Linear #164: The SaaS Categories That Won't Survive The Agentic Era, TekMetric: vSaaS for Auto Shops

One vSaaS breakdown. One biz story. One 'how to'. In your inbox once a week.

Today’s newsletter is sponsored by Xplor Pay. In a case study they show how a POS provider embedded payments using PayFac as a Service without taking on the burden of compliance, risk, or merchant onboarding.

Learn how white-labeled payments, streamlined setup, and flat-rate pricing helped the platform improve the experience while unlocking new recurring revenue. Read the full case study here.

Alright, let’s get to it…

Dead Weight -- The SaaS Categories That Won’t Survive The Agentic Era

Search was just the appetizer.

AI is coming for the $600B horizontal software market— and most companies aren’t ready for what’s next.

Something fundamental is shifting in the software landscape. It’s not just another cycle of multiple compression driven by interest rates—this time, the market is pricing in something far more existential: the possibility that AI agents will render entire categories of software obsolete.

The thesis is simple and terrifying: if an AI layer can understand the work, access the tools, and execute end-to-end workflows autonomously, then a massive swath of “thin” SaaS—products that are essentially UIs on top of commodity logic—gets re-rated from “essential infrastructure” to “nice-to-have middleware.”

Three Phases of Software Disruption

Phase #1: AI Eats the Open Internet

GPTs replace traditional search as the primary information retrieval layer. Google’s ad-driven model faces its first existential threat.

Content creators lose organic distribution. Traffic from search collapses. The open web begins to hollow out.

Users shift from browsing 10 blue links to conversational interfaces that synthesize answers. The click economy dies.

