#092: Your TAM Is Why I Have Trust Issues

One vSaaS breakdown. One biz story. One 'how to'. In your inbox once a week.

Today’s episode is brought to you by Vaya.

vSaaS companies use Vaya’s embedded credit to gamify adoption of their most important features.

Embed Vaya to accelerate your growth and retention.

Something a little bit different today, but I think you’ll like it…

My friend CJ Gustafson, a SaaS CFO and author of Mostly Metrics and I were chatting about the level of “stretchiness” most founders push when pitching their TAM (totable addressable market).

So I asked him to write up a guest post for us this week on the exact topic. It’s a good one. And if you’re not subscribed to his newsletter yet, I highly recommend it. It’s wonderful.

So without further ado, a guest post from the SaaS CFO and Mostly Metrics legend, Mr. Gustafson…

Your TAM Is Why I Have Trust Issues

I trust your TAM as far as I can throw it.

TAM, or Total Addressable Market, is a mainstay in all startup pitch decks. It attempts to convey the size of the revenue opportunity a company is chasing.

The simple thinking is a big market = more surface area for good things to happen.

But if you dig a bit deeper, the TAM a company quotes is often nothing more than a farce - a big number on a page, either lacking in analytical credibility or real world applicability.

Here are the most common problems with TAM analyses:

Lack of credibility

Doing the big number thing

Taking credit for someone else’s TAM

But first, why is TAM important in the first place?

Mostly metrics is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Upgrade to paid

Why is TAM important?

Investors need to think each investment can return the fund

As a rule of thumb, investors will often want to see a scenario where any given company could theoretically return the fund 1x.

So, if you are talking to an investor managing a $500M fund, the investor would be looking for a $500M return potential.

The simple math then would be in order to generate $500M returns, at 20% ownership the company needs to be valued at $2.5B at exit.

Assuming we are looking at a software company we could very simplistically assume a 10x exit revenue multiple (generous!) which would imply the company needs to reach $250M in revenue at exit

“We talk about power laws in venture investing and typically what we see is a smaller handful of companies return a larger number of returns for those funds.

And also we can’t invest in 200 or 300 companies; it’s not feasible to handle.

So we do require a certain type of exit or outcome. And if that has to be possible, we have to think hard about TAM, and unfortunately sometimes that means the TAM is too small for us”

-Sebastian Duesterhoeft, Partner at Lightspeed Ventures

(RTN Pod: Spotify / Apple / YouTube)

TL;DR: The mechanics of how venture firms work impact the size of the prize they need to go after. Investors, therefore, need to work backwards from a potential outcome, which is dependent on the market and revenue opportunity.

The “next buyer” analysis

However, there has to be an exit at some point.

It’s important to realize that when the investor sells, there has to be another buyer that is actually willing to pay a [10x] revenue multiple.

For that to happen, the next investor still needs to see a meaningful growth opportunity.

So now we aren’t even thinking of a $2.5B market, we are thinking about a multiple of $2.5B.

A 15-20% return for that next buyer would imply a 2x over 5-7 years, at which point the company would have to be $500M+ in revenue.

“There is a next buyer analysis where you have to think hard about how is the investor going to think about the opportunity when your journey with the company may end”

-Sebastian Duesterhoeft, Partner at Lightspeed Ventures

TL;DR: VCs are working backwards not only from their expected outcome, but also the next buyer’s expected outcome.

OK, so now that we understand why TAM is important, let’s dig into why it’s often done so poorly.

