Linear #179.5: Enterprise now buys like a consumer. PMF just shifted underneath you (With Kyle Lui of Bling Capital)

One vSaaS breakdown. One biz story. One 'how to'. In your inbox once a week.

Enterprise now buys like a consumer. PMF just shifted underneath you.

Nic and I sat down with Kyle Liu, General Partner at Bling Capital — built around helping founders find, define and scale PMF — on the two shifts every operator is feeling but few are naming: enterprise buyers are behaving like consumers (they’ll try anything, they’ll churn on a dime, they want one bill not ten), and the old PMF signals — $1M ARR, logo lists, a clean Series A deck — quietly stopped meaning what they used to mean.

The line between consumer and

enterprise is collapsing.

For twenty years there was a clean story. Consumer products were tried in seconds, loved or churned. Enterprise products were sold over quarters, integrated for months, and stuck around for years. That story is dead. In AI, your enterprise buyer behaves like a consumer — they’ll spin you up on a Tuesday and rip you out the following Tuesday — and the old PMF signals never accounted for that.

Kyle’s seen this from the inside. Bling’s product council — 100+ heads of product and growth at top tech and AI companies — used to be a hiring and advisory bench. Now they’re acting like consumer users for portfolio companies: trying everything, switching constantly, telling you within a week if your product earns a permanent seat in their stack. Buying committees flattened. Procurement got bypassed. The “champion + economic buyer + IT” map you learned at the last enterprise SaaS company doesn’t necessarily describe the buyer room anymore.

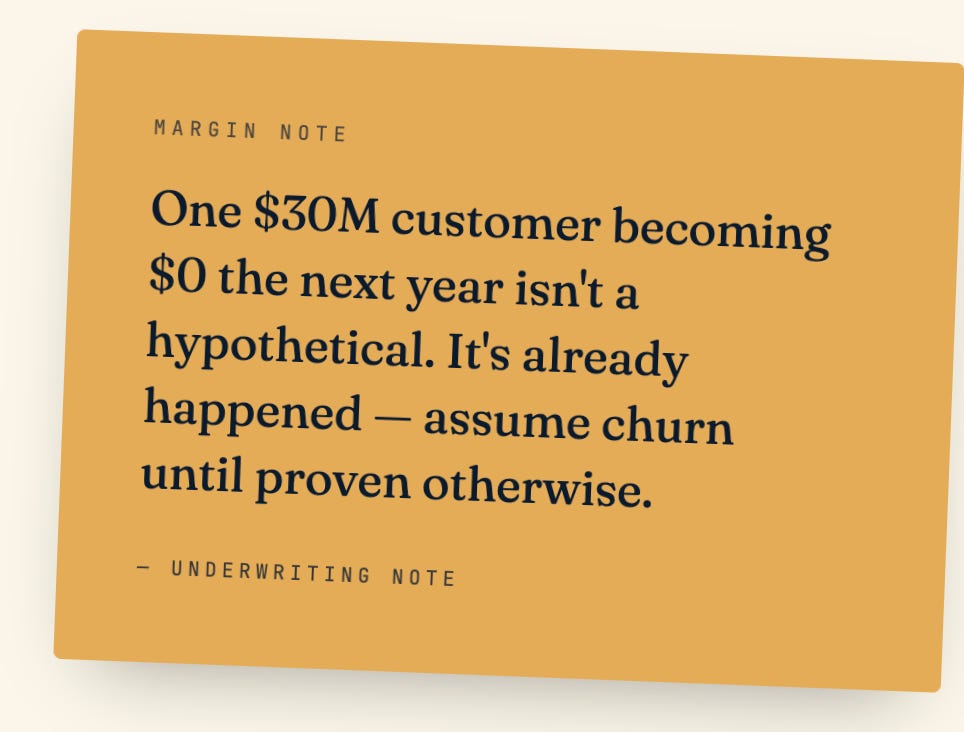

That collapse cuts both ways. The good news for operators: a single product-led demo can land a six-figure pilot in days. The bad news: a Series A AI company can go from a $30M customer to $0 the next year. Kyle’s seen it. The cost to build collapsed, the speed to market collapsed with it, and the feedback loops shortened — so 20 funded competitors now sit where three used to. $1M in ARR no longer proves anything. Defensibility, the thing every founder used to worry about later, is on the agenda at the seed pitch.