Phase #2: AI Eats Horizontal SaaS & Point Solutions

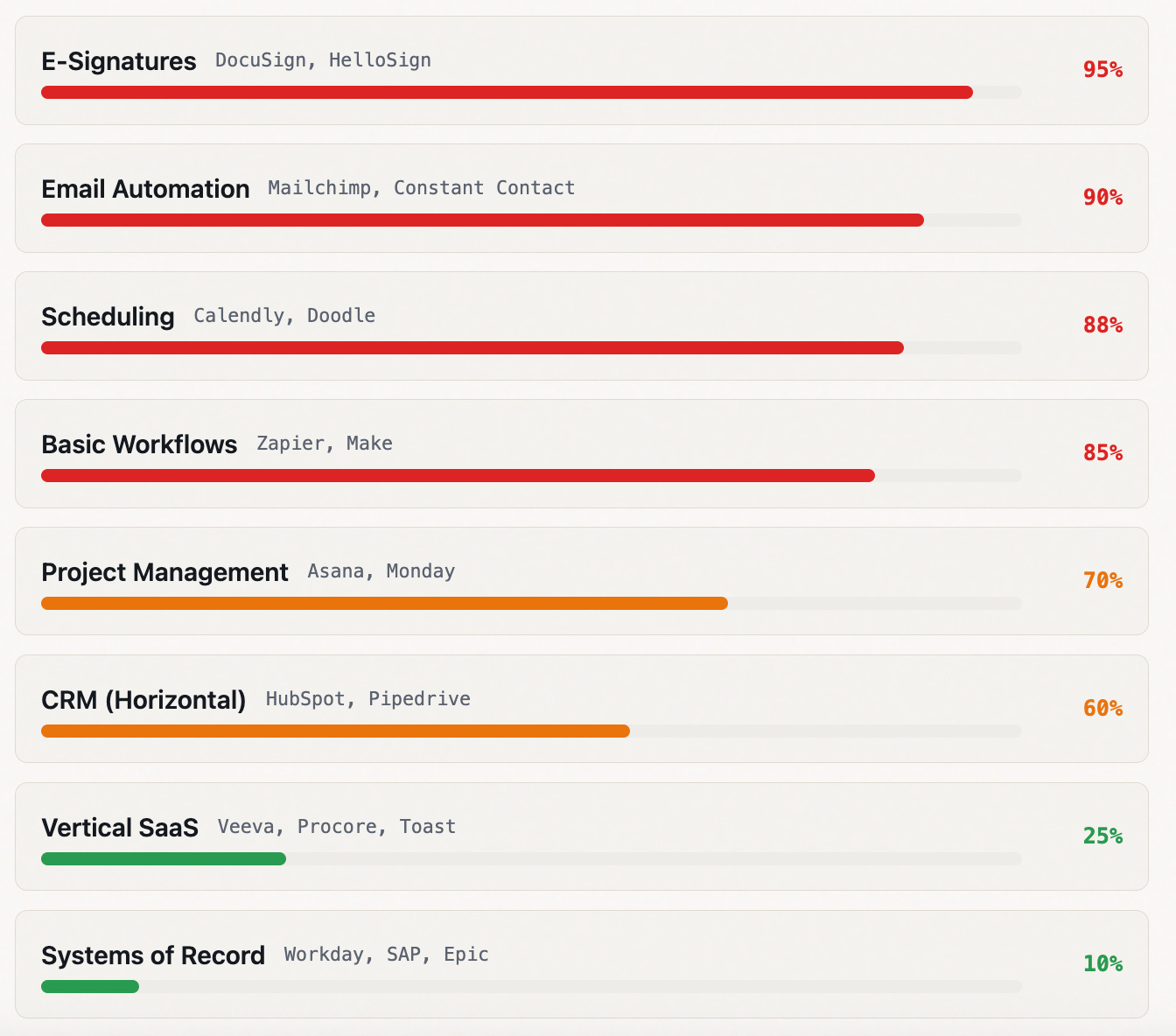

E-signatures, email automation, scheduling, basic workflows — all become features of an AI layer, not standalone products.

The “thin” SaaS layer gets compressed. Products with 90% commodity features and 10% differentiation get re-rated to zero.

AI agents can understand work context, access tools via APIs, and execute end-to-end workflows without human intervention.

Enterprise buyers start questioning: Why pay $50/seat/month for a tool an AI agent can replicate for pennies?

Phase #3: The Great Re-Rating

Public SaaS multiples compress further as the market prices in agentic disruption risk across every horizontal category.

