Linear #176: Your vSaaS Company Is Probably Not Worth 5x ARR, Why You Need To Become An AI Company, Avoca's $125M Announcement

One vSaaS breakdown. One biz story. One 'how to'. In your inbox once a week.

Today’s newsletter is sponsored by Xplor Pay. Embedded payments shouldn’t slow your growth. Xplor Pay Flex Framework helps vertical SaaS platforms choose the right model, adapt over time, and scale with confidence.

Shaped by lessons from decades of building and scaling 20+ SaaS platforms, it turns payments into a true growth lever. Read the guide to see how top platforms get it right. Read Now.

Your vSaaS Company Is Probably Not Worth 5x ARR (& how to overcome that)

Ok, I know none of you want to hear this.

I sure didn’t during the SaaS Crash. I anchored my mind that my company was always going to be worth 10x ARR. It was painful when I realized….. It wasn’t.

So let’s talk about it. And what you can do to get back to a higher multiple.

This week’s issue is about valuation reality.

Not the founder-group-chat version.

Not what the bankers tell you.

The real one.

Public SaaS comps have compressed. Private buyers have gotten stricter. AI-native companies are still getting paid differently. And a huge number of founders still have 10x ARR stuck in their head like it’s a law of physics.

It isn’t.

The most important skill for a founder in this market is intellectual honesty: knowing your real downside value (and being GOOD with you / your teams situation if that is indeed what happens) all while still building toward a much better future state.

How to understand the actual value of your company

Most founders start with the wrong question.

They ask:

What multiple should I get?

The better question is:

What is a buyer actually paying for?

Because buyers are not paying for your ARR in the abstract.