So what does PMF actually look like in the AI age — for founders shipping right now, not investors writing memos a year later?

That’s the lens Kyle brought in.

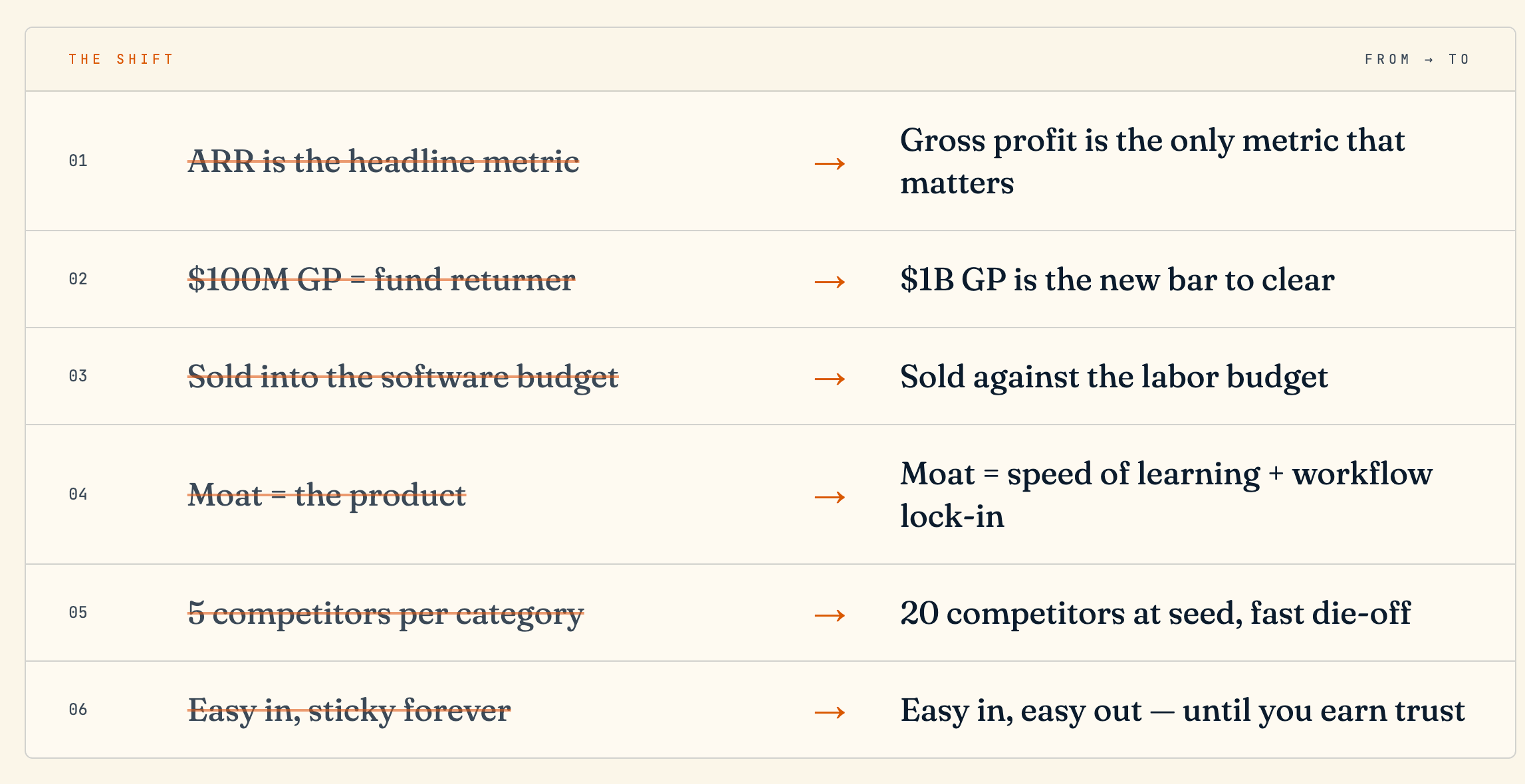

Earlier signal. Cohort discipline at week ten. A “press release at Series A” you can defend line by line. Gross profit, not ARR, as the honest scorecard.