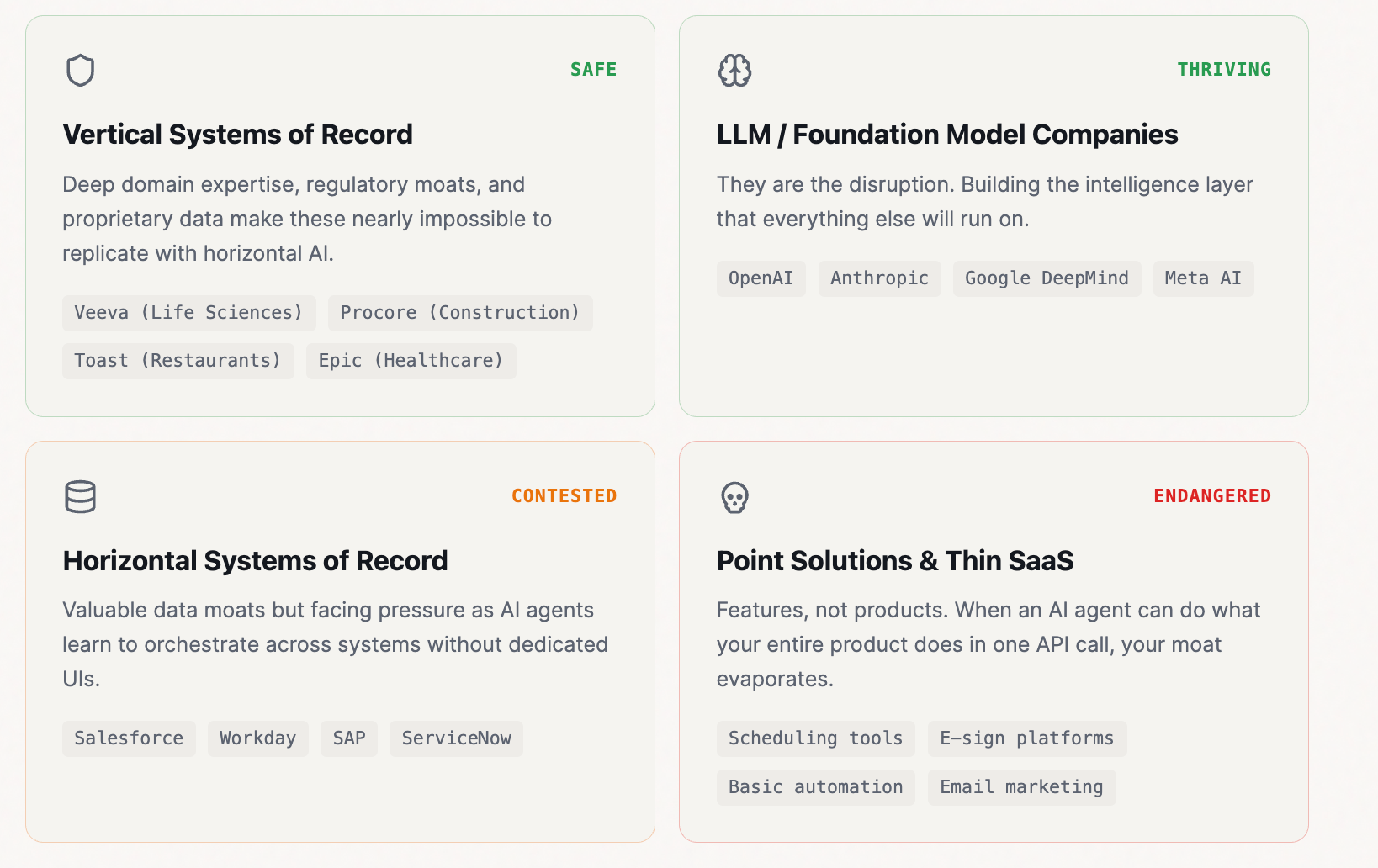

Only systems of record — vertical platforms with deep, proprietary data moats — maintain premium valuations.

The venture landscape bifurcates: AI-native infrastructure vs. deep vertical software. Everything in between gets squeezed.

//

The transition from Phase 1 to Phase 2 is where the real carnage begins. Phase 1 was almost abstract—AI replacing search felt like a “Google problem.” But Phase 2 hits different because it strikes at the $600B+ horizontal SaaS market. Every scheduling app, every e-signature platform, every email automation tool is now in the crosshairs.

Think about what an AI agent actually needs to schedule a meeting: access to a calendar API, understanding of context (who you’re meeting, when you’re free, preferences), and the ability to send an email. That’s it. That’s the entire product moat of a $3B scheduling company, replicated in an API call.

AI Disruption Matrix

Not all software is equally vulnerable.

Here’s how different categories stack up against agentic AI disruption:

Where Does This Leave Venture?

VCs aren’t stupid. They’ve been watching the same disruption thesis unfold and have been quietly (and not so quietly) retreating into Vertical Software. The logic is compelling: more defensible distribution, deeper proprietary data, tighter ROI loops, and regulatory moats that no foundation model can easily replicate.

If horizontal gets “eaten,” vertical still has teeth. A healthcare EMR isn’t just a UI—it’s a compliance framework, a clinical workflow engine, a billing system, and a longitudinal patient record all in one. An AI agent can’t just waltz in and replace that with a prompt.

The Survival Matrix

If you’re not a system of record (ideally vertical) or an LLM company, you’re in a very dangerous place.

OpenAI’s Blueprint Says It All

OpenAI’s latest Frontier platform announcement isn’t just a product launch — it’s a declaration of war on all SaaS with the exception of Systems of Record. Look at the architecture: they’re building the full stack from model intelligence to agent execution to business context.

