Linear #165: Launch an AI Agent App Store, Vertical Software Summit is BACK, Casca & Why It Could Be a Big Vertical AI Player

One vSaaS breakdown. One biz story. One 'how to'. In your inbox once a week.

Today’s newsletter is sponsored by Xplor Pay. In a case study they show how a POS provider embedded payments using PayFac as a Service without taking on the burden of compliance, risk, or merchant onboarding.

Learn how white-labeled payments, streamlined setup, and flat-rate pricing helped the platform improve the experience while unlocking new recurring revenue. Read the full case study here.

Alright, let’s get to it…

SaaS Company? Think About Adding An AI Agent App Store This Year

Every SaaS company that is 4 years old or more is racing to add AI products and transform its business into an AI Company.

At this point, I think most realize that

A) they need to do this from a valuation perspective and

B) the world is headed in this direction.

I do want to propose something to think about for platform companies that find themselves in this exact circumstance…

Should you add your own AI Agent products? Yeah, I think so. I sure would be. Hopefully you already have, but if not, I’d get on it.

But MORE IMPORTANTLY, there are other creative ways to drive value and position yourself well in this new era.

What about building the AI Agent App Store for your industry?

What if instead of just relying on yourself and your team to add net new products, you go partner with every upstart in the industry and launch an AI Agent App Store.

This is nice for a few reasons…

#1. You're not solely dependent on your internal resources to build/create/ship/iterate/etc

#2. You add a nice platform moat. If you are a system of record for your industry, this strategy will make it so everyone can play with / test AI products directly within your tool, leveraging your system’s data set.

#3. You won’t be on the HOOK for every AI product. Similar to the iOS App Store, folks aren’t blaming Apple for bad Apps. They're blaming the App maker themselves…

I haven’t seen ANY industry Systems of Record of Platforms take this approach, and I think it’s a really smart one to create staying power. You can still build your own AI tools, just launch them in YOUR app store.

App Stores are beautiful moats and beautiful business models. Nothing beats a toll fee.

A few REAL WORLD Examples of companies that SHOULD do this…

ServiceTitan (for home services/trades like plumbing, HVAC, electrical)

ServiceTitan is a comprehensive system of record for trade businesses, centralizing job scheduling, customer records, invoicing, dispatching, inventory, technician performance, and financials. It holds deep proprietary data on job histories, customer interactions, pricing, and operational metrics.

If they did this: They could launch a “ServiceTitan AI Agent Marketplace” where third-party AI developers build specialized agents (e.g., predictive maintenance agents that analyze historical job data to forecast equipment failures, dynamic pricing agents for quotes based on real-time market and customer data, or automated follow-up agents for customer satisfaction). These agents would run natively in ServiceTitan’s dashboard, accessing the platform’s dataset securely via APIs.ServiceTitan takes a cut (e.g., 20-30% toll) on transactions or subscriptions, while avoiding blame for underperforming agents and accelerating AI innovation without building everything in-house.

Toast (for restaurants)

Toast is the dominant point-of-sale and management platform (system of record) for restaurants, managing orders, menus, inventory, staff scheduling, payments, customer loyalty data, sales analytics, and online ordering integrations. It captures granular, real-time data on every transaction, menu performance, and guest behavior.

If they did this: A “Toast AI Agent Store” could partner with AI upstarts for agents like intelligent menu optimizers (analyzing sales data to suggest dynamic pricing or item removals), predictive staffing agents (forecasting busy periods from historical trends and external factors like weather/events), or personalized guest experience agents (generating tailored recommendations or automated re-engagement campaigns). Agents would integrate directly into Toast’s POS terminals or back-office app, using the platform’s rich transactional dataset. Toast monetizes via app fees or rev-share, builds a stronger moat by making Toast the central hub for restaurant AI experimentation, and lets developers iterate fast on niche tools.Mindbody (for fitness/wellness studios, gyms, spas, and boutiques):

Mindbody is a leading system of record for the wellness industry, handling class/instructor scheduling, client bookings, memberships, payments, attendance tracking, retail inventory, and marketing for studios and spas. It stores extensive client profiles, booking histories, class performance, and revenue data.

If they did this: They could create a “Mindbody AI Agent App Store” for partners to offer agents such as personalized workout planners (using client history and goals to suggest classes/programs), retention prediction agents (flagging at-risk members from attendance patterns), or dynamic pricing agents for classes/memberships based on demand data. These would embed in theMindbody app or client-facing portal, leveraging the platform’s dataset for hyper-relevant AI. Mindbody earns platform fees, reduces reliance on internal AI builds, and positions itself as the indispensable ecosystem hub—much like the blog’s vision—while third-party developers handle specialized AI innovation.