And a gut-check on whether the enterprise customer who just signed will treat you like an indispensable system — or like a Claude tab they’ll close next quarter.

This Weeks Vertical Titan: Kyle Lui (Partner @ Bling Capital)

Kyle was an operator first. He founded Choice Passenger, a sales performance management company that was acquired by Salesforce and grew inside it into the Salesforce HR Cloud — roughly $40M in ARR across 1,000+ enterprise, mid-market and SMB customers. From there, eight years investing at DCM, and in 2022 he joined his first-ever angel — Ben Ling — as GP at Bling Capital.

Bling is a product-led seed fund with a 100+ strong product council of heads of product and growth at top tech and AI companies — increasingly doubling as early design partners for portfolio startups. Kyle’s portfolio includes Spellbook (vertical AI for legal), Alma (AI-native immigration law firm), Miniva (vertical AI for high-volume manufacturing), and PartBay (used auto parts — the “is this market even big enough?” company).

The frame he keeps coming back to: cohort data over storytelling. Even ten weeks of data is signal worth pulling — not to declare PMF, but to find the bright spot inside a semi-horizontal product and aim the whole company at it.

And the line every founder should write on a wall: he’s looking for “learn-it-alls, not know-it-alls.” Meet a founder on a Monday, meet them again the next Monday — if they’ve already talked to half the people you introduced them to and re-shaped the plan around what they heard, you’re probably looking at a generational team in formation.

The enterprise buyer now behaves like a consumer. They’ll try anything in a week — and churn just as fast if you haven’t earned the workflow.

— Kyle Lui, Bling Capital

What PMF actually looks like in the AI age.

Nine lessons every operator should re-internalize before they trust their next ARR chart — including the consumer-style behavior now showing up in every enterprise deal.

#01. Size the company, not the market — in gross profit, not TAM

Bling’s market-sizing exercise doesn’t ask for a TAM slide. It asks how the company gets to $100M and $500M in gross profit: how many customers, what percentage of the market, over what timeline. The numbers aren’t arbitrary — $100M GP is roughly what a seed fund needs from an 8–10% stake to return the fund, and $500M is the multi-stage equivalent. It’s an ICP and willingness-to-pay question dressed as market sizing.

In the AI era, Kyle now adds a third number: $1B. Multiples have come down, growth rates have gone up, competition has gone up, and the power law got even more extreme. A billion in gross profit is the bar a multi-stage fund needs to see to be excited. If your model can’t credibly find that ceiling, your cap table tops out before you’d like it to.

Action item: Run the $100M, $500M and $1B GP exercise for your business. If you can’t credibly hit the second number, you’re not seed-VC-fundable. If you can’t see the third, you’re not multi-stage-fundable.

#02. PMF as the Amazon press release you can’t write yet

At seed, true PMF is unknowable. What’s knowable is the early signal of it. Bling’s exercise: imagine you just raised your Series A 12–18 months from today and write the Amazon press release that announces it. What claims are in there? Customer love, engagement acceleration, early distribution proof points. Then break each claim into OKRs and work backwards.

Every generational company starts as a wedge — Uber was ‘five times the cost of a taxi and people can’t get enough.’ Stripe was a clean API. The vision can be enormous, but the wedge has to be brutally specific, and the press release forces the conversation about which wedge actually proves itself first.

Action item: Draft the press release. Break each claim into measurable proof points. Treat the doc as your PMF roadmap, not a marketing exercise.

#03. Cohorts at week ten — find the bright spot, don’t prove PMF

Whenever there’s data — even ten weeks of it — Bling pulls cohorts. Not to certify PMF, which would be premature, but to find the one or two slices where engagement or retention is meaningfully ahead. That’s especially powerful for companies with semi-horizontal products debating between adjacent verticals.

The job is to cut through the noise of a market with 20 funded competitors and find the customer profile where urgency is real. Once you see it, the whole company should bend toward it: positioning, hiring plan, design partners, the next product surface. Sound discipline beats storytelling — and at seed, that discipline is most of the moat you have.

Action item: Pull cohort retention, expansion and engagement on every customer slice. Pick the bright spot. Re-orient the company around it.