Lack of credibility

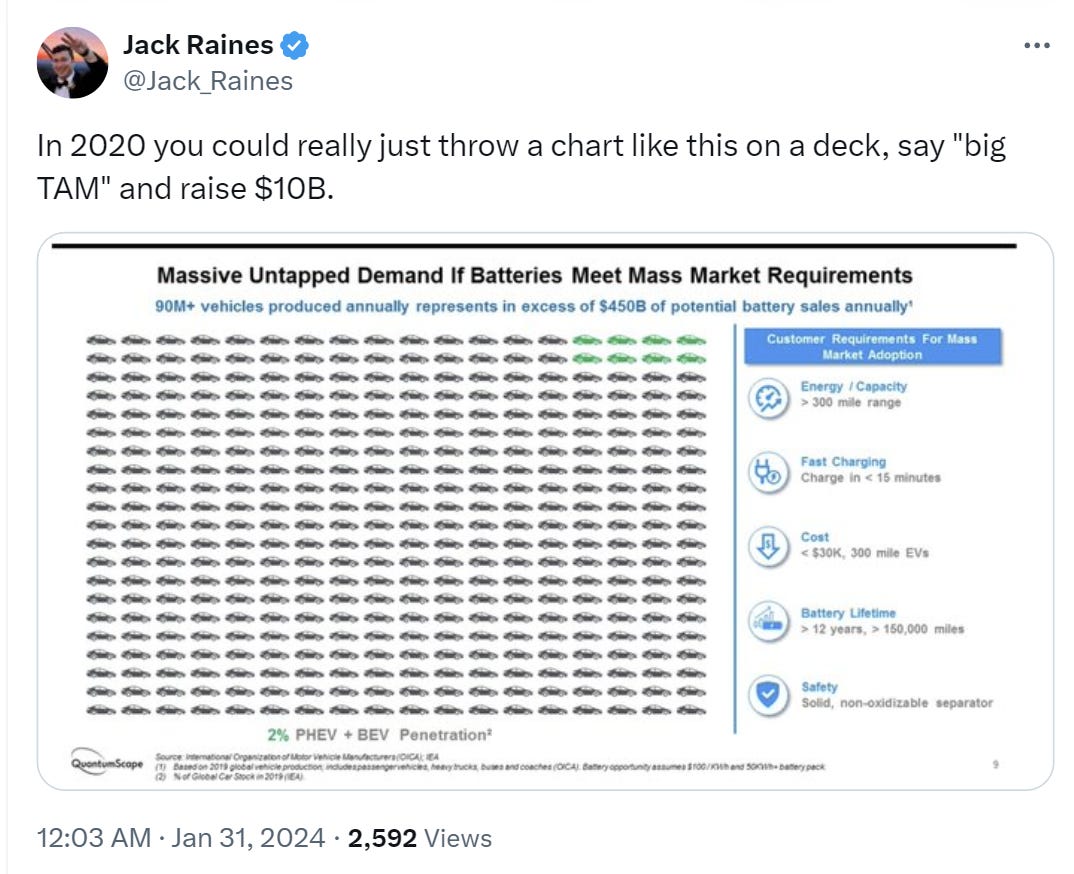

Half the world is men. That doesn’t mean half the world will buy your shaving kit.

Tops down TAM analyses, especially when cobbled together from a third party source, like a Forrester or Gartner, are lazy.

It’s common for companies to simply add up a bunch of pre-existing categories to create a large number, without actually deconstructing what’s in those “pre packaged” figures.

“I dismiss [TAM] in many respects. Because for the most part, they aren’t realistic - they lack credibility in these numbers.

I hear these TAMs - we are attacking a $30B TAM. OK, that’s great. But where did that number come from? The single biggest company that exists already in what you define as your category is a $2B company. So where is the other $28B? Where are these numbers coming from?

And then you have to unpack it… is it software? Is it software services other? They are packing it in so it looks gargantuan. But you look at every precedent company and nothing is over $2B.

So is it that fragmented? What’s going on here? The numbers don’t add up.”

-Tony Kim, Head of Technology Investments at Blackrock

RTN Pod: Spotify / Apple / Youtube

TL;DR: Quoting a massive TAM can actually hurt a company, especially if it’s taken from a third party source without any analytical rigor… and especially if the founder themselves doesn’t know what’s actually in that bucket.

Doing the big number thing

You can “math” your way to a big number pretty easily.

“Often companies will tell me, '“if we just took the Fortune 2,000 and multiplied by $1,000,000 per and we just took 2% of that…”

Large numbers times small percentages get big numbers.

And conceptually you think - yes this times that times this it’s the TAM. But that doesn’t match up with reality.”

-Tony Kim, Head of Technology Investments at Blackrock

At the core of any TAM is a P x Q (price x quantity) framework. It’s really critical to think hard about what the P x Q for your market is.

The P in theory is relatively straight-forward; it’s the price a company sets for its product.

