#098: The Latest SaaS Benchmarks, The Story of Blackboard.com, My Favorite vSaaS Playbooks

One vSaaS breakdown. One biz story. One 'how to'. In your inbox once a week.

Todays newsletter is sponsored by Check, the leading payroll infrastructure provider and pioneer of embedded payroll.

Check makes it easy for any SaaS platform to build a payroll business, and already powers 60+ popular platforms supporting 20M+ employees such as Wave, Homebase, and HousecallPro .

Alright, let’s get to it…

One vSaaS Breakdown:

SaaS Benchmarks Report - Q4 2024

KeyBanc Capital Markets drops a SaaS Benchmarks report every year and it’s always on the must read list. I pulled all the interesting insights for you all. Here goes…

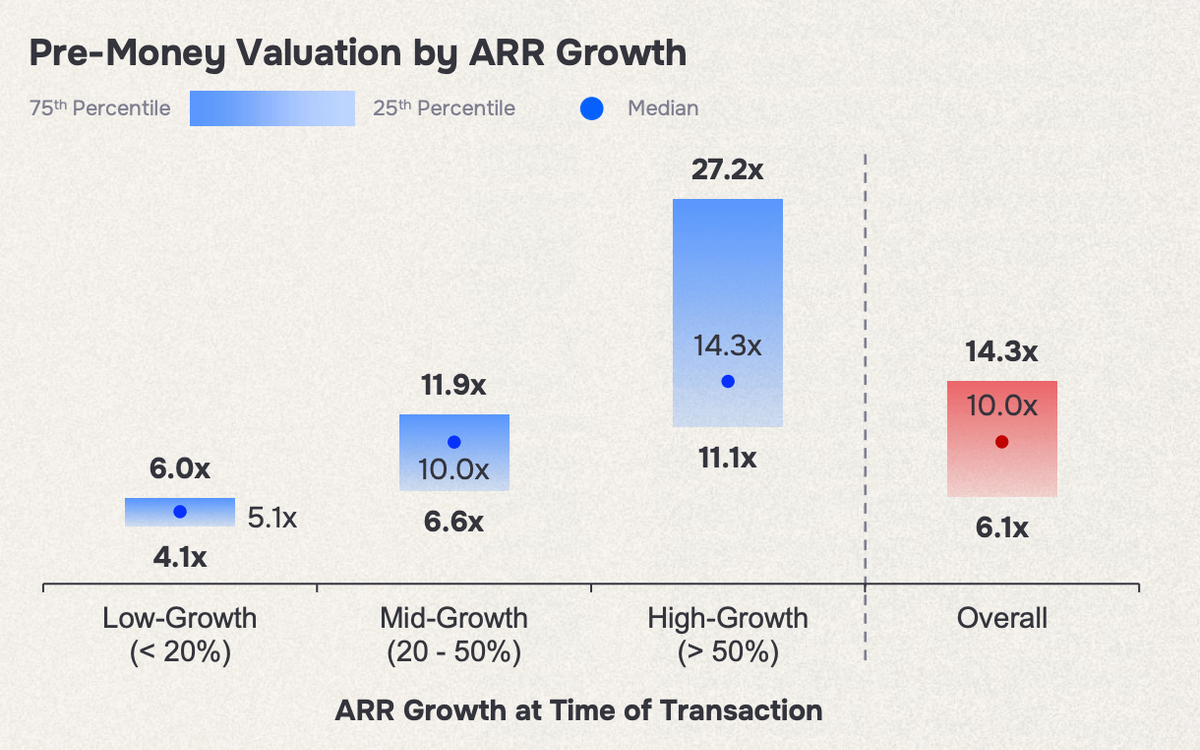

Revenue Multiples:

When you hear about people getting 50X ARR multiples on AI Start-Ups just take a deep breath, don’t go into negative thinking mode, and look at the public markets. They are always your sanity check! Not some crazy private round that happened. A few key things to remember:

The average public SaaS companies revenue multiples over the last ~20 years is 4.9X.

The all time high public SaaS revenue multiple was 16.3X

We’re currently sitting at 5.7X.

An important reminder…

Growth rates massively impact valuation.