Obviously this won’t be applicable to upstarts, but if you have a System of Record, EVEN A SMALL ONE, this is a competitive advantage…

So at least think about it…

Last year, we brought hundreds of the top Vertical AI & Vertical Software Founders to Miami for an unforgettable few days...

My favorite part?

I’ve now heard THREE separate stories of Founders that met investors here and raised subsequent rounds with them shortly after.

How cool is that???

Magic happens when you get hundreds of incredible Vertical AI & SaaS founders in a room for a few days...

We’re doing it again, but Bigger & Better in H2 2026 😃 😃 😃

I can’t wait to share the speaker lineup with you all...

It’s truly a who’s who of VERTICALS.

PS - I will give free tickets to a bunch of folks that opt in above :-))

Why Casca Could Be a Key Player in Vertical AI for Lending

Most Vertical AI companies don’t win because the tech is clever. They win because the economics are impossible to ignore.

Casca (formerly known as Cascading AI) is an interesting example in the Vertical AI space right now—a case study for why some wins aren’t just about flashy AI tech—they’re about potentially rewriting the economics of an industry.

I’ve been following lending tech for a while, and the pain in loan origination is brutal. Legacy systems—think COBOL-era software from the ‘80s or ‘90s—are slow, manual, error-prone, and completely incapable of scaling in today’s environment. For banks (especially community and regional ones) and non-bank lenders, this translates to real money bleeding out:

Sky-high cost per loan processed

Weeks-long decision times that kill applications (abandonment rates are painful)

Lost revenue from deals that walk away to faster fintechs or worse—predatory lenders charging insane APRs

Compliance headaches baked into outdated, fragmented workflows

Casca’s insight cuts through the noise: don’t just sprinkle AI on top of broken processes. Build an AI-native loan origination system from the ground up that replaces the legacy core. If you modernise the core lending workflow, you don’t just improve efficiency, you unlock growth.

This isn’t augmentation—it’s full rip-and-replace for mission-critical infrastructure. Banks aren’t experimenting; they’re embedding Casca into their lending stack because it directly ties to revenue throughput, lower costs, and better compliance at scale.

I’ve been digging deeper into Casca since spotting their early momentum, and the more I peel back the layers, the clearer it becomes why this could be one of the more compelling Vertical AI plays in fintech right now. It’s not just about the AI hype—it’s about a team that’s laser-focused on ripping out legacy pain in a market where the economics scream for disruption.

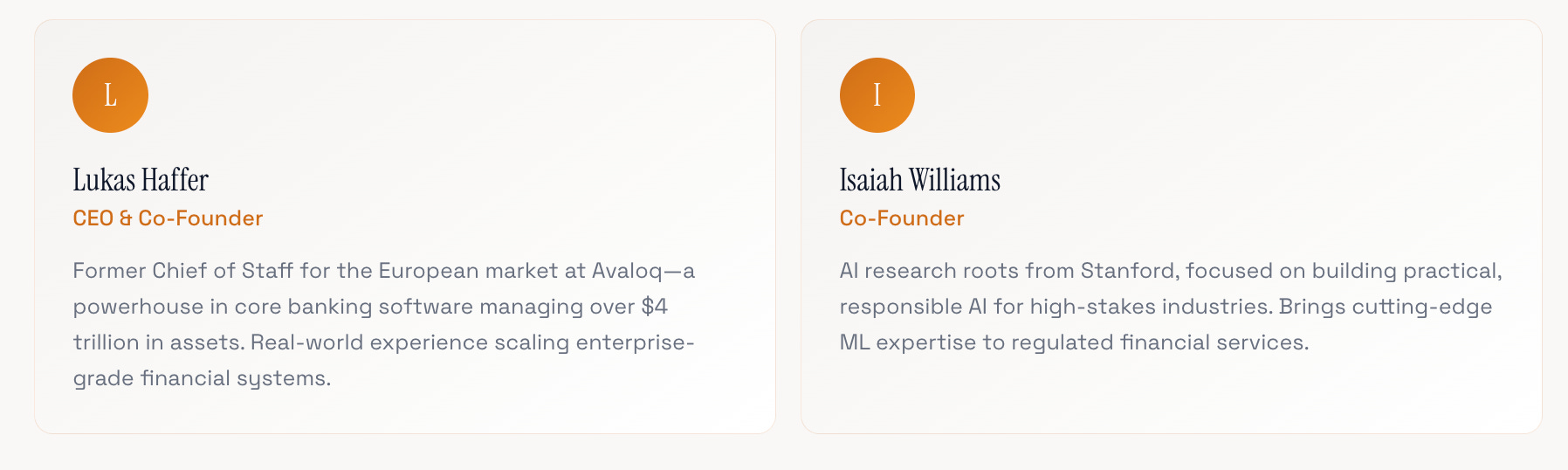

The Founders: Banking Insiders Meet AI Expertise

Casca was founded in 2023 by Lukas Haffer and Isaiah Williams, a duo that brings the perfect blend of domain depth and technical chops to tackle loan origination’s messiest problems.

