When the software is doing the work alongside a human — not just recording it — it has to feel personal, immediate, and trustworthy in the first 90 seconds. That’s a consumer bar, not a buying-committee one. Founders who internalize that ship a fundamentally different product, and quietly route around the incumbent sales motion entirely.

Action item: Make the first-time experience self-serve and unforgettable, even for an enterprise-bound product. Track activated end-users per company before you track logos.

#03: Plan for the B2B2C act — it’s a free moat on the map

Fuse is building an AI-native loan origination system for credit unions, banks, auto lenders. It is not, on the tin, a consumer product. But the byproduct of doing the job well is a dramatically better experience for the consumer applying for the loan — and that consumer is otherwise being courted by a neobank with a much sharper UI. Toast is the cautionary tale: a vertical software darling that never built a real consumer brand and is now vulnerable to DoorDash owning the moment of intent.

Almost every vertical SaaS company at scale ends up B2B2C — through embedded payments, financing, marketplaces, or just by being the touchpoint where the end customer experiences your buyer’s business. The founders who plan for that arc early get an extra moat for free. The ones who ignore it leave it for someone else to take.

Action item: Audit where the end consumer touches your product even when you sell B2B. Build for that surface as if it’s a standalone consumer brand — because eventually it will be one.

#04. Brand is the most underrated AI moat — start compounding it now

Nikhil’s most contrarian take: when the post-mortem of this AI era is written, brand will be the moat that quietly held everything together. People don’t switch off the products they trust with their data and their workflow, even when a technically superior competitor launches. iPhone is the case study — the flip phones and folding phones are objectively cool, and almost no one moves. The second Apple ships something, the entire market shifts back. That’s brand doing the work.

In vertical AI this is enormous, because the incumbents you’re attacking — your LabCorps, your 40-year-old EHRs, your legacy ERPs — have terrible NPS but have brand inertia. The opening is real, but only if you build a brand operators love. Capital can help; what compounds faster is a small set of early customers who are extraordinarily happy and tell their friends. That word-of-mouth in a small, tight-knit vertical is the hardest thing for a better-funded latecomer to replicate.

Action item: Treat early NPS, customer love and word-of-mouth in your vertical as a balance-sheet asset. Measure them. Resource them. Don’t outsource them.