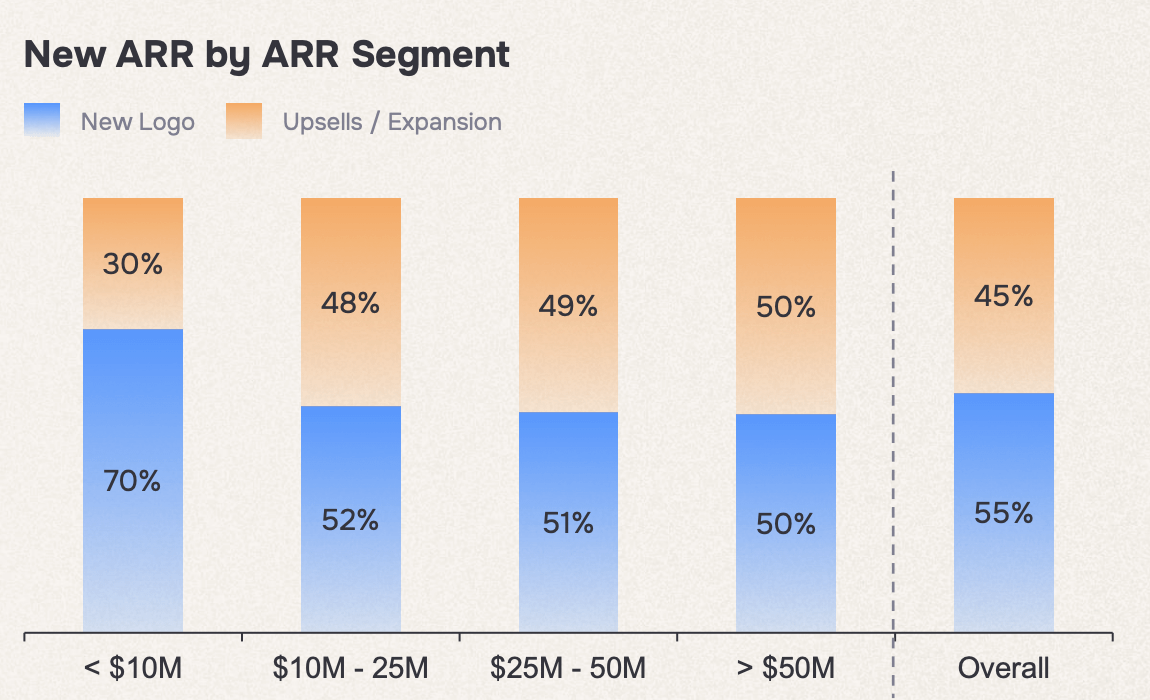

ARR:

In every single report I’ve seen, ARR growth has gotten WORSE YoY since 2022. Remember the SaaS markets crashed November/December 2021. It also gets harder and harder to continue growth as your business gets bigger and bigger.

It is so much easier to sell to an EXISTING customer than a NEW one. You know what's crazy? Once you hit ~$10M of ARR, half of your revenue comes from existing customers.

People forget this too often.

Put as much time into your expansion motion as you do your new biz one.

With tough markets comes more efficient and productive SaaS companies. Average ARR per employee continues to grow YoY. It sure has in my business.

Interesting to also observe that 27% of their respondents had average contract lengths of 3+ years. That is something new I have not historically seen a lot of. Personally, I don’t think it’s reflective of the broader market, but if your locking in 3+ year deals more power to you. Keep at it.

The majority of SaaS companies continue to price based on users / seats.

Usage is definetly continuing to rise, and becoming more and more popular, specifically in dev tooling.

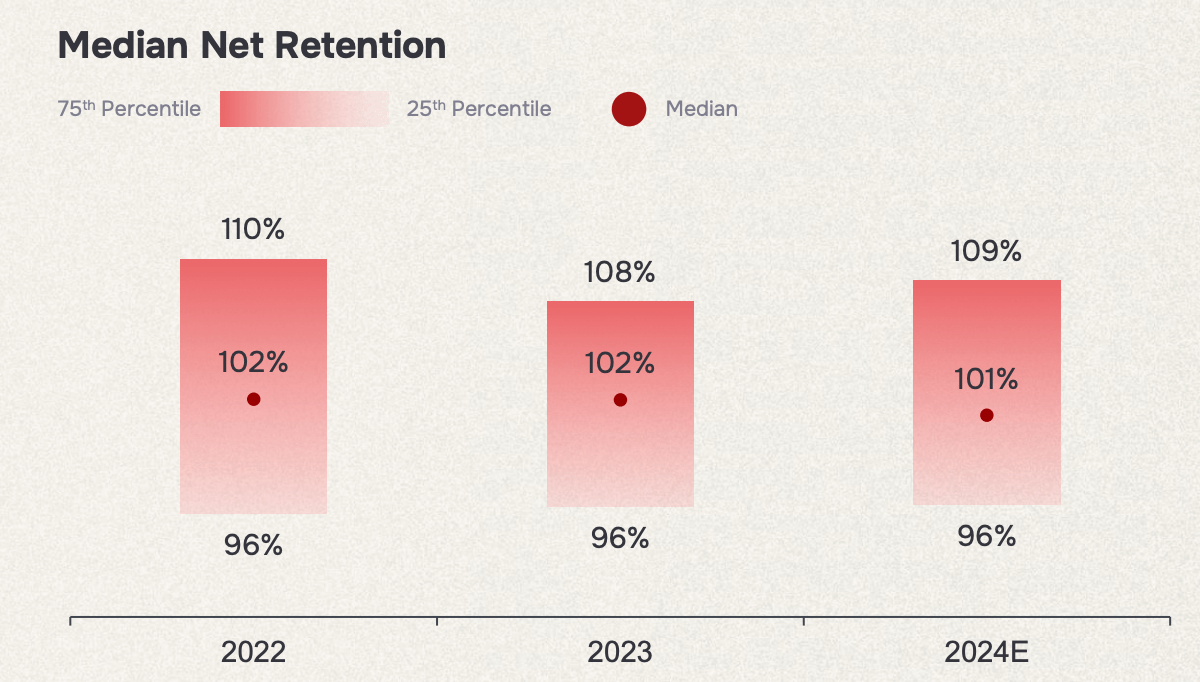

Retention:

The average net revenue retention in 2024 is sitting at 101%.