Together, they’ve assembled a 37-person team (as of late 2025) heavy on engineering and product talent, with advisors including FDIC bank CEOs and fintech scouts like Simon Taylor (a16z scout and Fintech Brain Food founder). This isn’t a generalist AI startup—it’s vertical from day one, born from insiders who know banking’s underbelly.

“Legacy loan systems aren’t just inefficient; they’re revenue killers. By going AI-native, Casca isn’t augmenting—it’s rebuilding the core to unlock trillions in trapped value.”

Traction: Real Metrics in a High-Stakes Market

Casca’s early traction is impressive, especially in a space where enterprise adoption moves at glacial speeds. They’re already embedded with flagship customers:

These aren’t pilots; they’re production integrations driving measurable outcomes:

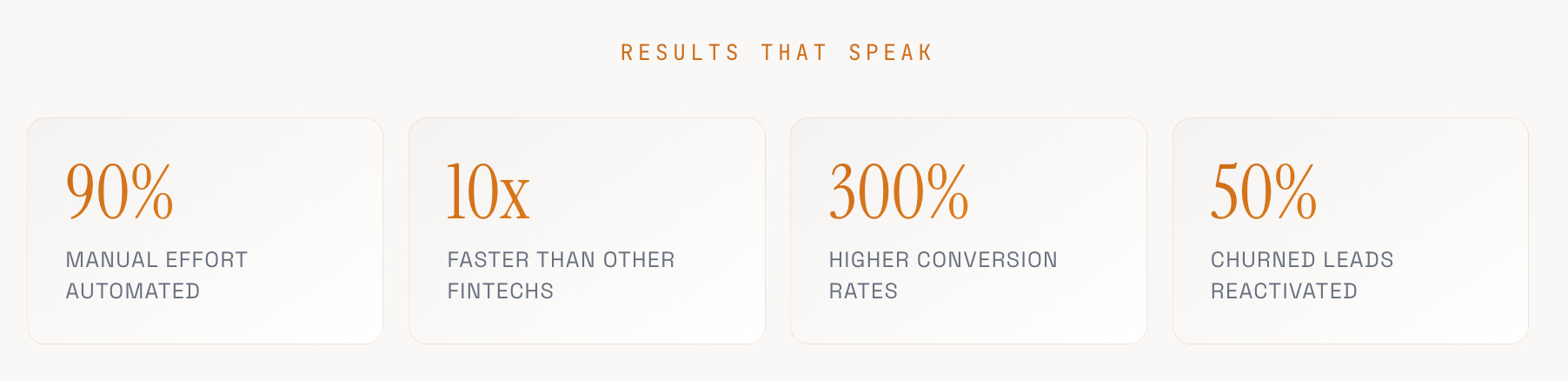

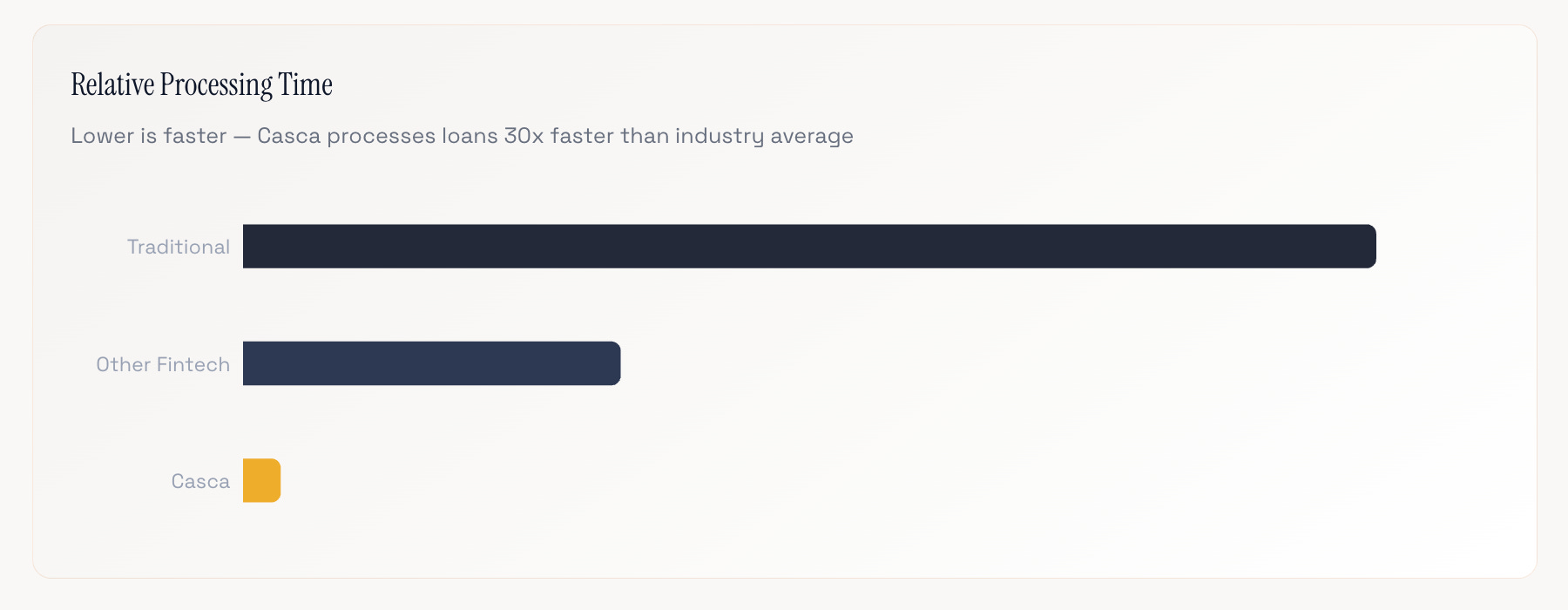

Commercial loans processed 10x faster than other fintechs and 30x faster than industry averages, with prequalification in just 5 minutes

Automates 90% of manual effort, handling 10,000+ pages of financial docs, 40+ KYB checks, and instant ratio calculations via 30+ native integrations

3x higher conversion rates through digital apps and auto-prefill; a 24/7 AI Loan Assistant responds in 2-3 minutes

Platform trusted by FDIC-insured banks and non-banks alike, setting new standards for SBA and commercial lending

Funding: Betting Big on Infrastructure Overhaul

The funding story tells the same tale. Casca raised $3.9M in pre-seed back in early 2024 to prove product-market fit. Then, in August 2025, they closed a massive $29M Series A—led by Canapi Ventures, with participation from Live Oak Ventures, Huntington, Peterson Ventures, Y Combinator, and others—bringing total funding to $33M.

That’s not “point solution” or “nice-to-have” money. That’s capital betting on core system replacement in a multi-trillion-dollar global lending market.

“Casca stands out... They’ve worked alongside top AI researchers and within banks themselves to simplify business lending using responsible AI.”

— Neil Underwood, Canapi Ventures