The message is clear: if your product is a “thin” workflow layer between the user and their systems of record, you’re about to be sandwiched. OpenAI (and others) are building the agent execution layer that makes your middleware obsolete. The only thing that survives is the system of record itself.

Counter Point:

I’ve read a few posts about those saying the System of Record is equally as vulnerable.

Why? They basically say the AI Agents can just clone/copy them.

The claim here is: a surprising amount of SoR product is just CRUD + permissions + workflow + reporting + forms. If agents can:

infer intent from conversation,

generate forms,

validate inputs,

call APIs,

produce audit trails,

…then a large portion of the experience can be replicated without replicating the vendor.

This is the “cloned CRM” intuition people cite: once the agent can operate tools reliably, a lot of “app-ness” gets reimplemented as agent skills + connectors.

My Verdict:

We’re going to see the death of horizontal software AND point solutions over the next few years. This isn’t hyperbole—it’s the logical conclusion of what happens when intelligence becomes a commodity and execution becomes automated.

The survivors will be those who own the data (systems of record), own the domain (vertical specialists), or own the intelligence itself (foundation model companies).

I don’t see SoR’s going away no matter what you’re reading right now. Operators/Founders know what has gone into their creation and the moat that exists.

I do believe SoR’s + Agents on top is the future.

So my view is that if you’re not a system of record (ideally a vertical one) or an LLM company, you are in a very dangerous place.

Last year, we brought hundreds of the top Vertical AI & Vertical Software Founders to Miami for an unforgettable few days...

My favorite part?

I’ve now heard THREE separate stories of Founders that met investors here and raised subsequent rounds with them shortly after.

How cool is that???

Magic happens when you get hundreds of incredible Vertical AI & SaaS founders in a room for a few days...

We’re doing it again, but Bigger & Better in H2 2026 😃 😃 😃

I can’t wait to share the speaker lineup with you all...

It’s truly a who’s who of VERTICALS.

From Physician to Police Officer to Shop Owner to SaaS CEO: The Wild Tekmetric Story

You know what’s better than a founder who comes from the industry they’re serving? A founder who took the absolute longest, most unconventional path to get there.

Meet Sunil Patel.

Sunil didn’t start in software. Hell, he didn’t even start in auto repair. His journey went like this: medical school → physician → volunteer police officer → luxury auto repair shop owner → SaaS CEO.

I’m not making this up.

In the mid-2000s, fresh out of medical school, Sunil was visiting Detroit when he met a shop owner who had made the exact transition Sunil was contemplating. The guy had left medicine to follow his passion for auto repair. That conversation changed everything.

By 2008, Sunil opened Motorwërks Autogroup, a luxury European auto repair shop in Houston. For the next nine years, he lived the independent shop owner life. He dealt with no-shows leaving bays empty. He manually tracked inventory across disconnected systems. He watched shops struggle with pen-and-paper repair orders while customers worried about getting ripped off.

And he became one of WorldPac’s highest-volume parts purchasers in Houston—meaning he wasn’t running some hobby operation. This was a real business with real scale.

That’s not theoretical pain. That’s battle-tested operator credibility.

The Bootstrapped Beginnings: Building in Stealth Mode

In 2015, while still running his shop, Sunil started working on what would become Tekmetric. He assembled a small team (co-founded with Prasanth Chilukuri) and spent the next two years building in relative stealth mode, refining the product based on everything he’d learned running Motorwërks.

The first version officially launched in 2017. The wedge? Cloud-based shop management software that actually worked the way shop owners think.

Digital vehicle inspections with photos and videos

Repair order management

Parts tracking and inventory

Customer communication

Real-time reporting dashboards

Nothing revolutionary. Just the core workflows done 10x better than the legacy garbage most shops were stuck with.

Pricing started at just $99/month with unlimited users, unlimited ROs, and unlimited support. No massive upfront costs. No painful implementations. Month-to-month with discounted annual plans.