1) Start with public reality, not private mythology

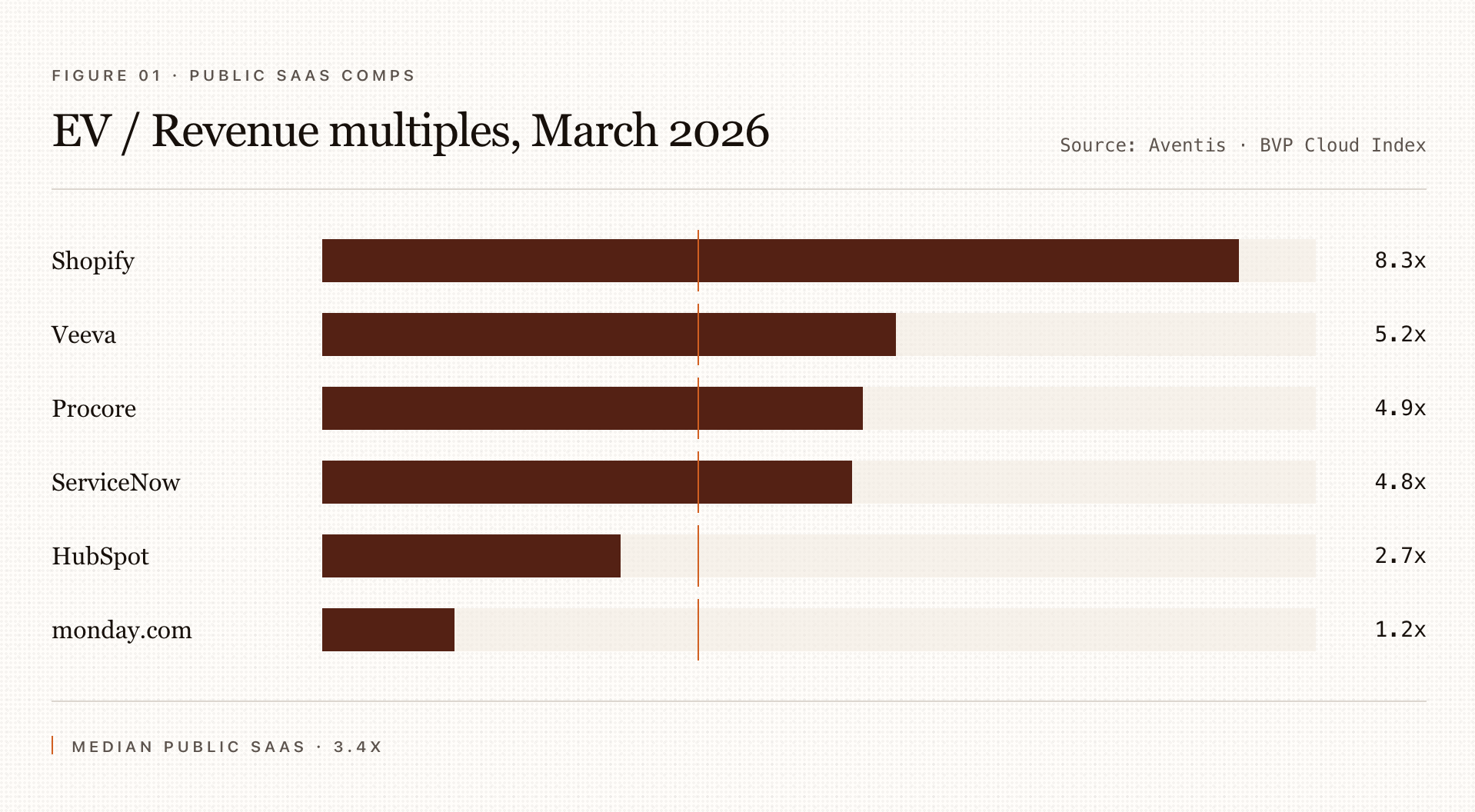

As of March 2026, Aventis shows the median public SaaS EV/revenue multiple at 3.4x. That is a brutal reset from the old market. And even strong public software names are not all floating around on fantasy numbers. On the BVP cloud index, recent EV revenue multiples were roughly 4.8x for ServiceNow, 2.7x for HubSpot, 4.9x for Procore, 5.2x for Veeva, 1.2x for monday.com, and 8.3x for Shopify. The spread is wide, but the lesson is obvious: the market is rewarding only a narrow band of truly exceptional assets.

So if elite public software companies are trading in the low-to-mid single digits on forward revenue, your private company does not deserve 5-10x ARR by default just because you are software.

The best companies in the WORLD are trading <5X ARR..

That number is not a principle.

It is our current data.