#04. Your enterprise buyer is a consumer now — and ARR is hiding it

In vertical SaaS, hitting $1M ARR meant something — it usually came from roughly twenty discerning customers with 80–95% likelihood of retention. In vertical AI, Kyle has seen a Series A company go from $30M in one customer to $0 the next year. The reason: enterprise buyers now behave like consumers. They trial fast, they champion fast, and they churn fast when the next demo is shinier — exactly the way an individual flips between Claude, ChatGPT and whatever they read about on Twitter that morning.

That’s why ARR has stopped being the honest scorecard. For operators, the numbers that actually predict survival are gross profit, gross-margin trajectory, customer concentration, and second-cohort retention. If a single customer is more than 20% of revenue, that’s not a logo — it’s a runway risk.

Action item: Don’t celebrate ARR until you’ve stress-tested concentration and second-cohort retention. Track GP, not bookings.

#05. Moats fall first — then rebuild around workflow and trust

Kyle is blunt: moats are falling. In the early days founders shouldn’t worry about defensibility because they have nothing to defend — what matters is execution speed and getting people to pay attention. But over time, the durable moats start to look familiar: data, workflow lock-in, and trust earned inside traditional industries that don’t actually want to switch once they’re happy.

Harvey, Legora, Spellbook didn’t out-model Claude — they out-executed everyone else and embedded into workflows the foundational labs aren’t going to touch. Developers are actually the hardest customer to retain, because they care about marginal performance. Traditional industries, once they trust you, are the opposite — they don’t want to re-evaluate every six months.

Action item: Year one, optimize for speed of learning. Year two, consciously pay down workflow depth and switching cost — not just ship features.

#6. Be the router, not the reseller

Users will pay a ~20% tax for a product that picks the right model for each task. Cursor is the canonical horizontal example; every vertical AI company has the same opening. The router is a clean wedge — high frequency, immediately valuable, and a beachhead for the workflow you actually want to own.

But if your core value prop is the same thing the LLM does well — pure document review, for instance — the labs can eat you. Routing is a wedge; it can’t be the whole company. The constellation of features around it is what makes ‘just use Claude’ a non-option twelve months in.

Action item: Start as a great router. Use that to capture workflow, data, and trust. Then layer the features that make a single-LLM fallback genuinely worse.

A quick word from our incredible partner,

Parafin - the leading embedded capital partner.

4.8 star rating on Trustpilot, with over 500 reviews [source]