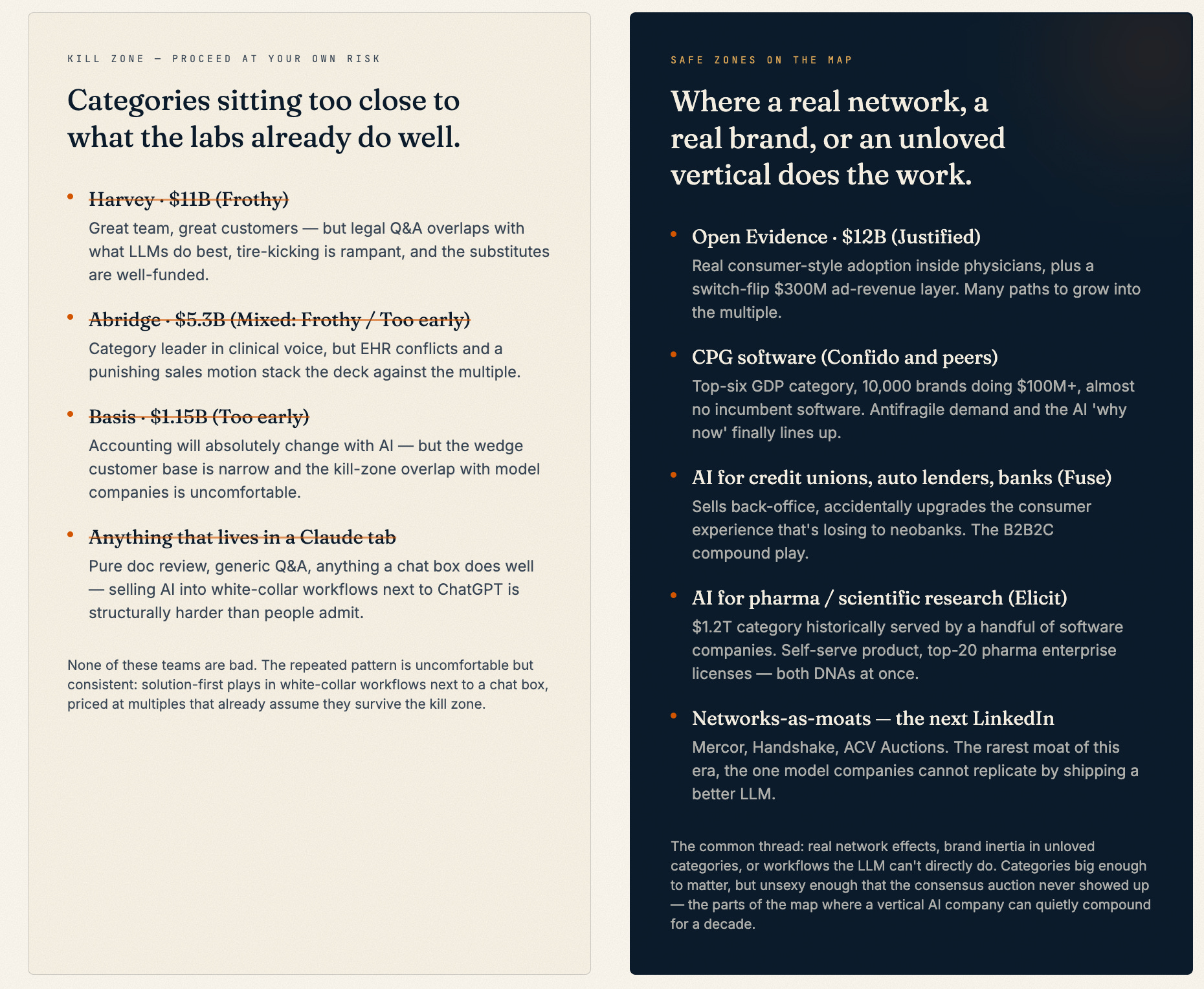

#05. Stay out of the LLM kill zone — pick the workflows chat can’t do

Nobody can prognosticate where the model companies are in five years, but you can absolutely choose not to stand in their path. Footwork’s underwriting filter: is this product fundamentally different from what Anthropic or OpenAI will ship horizontally? Is there a real reason for stickiness — proprietary data, complicated integrations, workflows that simply do not fit a chat interface? If not, it’s a thin bet no matter how strong the team.

It’s even worse if your core value prop overlaps with what the LLM already does well. Pure document review, generic Q&A, anything that lives comfortably in a Claude tab — the labs will eat. The work for founders is to find the parts of the job where a chat box is structurally the wrong UI, where the data is hard to get, and where the integration cost is the moat. That’s where defensibility quietly lives.

Action item: Write a one-pager titled ‘Why a Claude tab can’t do this in 12 months.’ If you can’t fill the page, change the product before you raise.

#06. Hunt the legacy verticals with terrible NPS and no software heritage

Ask a room of founders to name a venture-backed software company at scale selling into the CPG industry. Long pause. CPG is a top-six GDP category — $3T+ of spend — with 10,000 brands in the US doing more than $100M of revenue each, almost none of them well-served by software. Footwork’s portfolio company Confido is building the source of truth across ops, sales and finance for those brands, integrating with every retailer, doing trade promotion management and forecasting that has been manual until literally now.

These categories are ‘unloved’ for a reason: they’re harder to sell into, the buyer is more skeptical, the AI tailwind isn’t obvious to the customer yet. But they are also antifragile — people will keep eating, drinking, getting blood drawn, applying for credit-union loans, taking GLP-1s — and they are wildly underpenetrated by software. The boring vertical with low NPS incumbents and a real labor problem is, in 2026, often a far better venture bet than the obvious one.

Action item: Make a list of the ‘no one would build a SaaS company there’ verticals you actually understand. Rank them by NPS of the incumbent and willingness to pay against labor. Go where the score is worst.

A quick word from our incredible partner,

Parafin - the leading embedded capital partner.

4.8 star rating on Trustpilot, with over 500 reviews [source]

71% CSAT rating across all partners

84 NPS

Serving top Fortune 500 companies, including Amazon, Walmart, and DoorDash

#07. Network effects are still rare, still real, and worth raising your hand for

Nikhil’s 16-year dream company is the one that finally unseats LinkedIn — because LinkedIn is a brutal case study in just how durable a real network effect is. The Mercor / Handshake / data-labeling space is the closest thing this cycle has to that opening: experts and talent on one side, businesses on the other. Whoever actually builds the next professional network — the one where people show their skills, not just their resumes — is the real long-term threat in that category.

The broader point: network effects in this AI era are quietly some of the most powerful moats still available. ACV Auctions in car auctions, a category nobody would have predicted to be network-effect driven, is the archetype. If you have a real one — or sit on a latent network like Handshake did — it is one of the very few assets that compounds against falling model prices and accelerating competition.