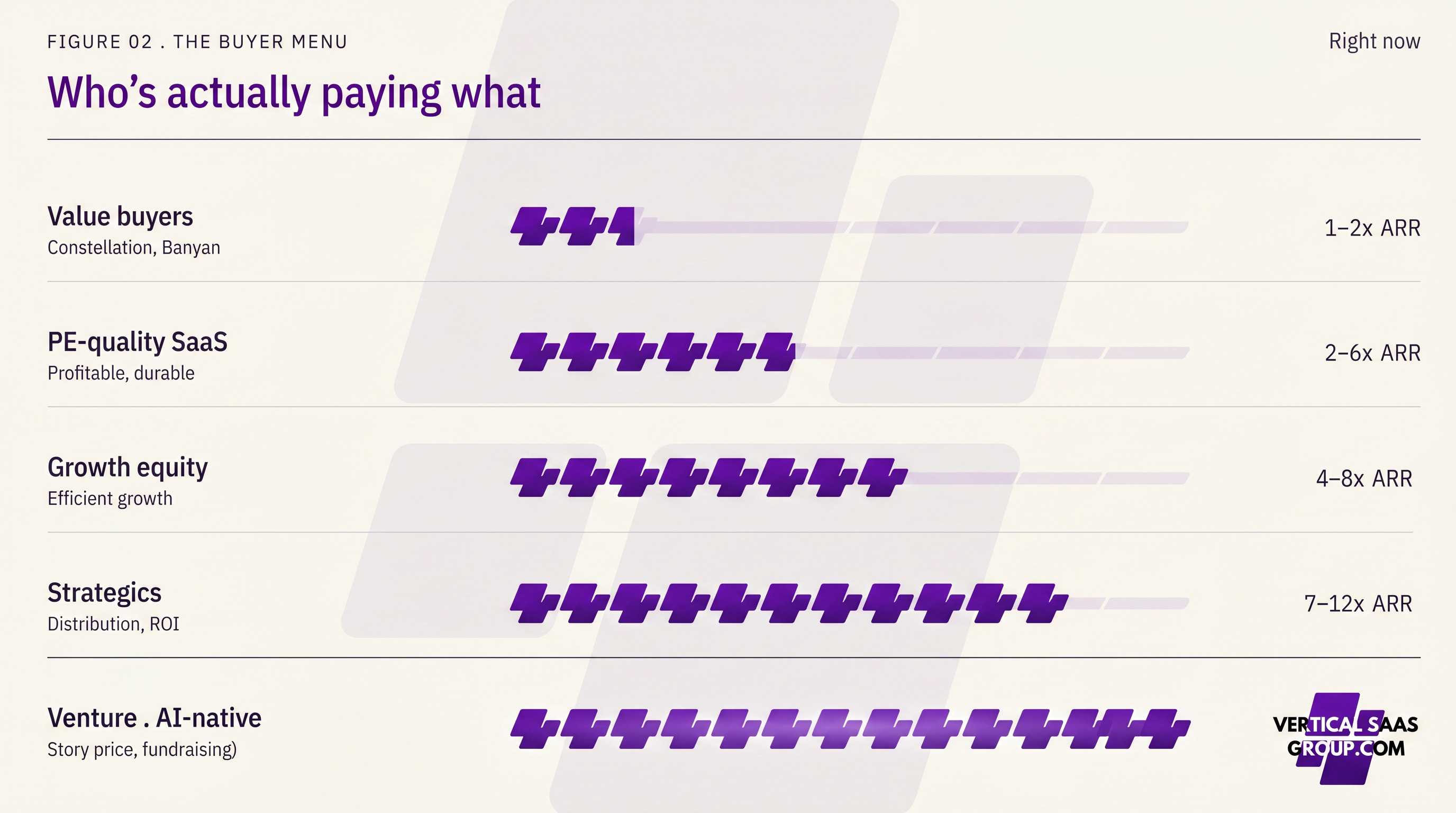

2) Understand the actual buyer buckets

The cleanest way to think about the market right now is by buyer type and asset quality.

Here’s the rough menu based on what I’m seeing RIGHT NOW:

Value Buyers (Constellation, Banyan, etc.) often closer to 1–2x ARR / low-teens EBITDA logic

Private equity-quality SaaS businesses: often 2–6x ARR

Growth equity-quality assets: often 4–8x ARR

Venture investors: often 8x ARR+ but these folks are almost exclusively funding AI-Native companies.

Strategics can land 7–12x ARR, with occasional higher outcomes for standout companies but this is only if they can really sell your product into a massive base and quickly deliver an ROI. A lot of strategics are incredibly worried right now about M&A. Especially public ones. If the market doesn’t like what they paid, they will get hammered. And they can’t afford that right now. They really only want to buy AI.

That doesn’t mean every founder should accept the low end.

It means every founder should understand what market they are actually in.

3) Ask the most important valuation question: what meat is left on the bone?

This is the question buyers actually care about.

Not “how hard did you work?”

Not “what did SaaS trade at in 2021?”

Not “what did your friend get?”

They care about what value is still available after they buy the company.

That usually means they are underwriting some combination of price increases, better packaging, margin improvement, sales efficiency, lower churn, embedded payments attach, AI-driven labor reduction, cross-sell, better lead conversion, or tighter operational control.

If you have already optimized everything, there is less upside for the buyer.

And if there is less upside for the buyer, there is less price for the seller. That is why some founders overestimate value. They confuse “good company” with “high-upside acquisition target.”

Those are not the same thing.

You HAVE to package for a buyer exactly how they will crush it. It took me years to realize this…

4) Separate quality from scarcity

A business can be solid without being scarce.

Scarcity is what drives price.

Scarcity comes from:

proprietary data,

embedded workflows,

trust with a niche customer set,

measurable AI leverage,

or a monetization wedge competitors do not have.

That is one reason AI matters so much. If your company is still just workflow software with a few automations, you will usually be valued like software. If your company is becoming the decision layer, action layer, or revenue layer for a vertical, you can start to access a different conversation.

5) Get comfortable with your downside number

This is the part founders avoid.

You should know:

your fundraising story value,

your strategic premium value,

and your downside private-market value.

You do not need to love the downside number.

You just need to know it.

Because once you know it, you can make sharper decisions about whether to raise, wait, hire, cut, reposition, or push harder into AI. Intellectual honesty is not bearish. It is what allows you to move with precision.

This Is Why You Need To Become an AI Company, Not a SaaS Company…

If you are building vertical software right now, you should be racing to become an AI company.

Not because “AI” is trendy.

Not because your deck needs new words.

Because the market is still telling you, very clearly, that AI companies are being priced differently from traditional software companies. Carta found that seed-stage AI companies carried a 42% higher median pre-money valuation than non-AI startups in 2024, while Series A AI companies were valued 30% higher and Series B AI companies 50% higher. In Carta’s 2025 review, the AI premium persisted, with Series A AI valuations 38% higher than non-AI peers and late-stage premiums reaching 193% at Series E+.

But the most useful way to frame this is: the AI premium is real, but it is not automatic.

A lot of that premium is happening in fundraising markets, not necessarily in full-company sale processes. Aventis puts the median revenue multiple for AI companies in fundraising comps at 29.7x, while explicitly warning that full M&A outcomes are usually significantly lower. That distinction matters.

Founders keep confusing “what venture investors will mark up” with “what a buyer will wire.”

Those are VERY DIFFERENT different numbers.

That’s why founders need two prices in their head at all times:

the story price

the downside price

The story price is what you market.