71% CSAT rating across all partners

84 NPS

Serving top Fortune 500 companies, including Amazon, Walmart, and DoorDash

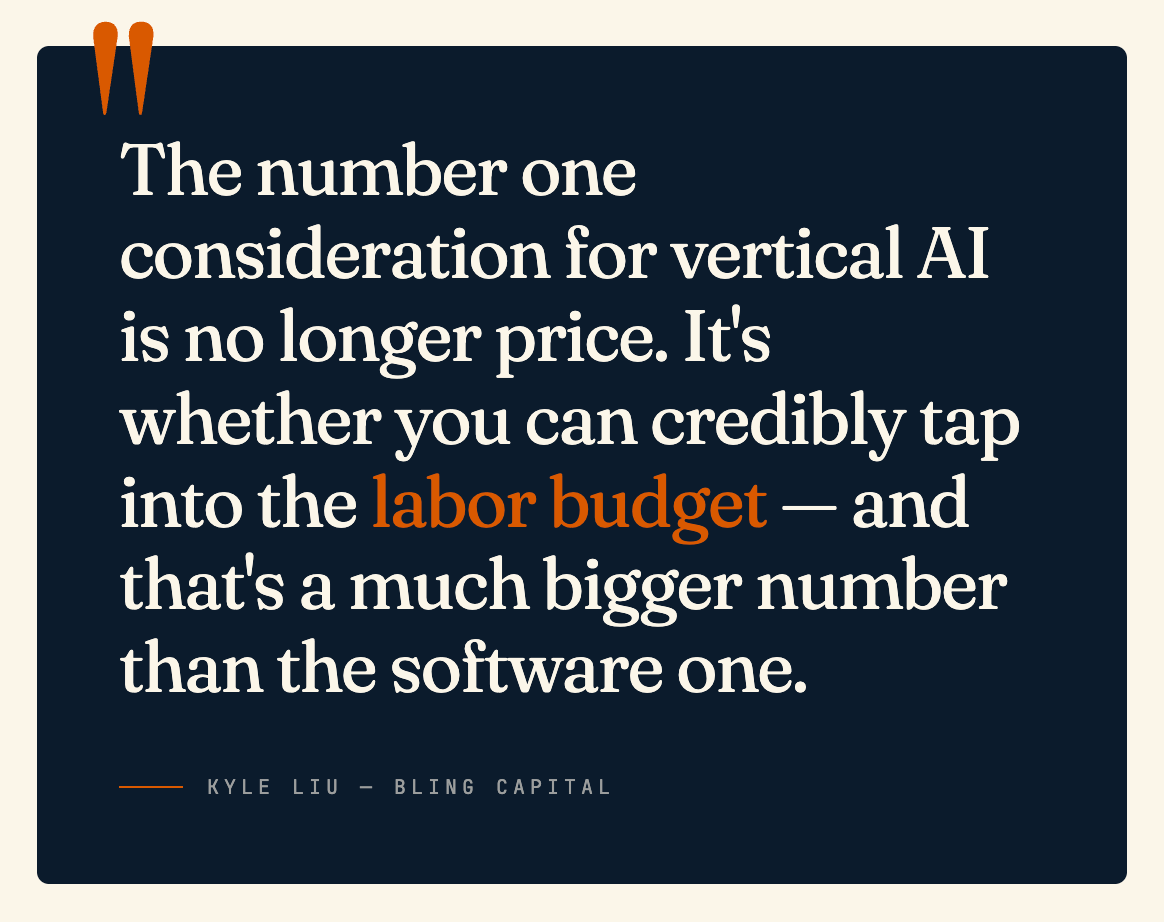

#07. Sell against the labor budget — the biggest unlock of the cycle

Kyle has watched board conversations rewire in real time. R&D line items now combine token spend and headcount in the same row — and traditional industries are even further along. They feel labor replacement viscerally. Alma, an AI-native immigration law firm in Kyle’s portfolio, compressed 40 attorney-hours of visa work into roughly 4. Miniva, in high-volume manufacturing, is targeting roles factories literally cannot find people for.

That changes what counts as a venture-scale market. Vertical AI for private aviation brokers sounds laughably niche — until you realize the early contracts are seven figures because the budget is coming out of payroll, not the software stack. The categories that didn’t pencil under SaaS economics often pencil beautifully when the comparison is loaded labor cost.

Action item: Price against fully-loaded labor cost. If buyers are still benchmarking you against SaaS seats, you haven’t told the right story yet.

#08. Gross margin still matters — eventually

Negative gross margin from compute is forgivable; everyone assumes inference costs trend down. Negative gross margin from a giant services bench is not — that’s just BPO with a venture multiple on top. Compute costs come down. People costs don’t.

You can’t invest a dollar to make 80 cents forever. There has to be a clear inflection where the business model becomes viable on its own — and a credible path from today’s gross margin to a steady-state target you can actually defend in a board meeting.

Action item: Map the path from today’s GM to a steady-state target. If you can’t draw that line, you don’t have a business yet — you have a subsidy.