Action item: Map the two-sided dynamics inside your vertical. If you can credibly seed both sides with the same product, you have a moat the model companies cannot replicate by shipping a better LLM.

#08. Earn the right to do more than one thing — but only when the team can

Focus still works. Anthropic’s relentless focus on coding agents is what’s powering its run inside the enterprise; OpenAI’s split attention across consumer and enterprise arguably cost them the developer mindshare they’re now chasing back. So the playbook isn’t ‘do everything from day one.’ It’s that at some point — sooner than the SaaS playbook would suggest — the very best companies are forced to do multiple things really, really well, and the founders who built a team capable of that compound faster than the ones who didn’t.

Nikhil isn’t the board member walking in saying ‘focus less.’ He’s the one watching whether the founder is openly thinking about the second and third act, hiring leaders who can shoulder them when the time comes, and staying flexible in a market that re-prices itself every quarter. That mindset is the real differentiator between a good company and a generational one.

Action item: Keep this quarter’s focus brutal. But sketch the second act on a single page and revisit it monthly. Hire one leader this year who could credibly run it.

#09. Back domain depth — especially in the unsexy verticals

The pattern across Confido (CPG), Fuse (credit unions), Elicit (pharma research): the founders are not Silicon Valley generalists parachuting in. Several are first-time entrepreneurs in their 20s. What they share is years of having lived in or studied their buyer. In categories where the customer is more skeptical and the AI thesis isn’t pre-sold, that domain depth is the unlock. You cannot fake your way into the trust of a CPG ops leader or a credit union CIO.

The corollary for operators: if you’re attacking a hairy vertical with no software heritage, your sharpest weapon is the depth of your relationships and the specificity of your insight into how the work actually gets done. The flashy go-to-market deck loses to the founder who can sit in the back office for a week and come back with a roadmap.

Action item: If you don’t have years of domain depth, hire it into the founding team — and spend a month embedded with your buyer before you ship v2.

The map, drawn live — which obvious bets are kill zones, and which are quietly the safe ones.

We closed the episode by putting Nikhil — and Nic — in the seat and pricing the map in real time: which of the most highly valued vertical AI bets are sitting inside the kill zone, and which still have a clean moat, a real network, or an unloved vertical underneath them. Below: where on the map each lands, and the operator-grade reasoning underneath.

The pattern is uncomfortable but consistent. The hype-cycle category of any given year almost never produces the biggest outcome of that year. The biggest outcome comes from the category everyone agreed was dead, niche, or already won. If your whole thesis is in the consensus column, you’re not actually playing for power-law returns — you’re playing for second place.

The operator takeaway from the rapid-fire round: don’t build inside the kill zone, no matter how loud the category is. Spend your time where the moat is brand, network, or workflow depth the LLM cannot replicate — that’s the only stretch of the map that actually compounds.

The most uncomfortable line of the conversation: selling AI into white-collar industries where the user already has Claude open is structurally harder than selling AI into a back office that has nothing today. The unloved legacy vertical with a 40-year-old EHR and no business network is, in 2026, often the better square on the survival map than the keynote-friendly one.

Survive the map first.

Then build something the labs can’t follow.

If you’re a founder or operator shipping vertical AI right now, four moves separate the companies that survive the map from the ones that don’t:

1. Map the kill zone before you map the market. If a Claude tab can credibly do your core value prop inside 12 months, you don’t have a company — you have a feature waiting to be eaten. Pick workflows that need proprietary data, hairy integrations, or a UI that isn’t chat.

2. Compound a real moat from day one. In this era only three actually hold: brand (the iPhone effect), real network effects (the next LinkedIn, the next ACV), and workflow trust earned inside a traditional industry. If you can’t name which one you’re building, execution speed is your only moat — and that’s a brutal place to live.

3. Build in the unloved, antifragile verticals. CPG, credit unions, blood testing, pharma research, accounting back-offices. Terrible incumbents, no real software heritage, demand that isn’t going anywhere. The unsexy squares on the map are quietly the biggest ones — and the consensus auction never shows up.

4. Refuse the binaries that cap your ceiling. Consumer or enterprise. Focused or expansive. Software or services. The defining companies of this cycle — Canva, SpaceX, Anthropic, Open Evidence — refused all three. Plan for the second and third acts early, even if you only ship the first one this year.

The operators who win this cycle are the ones who treat vertical AI like a map, not a thesis. Most of the board is hostile. A small set of squares — unloved verticals, real moats, workflows the labs can’t reach — is where the next generational companies are quietly being built. Find those squares, plant your flag, and compound for a decade.

Thanks for reading LINEAR. I reply to every email…

Have any questions, feedback, comments? Let us know, we work for you!