109% is excellent.

96% and you’re in the bottom quartile of SaaS companies.

A bit crazy to see how much this has decreased post SaaS crash. It feels like the norm was 110% in 2020/2021.

The average gross retention in 2024 is sitting at 91%.

95% is excellent.

82% and you’re in the bottom quartile of SaaS companies.

One tip I give vertical SaaS founders is to hire Customer Success folks from your vertical. Not SaaS Customer Success folks. I've seen this simple hack work again and again. I took this number from bottom quartile to top in ~2 years by doing so.

Thanks to the folks at KeyBanc and Sapphire Ventures for the beautiful report.

If you want to access the full report head here.

One Biz Story:

The Story of Blackboard.com

In 1996, Cornell students Stephen Gilfus and Daniel Cane founded CourseInfo in their dorm rom. The goal? Create a course management system that would enable students and instructors to access everything they needed to know about their college classes online.

One year later, Michael Chasen and Matthew Pittinsky were working on a very similarily prototype while working at KPMG. Cane of CourseInfo, and Chasen of Blackboard, met at an education conference and decided to merge the companies to help raise money and scale the business.

The Blackboard team started out with a freemium model, allowing instructors to host their courses online for free for two weeks, before having to move to a paid model. By 1998 they had instructors at 15 Universities utilizing their software eclipsed $1M in revenue.

That was enough for the company to raise their first round of venture capital, a $1.9M Series A round in 1999. With the dot com boom in full effect, their Series B and Series C happened in relatively short order - a $3.5M Series B round in 1999, and a $12.5M Series C in 2000.

Selling into higher education is well known in the venture capital community to be INCREDIBLY difficult. Blackboard was such an early mover that it doesn't seem they faced the same type of challenges. In 5 years from their founding, they had achieved 39% market share 🤯🤯🤯

It didn't seem like Blackboard could be stopped. The company went public in 2005 at a valuation of $350M. An absolutely INSANE number for a group of college students who founded the business in their dorm room.

Leveraging funding from the public debut, they acquired two other dot com education start-ups, Prometheus LMS and WEB CT LMS in 2005 and 2006. That, along with their organic growth, led to blackboard owning 60% of the higher education market by 2006 (!!!!)

Blackboard is a case study that vertical SaaS companies can achieve such a larger percent of market share than horizontal peers. Tailor-made features and capabilities allow for this. 60% is truly INSANE. But it'd be Blackboard's peak.

The company hit a bit of a wall between 2007 and 2009 as competitors emerged. Moodle, an open-source LMS, came onto the scene with a solution far cheaper and more customizable.

Blackboard made the decision to sell the business to Providence Equity Partners in 2011 for a whopping $1.64 BILLION Chasen, Co-Founder & CEO, would only remain at the company for one more year, through 2011. Pittinsky was gone by 2012.

Providence Equity ran the classic Private Equity strategy. They brought in Jay Bhatt, a professional CEO, and went on a crazy acquisition spree. They bought 20+ companies over the next ten years. Gluing together so many companies created a lot of challenges for end users...

According to a TechCrunch article, despite its success, Blackboard had become "one of the most disliked — even detested — companies in education." Fast Company reported that 93% of respondents to a customer opinion survey "hate" the company.

Even with the amount of acquisitions, Blackboard's market share continued to rapidly shrin. Canvas LMS, an innovative upstart out of Utah began to rise to prominence.

In 2021, Blackboard merged with Anthology, a provider of back-office tools for Higher Education, with a flagship Student Information System.

Blackboard is a case study in:

College students can create incredibly innovative companies from their dorm rooms

Vertical SaaS continues to show that they can acquire SO MUCH more market share than their horizontal peers.

Acquiring companies can be disastrous

It is too early to tell how the Anthology + Blackboard combination will go.

Time will surely tell.

One ‘How To':

Some of My Favorite Playbooks

I have 50+ playbooks in the Vertical SaaS Bible.

A few of my favorites:

Vertical AI Co-Pilots

Vertical SaaS + Embedded Payments Playbook

Land & Expand Strategy

Using Maslow’s Hierarchy of Needs To Build Great Products

All B2B Products Eventually Converge

Check them out!

Have a product or service that would be great for our audience of vertical SaaS founders/operators/investors? Reply to this email or shoot us a note at ls@lukesophinos.com