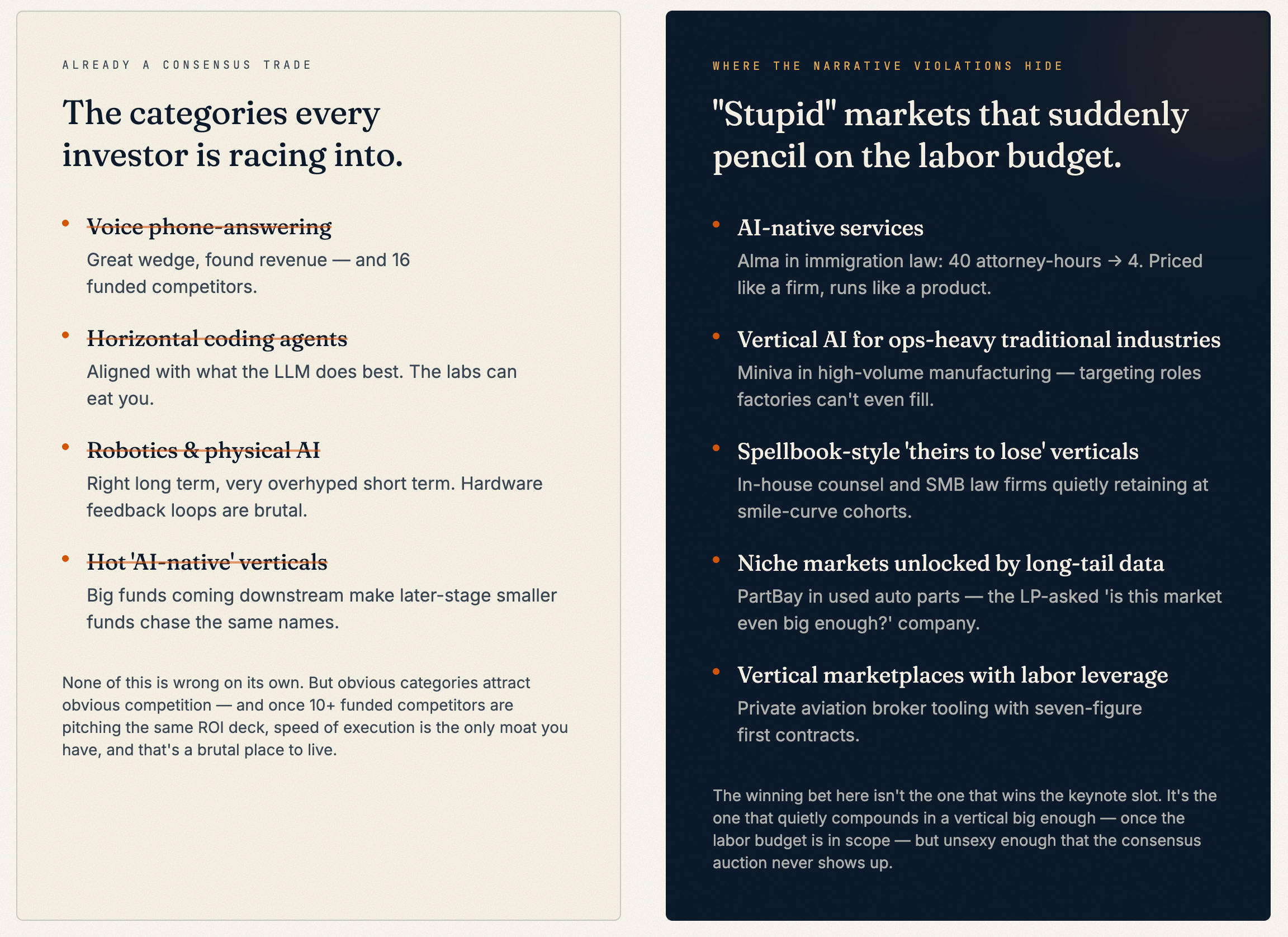

#09. Hunt narrative violations — the obvious bets are already crowded

Big funds coming downstream has created consensus vortices around a few hot categories. Meanwhile the biggest outcomes of this decade — SpaceX, Anthropic, OpenAI — were all unloved at the moments that mattered most. The ‘stupid’ vertical that 10 VCs pass on may actually buy you the longest stretch of low competition and a clean shot at owning the names that matter in your market.

If everyone you respect is already in your category, your moat is now execution speed and very little else — a brutal place to live. If they all think it’s stupid, do the work twice. That’s where the real outcomes hide.

Action item: Pressure-test your category against the consensus list. If you’re on it, ask what would have to be true for you to win on execution alone.

Where vertical AI is already a consensus trade — and where the real outcomes still hide.

Big funds coming downstream has created consensus vortices around a handful of categories. Kyle’s read on where the auction is hot — and where the next category-defining companies are most likely to be quietly built.

Kyle’s most provocative line:

The pattern is uncomfortable but consistent. The hype-cycle category of any given year almost never produces the biggest outcome of that year. The biggest outcome comes from the category everyone agreed was dead, niche, or already won. If your whole thesis is in the consensus column, you’re not actually playing for power-law returns — you’re playing for second place.

Thanks for reading LINEAR. I reply to every email…

Have any questions, feedback, comments? Let us know, we work for you!

Enterprise buyers acting more like consumers explains a lot of the churn, experimentation, and pressure on AI startups to prove value faster than ever