This is the vSaaS wedge playbook: low friction, high value, solve the daily pain first.

The Funding Journey: Capital-Efficient Growth

Here’s where Tekmetric’s story gets really interesting. While most SaaS companies were racing to raise massive rounds and burn cash on growth-at-all-costs strategies, Tekmetric took a different path.

Total funding raised: ~$5M across three rounds

2016: Seed round from Narahari Investments

2018: Small venture round (amount undisclosed)

2022: Growth equity from Susquehanna Growth Equity (March 2022)

That’s it. According to multiple sources including PitchBook and Crunchbase, Tekmetric raised approximately $5M total over six years. Some sources cite $1.14M-$1.6M in disclosed amounts, suggesting the remainder came through undisclosed portions of later rounds.

Compare that capital efficiency to the customer growth:

By 2024: Tekmetric was serving 13,000+ shops across North America with a team of 189 people (per Getlatka).

By June 2025: An Instagram post from Tekmetric referenced “more than 10,000 shops” using DVIs.

By November 2025: A press release cited “more than 12,000 shops.”

By February 2026: The latest BusinessWire announcement for Tektonic 2026 states “more than 13,000 shops nationwide.”

To put that in context: 250,000+ independent repair shops exist in North America. Even at 13,000 customers, Tekmetric has penetrated just 5% of the market. The opportunity is still massive.

As for revenue, Getlatka reported Tekmetric hit $15M in revenue in 2024, up from $7.2M in 2023 and $2.9M in 2021—suggesting strong growth trajectory on minimal outside capital.

The Platform Expansion: Where the Real Money Lives

Once Tekmetric owned shop operations, they did what every smart vSaaS company does: they moved into payments and marketing.

Around 2017-2018, they integrated with Stripe to launch Tekmetric Payments. Instead of shops using separate POS systems with reconciliation nightmares, everything flows through one platform:

Card-present and card-not-present transactions

Text-to-Pay for remote collections

Buy Now, Pay Later integration (Affirm, Klarna, Sunbit)

Apple Pay, Google Pay, contactless

Automated reconciliation tied to repair orders

According to Tekmetric’s own case study with Stripe, shops with BNPL enabled saw average order volume triple. When customers can finance a $3,000 brake job, they say “yes” instead of “not today.”

Payment processing margins are beautiful. We’re talking 2-3% of gross payment volume. When your average shop processes $500K-$2M annually, that becomes serious high-margin recurring revenue stacked on top of the software subscription.

Then came Tekmetric Marketing (launched 2025):

24/7 online scheduling

Automated appointment reminders (cuts no-shows)

Follow-ups on declined jobs

Review requests

Seasonal campaigns

Professional website builder

Every feature designed to keep customers coming back automatically, without shops lifting a finger.

The Numbers Don’t Lie: Customer Results

This is where vSaaS gets real. Tekmetric customers aren’t seeing marginal improvements—they’re fundamentally transforming their businesses:

Mission Auto KC: Monthly revenue doubled from $40K-$50K to $90K after implementing Tekmetric.

Wiggs Auto & Fleet: Went from $500K to $1.7M in annual revenue in 4 years. Their five-shop operation grew monthly revenue 48% (from $155K to $230K) in just nine months. The flagship store alone doubled sales.

Campus Automotive: Increased revenue by $300K in 6 months.

These aren’t vanity metrics. These are real shops with real P&Ls that are night-and-day better because they finally have software that works.

The M&A Strategy: Building the Category Leader

In October 2024, Tekmetric made its first acquisition: Shopgenie, a Scottsdale-based competitor that had reached $5M ARR in just 18 months (per Houston Business Journal reporting on the deal).

Say whaaaaaaaat.

Shopgenie’s rapid growth validated that the market was still wide open. The acquisition wasn’t defensive—it was offensive. Tekmetric is consolidating a fragmented category and aiming for what Sunil publicly called “unicorn status” in an interview with the Houston Business Journal.