The business model aligns perfectly with enterprise reality in financial services:

High ACV (tied to loan volume and throughput)

Long sales cycles, but sticky, long-term contracts once embedded

Extremely high switching costs (you’re replacing the heart of origination)

Buyers with real budget authority (CFOs, heads of lending at banks/credit unions)

Why This Matters for Vertical AI

Casca sits in that rare spot: mission-critical workflow + direct revenue linkage + capital aligned with infrastructure overhaul, not experimentation. Their story reinforces an interesting take:

Will the biggest wins in Vertical AI come from full system replacement or bolt-on augmentation?

With mission-critical ties to revenue (more loans, lower costs, better compliance), high ACVs linked to volume, and sticky contracts in a regulated space, the moat is massive. They’re not selling demos—they’re selling economic transformation in a market ripe for it.

It’s a strong reminder in Vertical AI: the real winners aren’t the ones with the cleverest prompt engineering or the shiniest agent demo. They’re the ones making the economics impossible to ignore—by going after structurally broken, high-cost processes and replacing them entirely.

So, the question I keep asking myself:

Do the biggest Vertical AI wins come from augmentation or full system replacement?

Casca’s take is its full system replacement that unlocks the outsized returns. Augmentation is valuable (and easier to sell early), but it rarely changes the unit economics enough to dominate. When you rip out the legacy core and build AI-native from the start, you capture the full value—efficiency, speed, scale, and defensibility.

Casca is proving that thesis in real time in one of the toughest verticals out there. Excited to see how far they take it. Watching this one closely as they expand.

If you’re in fintech or Vertical AI, what’s your read—can rip-and-replace scale faster than augmentation in regulated industries?

Have a product or service that would be great for our audience of vertical SaaS founders/operators/investors? Reply to this email or shoot us a note at ls@lukesophinos.com