The downside price is what you plan around.

The story price is what gets people excited.

The downside price is what keeps you from making bad strategic decisions.

And if you want that downside price to move, you need to become the kind of vertical company that deserves AI repricing.

That usually means some combination of:

owning a higher-value workflow,

using proprietary vertical data,

automating labor-heavy steps,

getting closer to revenue or margin outcomes,

and becoming harder to rip out of the customer’s daily operation.

This is probably the most important one, it’s showing AI-level growth. It’s not just re-branding as an AI company. And that my friends, is a lot harder than X.com makes it seem…

That is the real shift.

The old moat was being the system of record.

The new moat is becoming the system that helps the customer make money, save labor, and move faster.

Avoca: the home-services AI company everyone should study

Avoca announced on April 27 that it had raised more than $125 million across Seed, Series A, and Series B at a $1 billion valuation, backed by Kleiner Perkins, Meritech, General Catalyst, Amplify Partners, Nexus Venture Partners, and Y Combinator. The company says it is building AI agents for the services economy, starting in home services and expanding into roofing, restoration, auto, and adjacent verticals.

That alone makes it notable.

But the more important part is why investors paid attention.

What Avoca actually does

Avoca calls itself “the AI front office for home services.” That is the right framing. Not general AI for contractors. Not “copilot for SMB.” A front-office system built to answer every call, book more jobs, fill open capacity, and give operators visibility into how the revenue engine is performing.

On the product side, Avoca is building a pretty coherent stack:

Inbound AI agents that answer calls, texts, and chats 24/7

AI booking that can schedule jobs and sync them into the customer’s CRM

Emergency escalation and routing when calls require humans or urgent handling

Outbound campaigns across SMS and calls to re-engage customers, revive old estimates, renew memberships, and fill the board

Call scoring / analytics / coaching to surface missed opportunities and monitor CSR performance

That matters because most home-service companies do not just have a “phone problem.”

They have a front-office capacity problem.

They are bleeding revenue through:

missed inbound demand,

slow speed-to-lead,

after-hours gaps,

weak estimate follow-up,

inconsistent booking quality,

and underutilized schedules.

Avoca is attacking that whole surface area.

The insight behind the company

The founding story here is unusually good.

Fortune reported that Avoca’s founders were originally thinking about restaurants. Then they met an HVAC company in Texas and realized something important: when a restaurant misses a call, maybe it loses a $30 or $40 order. When a home-service company misses a call, it may be losing a $30,000 or $40,000 HVAC install.

That is the kind of insight I always pay attention to.

It is not abstract.

It is not narrative-driven.

It is economic.

They found a vertical where one operational failure point had an absurdly high dollar consequence.

That is how you build a category.

How Avoca says it works

One of the most interesting things about Avoca is that it is not just selling a model. It is selling deployment.

The company describes itself as an omnichannel AI platform for home services, and its docs and integrations make it clear that the product is meant to sit at the customer communication and intake layer: handling inbound calls, chat, web inquiries, qualification, booking, and syncing clean job records into the underlying system.

That last point is important.

On its Aitto integration page, Avoca says: “Aitto runs operations exactly as it does today” and “Avoca adds a front-end intake layer.” In other words, Avoca is often not asking the contractor to rip out the core operating system. It is asking to own the front door.

That is a very strong wedge.

Because in vertical software, the company that controls the front office often controls:

lead capture,

booking quality,

board fill,

response speed,

revenue attribution,

and the first customer impression.

That is not a side feature.

That is the growth engine.

Why their implementation model matters

Most AI vendors talk about product. Avoca also talks about deployment.

The company has written about using Forward Deployed Engineers who sit with customer teams, learn how dispatch boards are actually used, understand their edge cases, and then tune the deployment around how the office really runs. Avoca says this shortens feedback loops from weeks to hours and allows highly customized logic for things like emergency handling, routing rules, or local operating nuances.

That tells you something important about how they see the market:

They are not treating the front office as generic.

They are treating it as operational software.

And that is the right instinct.

In home services, a Phoenix HVAC operator and a New Jersey plumber do not run the same business. If you want to automate the real workflow, not just the demo version of the workflow, someone has to care about the details.

The product suite is broader than just “AI phone answering”

This is where Avoca gets more interesting than the simple headline.

Yes, the company started around the missed-call problem.

But if you look at the site, case studies, and outbound pages, it is already moving into a broader revenue-ops layer:

after-hours and overflow call handling,

hybrid AI + human call coverage,

outbound reactivation campaigns,

capacity-aware board filling,

AI-led qualification,

direct CRM booking,

and manager analytics tied to bookings and revenue.

That is an important transition.