Why Auto Repair Is a Massive vSaaS Opportunity

Let’s zoom out and talk about why this market is so compelling:

The TAM is enormous:

U.S. auto repair market: $300B+ annually

Independent repair shops: 250,000+ locations

Average shop: 1-3 locations, owner-operated

Tech penetration: Embarrassingly low

Most shops were (and many still are) running on:

Decades-old on-premise software

Pen-and-paper systems

Disconnected tools for everything

Manual end-of-month reconciliation hell

This is the vSaaS dream scenario:

✅ Large, fragmented market with terrible incumbents

✅ Daily-use software with high switching costs

✅ Payment integration that drives margin expansion

✅ Low churn because shops need it to operate

✅ Operator founder with deep domain expertise

And here’s the kicker: most shops haven’t switched yet. Even at 13,000 customers, Tekmetric has penetrated less than 6% of the market. There are still 237,000+ shops out there running on legacy garbage.

The Go-To-Market That Actually Works

Sunil’s strategy was textbook vSaaS (before the textbook even existed):

1. Product-Led Growth

Start at $99/month. Make onboarding frictionless. Let the product sell itself through word-of-mouth in a tight-knit industry.

2. Customer Obsession

Tekmetric literally road-tripped across North America visiting customer shops. Not surveys. Not Zoom calls. They showed up, watched teams work, and built what operators actually needed. That earned them top G2 ratings and a fanatical customer base.

3. Community Building

They launched Tektonic, a multi-day conference for shop owners, advisors, and technicians. The 2026 event (April 9-11 in Houston) features keynotes from Codie Sanchez and Mike Michalowicz, plus 50+ breakout sessions. This isn’t a user conference—it’s a movement.

4. The Platform Play

Don’t just be shop management software. Own operations, payments, marketing, and customer engagement. Become the operating system for the entire business. When you’re that embedded, you’re not getting ripped out.

What We Can Learn From Tekmetric

If you’re building in vertical SaaS, here’s what Tekmetric teaches us:

1. Operator credibility matters. Sunil’s nine years running Motorwërks gave him instant credibility. He knows the language, the pain points, the workflow bottlenecks. That’s not something you fake.

2. Capital efficiency > vanity metrics. They built a 13,000-customer business on ~$5M in funding. That’s roughly $385 in funding per customer acquired. Most SaaS companies would kill for those economics.

3. Win with simplicity first. Don’t try to boil the ocean. Nail the core workflows that shops live in every day. Make those 10x better than the incumbent. Then expand.

4. Payments are a superpower. Once you’re processing transactions, you have incredible data and a high-margin revenue stream. Consumer financing options (BNPL) are table stakes now—they literally help customers say “yes” to bigger repairs.

5. Think platform, not point solution. The best vSaaS companies start with a wedge and become the full-stack operating system. Shop management → Payments → Marketing → [what’s next?]. Each layer increases stickiness and ARPU.

6. Community builds moats. When your customers become evangelists, when they attend your conferences, when they contribute to your product roadmap... that’s a competitive advantage no VC-backed competitor can copy.

The Bottom Line

Tekmetric is what vSaaS looks like when it’s done right. A founder with deep domain expertise and an unconventional path. A wedge product that solves real pain. A platform expansion that captures more value. Payment integration that drives margins. And a customer base that’s genuinely thrilled with the product.

Over 13,000 shops trust Tekmetric to run their businesses. That’s not hype. That’s operators voting with their dollars every single month.

And here’s the kicker: the auto repair vertical is just getting started with digital transformation. There are still 237,000+ shops out there running on legacy systems or pen and paper. The opportunity is enormous.

So here’s my question for you: What vertical are you underestimating right now? Where could you build the next Tekmetric?

What are you waiting for? Go find your Tekmetric.

Have a product or service that would be great for our audience of vertical SaaS founders/operators/investors? Reply to this email or shoot us a note at ls@lukesophinos.com