The Q is typically what is much more difficult to determine. It’s relatively easy if your product is priced on a per seat basis, e.g. a DevOps product going after the # of professional developers (~13M in the US + Europe).

It gets a lot harder for a product like Snowflake which is priced on a somewhat difficult to grasp volumetric basis depending on the amount of compute and storage used by a company.

A workaround in those cases can be to try to determine what the spend potential of “typical” SMB/mid-market/enterprise customers is, which then allows you to extrapolate that spend to the # of companies out there in each of these size buckets.

TL;DR: Dig most closely into the “Q” a company is using in their build up. This is where the math goes off the rails.

Taking credit for someone else’s TAM

Stolen valor alert!

“So are you going to rip and replace the $40B TAM?”

“No, no no. 90% of our business is net new - it’s something else. We aren’t ripping and replacing this stuff.”

“So hold on, you aren’t ripping and replacing. You are building an adjacency or building on top of this thing. So that’s not your TAM. Your TAM is not the $40B thing you are replacing, you are building something on top… Because a rip and replace is hard to do.

So what you’ve done is take the accreditation for this massive pool of spend you really aren’t going after right away.

You are adjacent to it. But you claim it’s your TAM. You took credit for it but you are not going after it.”

-Tony Kim, Head of Technology Investments at Blackrock

Don’t claim a market you aren’t actually competing in. Close is only good in horseshoes and hand grenades.

TL;DR: Test if a company is getting “cute” as to where they directionally compete. Building on top of an existing market, or next to an existing market, is not the same thing as competing head on. Those dollars are reserved for the real gangsters.

Deconstructing the Truth

Companies come in and tell me I have this massive TAM.

I immediately zone out.

And then I say, let’s deconstruct this. What are you really saying?

Once you deconstruct truth, you realize it’s not the real TAM.

-Tony Kim, Head of Technology Investments at Blackrock

So how do you get to truth? Here are three lenses to run any TAM analysis through:

Where is the initial insertion point?

If you own the control point, from there you are embedded into a workflow, and can potentially stack layers of revenue

Depending on what your initial product is, it may or may not give you the right to compete for adjacent TAM

Toast had a great insertion point to set them up for success from the point of sale - how someone may accept payments in a restaurant is pretty critical

Toast will have a better expansion point than Yelp who offers reviews, not because they aren’t both useful to the restaurant owner, but because they aren’t equally positioned to expand to the most critical expansion areas

What’s the relative level of competition?

A massive TAM often invites massive competition. Not all dollars are created equal in terms of being up for grabs.

Fragmentation is based on Herfindahl Hirschman index. Basically, the higher the score, the closer the market is to monopoly. The lower the score, the closer it is to perfect competition.

If, for example, there was only one firm in an industry, that firm would have 100% market share, and the HHI would equal 10,000, indicating a monopoly.

If there were thousands of firms competing, each would have roughly 0% market share, and the HHI would be close to 0, indicating nearly perfect competition.

The U.S. Department of Justice considers a market with an HHI of less than 1,500 to be a competitive marketplace, an HHI of 1,500 to 2,500 to be a moderately concentrated marketplace, and an HHI of 2,500 or greater to be a highly concentrated marketplace.

The HHI is calculated by taking the market share of each firm in the industry, squaring them, and summing the result

What’s the market’s maturity, and time to capture?

Where is the market today?

Are you at a point in the maturity curve of that market where enough dollars can flow your way so you can build a company in a timeframe that matters to a venture investor?

It doesn’t matter so much if you can get to $200M in 20 years. In venture, you require a faster timeframe than that

Furthermore, is the TAM even contractually available?

Some buyers are under 3 to 5 year contracts - how do you displace those?

Other buyers don’t buy tech very often, and it’s harder to displace whatever they have used for decades, like in vertical software

Ask yourself: How fast can this all happen?

Thanks again to CJ at MostlyMetrics.com for the guest post. Subscribe to his newsletter below:

PS…

Vertical SaaS Bible’s last week of the discount period is among us. Grab it before the price jumps back up to $200 :-) Just use the code BIRTHDAY.

Have a product or service that would be great for our audience of vertical SaaS founders/operators/investors? Reply to this email or shoot us a note at ls@lukesophinos.com