Phone-answering is a wedge.

Revenue orchestration is the real opportunity.

It’s basically building Gong for Home Services companies.

The customer evidence is stronger than most early AI companies

The case studies on Avoca’s site are worth reading because they show a consistent pattern: this is not being sold as novelty software. It is being sold as a very clear ROI system.

Aire Serv says replacing a traditional live answering service with Avoca led to:

after-hours bookings increasing from 58 to 208,

a 90% booking rate on after-hours calls,

an 8.6% increase in overall booked calls,

and 41% of eligible callers signing up for subscription plans.

Call Dad (great name for a home services biz btw) says Avoca’s hybrid model let AI handle 78% of all calls, achieve a 90%+ AI call resolution rate, and drive a mix where 70%+ of booked jobs were repair and service work, which they identify as the highest-margin category.

Reliable Comfort says Avoca enabled 100% after-hours coverage, handled 150+ simultaneous calls, and allowed the business to achieve true 24/7 responsiveness without adding staff.

That pattern is what investors are paying for.

Not AI theatre.

Operational leverage.

So how does Avoca stack up against ServiceTitan and Housecall Pro?

This is where the story gets interesting.

Because Avoca is not entering an empty market. This is a brutally competitive space.

The incumbents have noticed the same thing.

ServiceTitan is the incumbent system-of-record giant

ServiceTitan is pushing hard with its Pro Products suite. Its positioning is broad: automate the entire customer journey using AI powered by ServiceTitan data. The stack includes Contact Center Pro, Marketing Pro, Scheduling Pro, Dispatch Pro, and Phones Pro. Contact Center Pro includes AI call summaries, sentiment analysis, second-chance lead identification, and AI voice agents that can book jobs, reschedule appointments, and escalate to live agents. Phones Pro is fully integrated into ServiceTitan’s software and built around giving office staff a native call-booking workflow.

ServiceTitan’s core advantage is obvious:

it owns the operating system,

it has the data,

it has the incumbent distribution,

and it can bundle AI into a larger suite.

If you are already a deep ServiceTitan customer, its native AI products will be very attractive.

Housecall Pro is building the SMB-friendly all-in-one

Housecall Pro is coming from a different angle. It positions itself as the simpler “run and grow your business” platform for home-service pros, and increasingly layers AI across that experience. Its AI Team includes:

CSR AI for answering calls and chats and booking jobs 24/7,

Analyst AI for reports and trend analysis,

Coach AI for business recommendations,

and Marketing AI for generating customer-facing content.

Housecall Pro’s advantage is simplicity and breadth for smaller operators. It is not just selling AI answering. It is selling an easier operating stack with AI embedded inside.

If ServiceTitan is the enterprise incumbent, Housecall Pro is the friendlier SMB operating system with an increasingly opinionated AI layer.

Where Avoca is different

Avoca’s wedge is narrower, but in some ways sharper.

It is not trying to be the whole back office.

It is trying to own the front-office revenue layer.

That means its differentiation looks something like this:

The key strategic distinction is this:

ServiceTitan and Housecall Pro are extending from the system of record outward.

Avoca is attacking from the front office inward.

That is a real opening.

Because many vertical markets get disrupted first at the workflow edge, not at the data core.

The real question: can Avoca become more than a wedge?

This is what I’d be watching.

Avoca clearly has the wedge:

high-value missed calls,

after-hours capture,

faster booking,

better outbound follow-up,

stronger board utilization.

That is enough to build a meaningful company.

But the really big outcome happens if the company turns that wedge into a deeper system:

more ownership of customer communication,

more attribution,

more customer lifecycle automation,

more revenue optimization,

more manager tooling,

and more leverage across adjacent service verticals.

The reason this matters is simple:

If Avoca stays “AI phone answering,” it is a feature-rich point solution.

If Avoca becomes the AI revenue layer for service businesses, it becomes something much more durable.

And the site already hints in that direction. Outbound board-fill workflows, estimate recovery, membership renewals, CRM syncing, analytics, and hybrid staffing all push it closer to revenue infrastructure than pure communication software.

My take

I think Avoca is a very good example of where vertical AI gets interesting.

Not when it tries to replace the entire incumbent stack on day one.

Not when it sells “agents” as a vague concept.

But when it finds one painful, high-ROI, high-frequency problem and starts owning an increasingly valuable layer of the workflow.

That is what this looks like:

missed calls become booked jobs,

booked jobs become board utilization,

board utilization becomes revenue,

and revenue intelligence becomes product expansion.

That is how vertical AI creeps from wedge into platform.

And that is exactly why the round happened.

Do me a solid and forward to a friend :-)